MNI ASIA OPEN: Tsy Yields Retreat Ahead January Employ Report

EXECUTIVE SUMMARY

- MNI BONDS: Japanese Investors Sold OATs In December, Foreigners Buying Domestic Debt

- MNI US DATA: Imported Inflation Ended 2025 On A Stronger Note

- MNI FED: Cleveland's Hammack: Could Be On Hold For "Quite Some Time"

- MNI FED: Dallas's Logan: Currently More Worried About Inflation Than Labor Market

- MNI US DATA: Weekly ADP Tracking Continues Pace Seen In ‘January’ Print

US

MNI FED: Cleveland's Hammack: Could Be On Hold For "Quite Some Time"

In a speech largely devoted to banking regulation (speech text here), Cleveland Fed President Hammack (2026 FOMC voter, hawk) makes the case for "err[ing] on the side of patience" when it comes to rate-setting. We continue to believe that she is not supportive of any rate cuts this year, and is perhaps the biggest hawk on the FOMC at present.

MNI FED: Dallas's Logan: Currently More Worried About Inflation Than Labor Market

Dallas Fed President Logan (2026 FOMC voter, hawk) doesn't sound like she would support a rate cut in the coming months. While her base case is that inflation pressures will abate in 2026, she says in a speech Tuesday "I am not yet fully confident inflation is heading all the way back to 2 percent", and "the labor market now appears to be stabilizing, and the downside risks appear to have meaningfully dissipated" with December's unemployment rate consistent with full employment. We continue to presume that she doesn't support any rate cuts in 2026.

NEWS

MNI BONDS: Japanese Investors Sold OATs In December, Foreigners Buying Domestic Debt

Japanese balance of payments data for December was released yesterday. There wasn’t clear evidence of broad-based foreign bond shedding by domestic investors. The January data may be more interesting given the historic rise in domestic yields, amid familiar fiscal/issuance concerns. More timely weekly data suggests domestic investors were net sellers of foreign bonds in the 6 weeks to Jan 30, but foreign purchases of domestic stocks and bonds presented a far more material dynamic.

MNI STIR: Navarro's NFP Comments Help Blunt Dovish Data Reaction

Dovish repricing initially seen in the USD short end as retail sales come in on the soft side of expectations (with negative revisions). The downside surprise in the ECI was modest, particularly when rounding is accounted for, while the import price readings were mixed.

MNI INTERNATIONAL TRADE: USTR On USMCA, China Trade, India & Indonesia Deals

Speaking to Fox Business Network, US Trade Representative Jamieson Greer says that the US is entering talks with Mexico "right now" regarding the US-Mexico-Canada Agreement (USMCA) trade deal re-negotiation. Says that negotiations will continue on a bilateral basis. Acknowledges that amid cratering ties with Canada, talks on the USMCA with Ottawa are "more challenging". Trump's latest threat to stop the opening of a bridge linking Canada and the US risks further deterioration, with Greer saying the President has 'valid concerns'.

US TSYS

MNI US TSYS: Tsys Hold Curve Flattening Gains Ahead Wednesday's January Employ Data

- US Treasuries look to finish higher Tuesday, curves bull flattening (2s10s -2.617 at 68.665, 5s30s -2.461 at 108.724) with bonds outperforming. Massive block sales over a 90 minute midday period: saw -115,000 TYH6 over 90 minutes from 112-17.5 to -15, as well as -95k FVH6 from 109-11.25 to -10.

- Incidentally, Treasury futures held near highs (TUH6 104-11.88, +1.5, TYH6 +10 at 112-16) after the $58B 3Y note auction (91282CQA2) drew 3.518% high yield vs. 3.519% WI; 2.62x bid-to-cover vs. 2.65x prior.

- Treasuries gained after Peter Navarro, counselor to Pres Trump, expressed the "need to revise expectations on monthly job numbers" Bbg. (NFP for January released tomorrow).

- Taking another round of geopolitical risk with a grain of salt - markets showed little react to Pres Trump stating he may may send second carrier to Iran if talks fail, Axios reporting. Trump is meeting the Israeli PM tomorrow, with the date for the next US Iran meeting yet to be finalised.

- Japanese assets have firmed on Tuesday, bolstered by comments from Finance Minister Katayama, who appears to have successfully calmed the markets on the timing and financing of the sales tax cut. Stabilisation across the JGB curve has facilitated an extension of the Japanese yen rebound, with the USDJPY pullback from yesterday’s post-election high reaching 2.35% at today’s 154.06 low.

- All focus turns to tomorrow’s US employment data. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

OVERNIGHT DATA

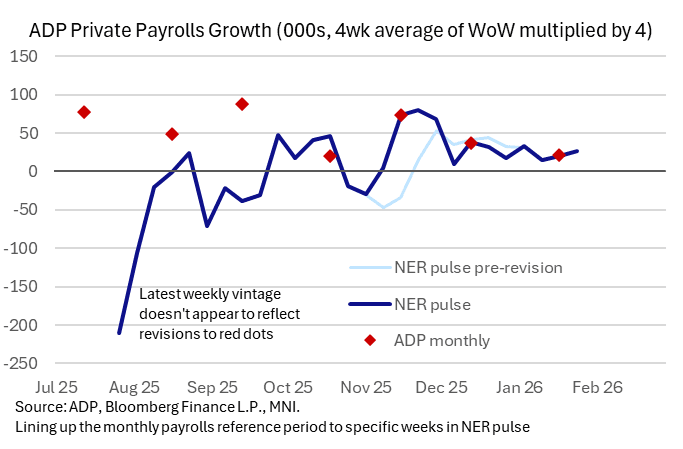

MNI US DATA: Weekly ADP Tracking Continues Pace Seen In ‘January’ Print

ADP employment increased an average 6.5k w/w in the four weeks to Jan 24. Revisions were extensive but not surprising after benchmarking in last week’s monthly report (see US DATA: ADP Employment Sees Modest Miss and Large Downard Revisions On QCEW - Feb 4).

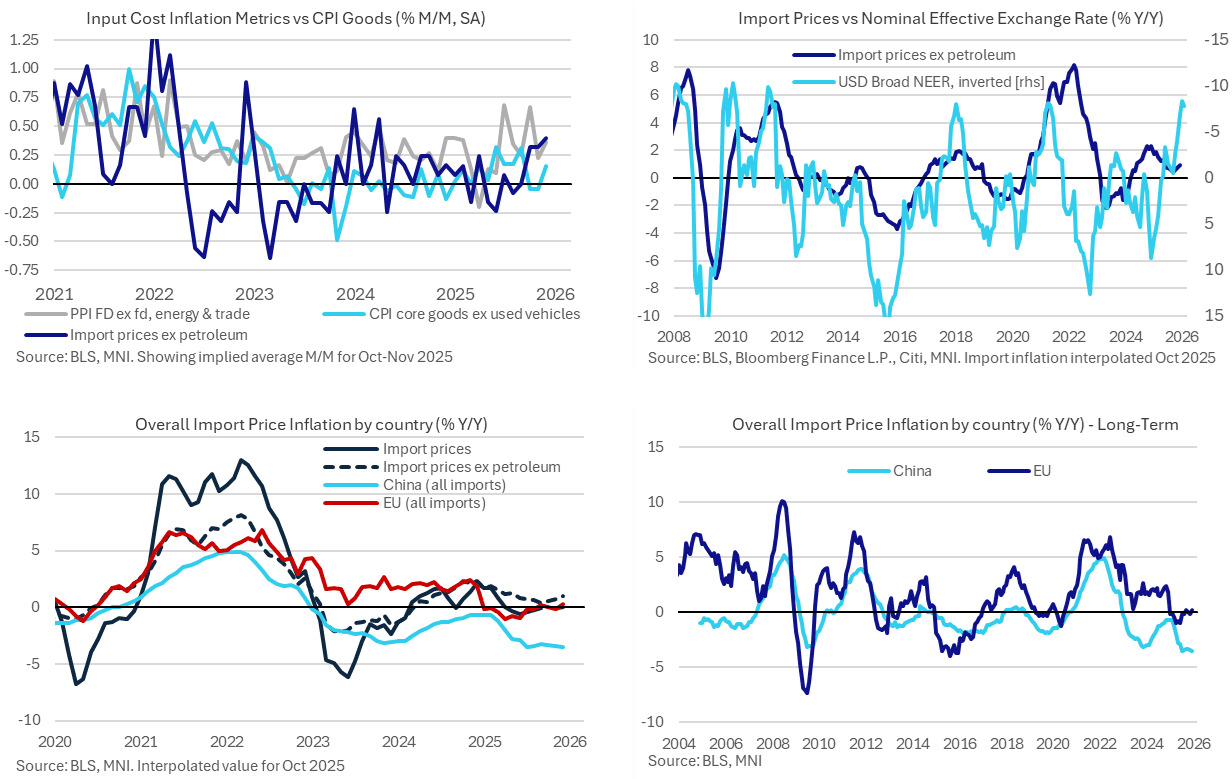

MNI US DATA: Imported Inflation Ended 2025 On A Stronger Note

Non-oil import prices were stronger than expected in December as they ended the year with some upward price pressures and with potentially more to come judging by US dollar depreciation. Bearing in mind that import prices don’t include tariffs, it points to a notably different backdrop than earlier in 2025 when foreign exporters were offering greater concessions in the face of tariffs. China stands out with firmly negative import price inflation whilst import prices from other trading partners have firmed.

MNI US DATA: Retail Revisions And Control Group Miss Confirm Q4 PCE Slowdown

December's advance retail sales data was roundly weaker than expected, which in addition to lower revisions in prior months will likely mean a pullback in Q4 personal consumption expenditures estimates in the GDP accounts. Even prior to this report, January had been expected to be a weak month for retail sales given incoming indicators, so there will be concerns about the momentum of consumption going into 2025. And the report is in nominal terms, so in volume terms Q4 2025 suddenly looks to have been closer to flat instead of robust for core goods sales.

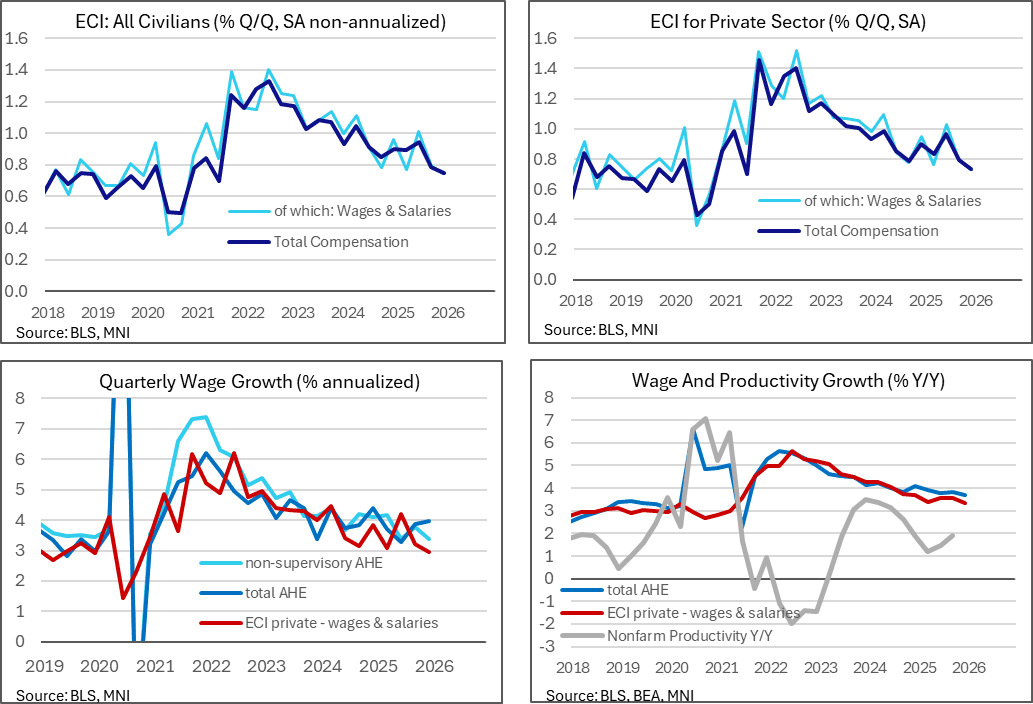

MNI US DATA: Wage Growth Moderation Continued In Q4 ECI Report

The Q4 ECI update continued a trend moderation in wage growth. This more comprehensive wage growth metric, which the Fed puts much more weight on when it comes to assessing wage dynamics, offers a softer take than hourly earnings data in recent monthly payrolls reports.

- The employment cost index was on the soft side of expectations in Q4 as it increased 0.75% Q/Q non-annualized (cons 0.8) after 0.79%. It left annualized growth of 3.0% annualized in Q4 for its softest since 2Q21 after 3.2% in Q3, 3.8% in Q2 and 3.6% in Q1.

MNI US DATA: Redbook Retail Sales Continue To Pull Away From "Official" Series

Notwithstanding the poor "official" December Census Bureau retail sales report released earlier Tuesday, Redbook retail sales continue to post robust gains into 2026. The Johnson Redbook retail sales index rose 6.5% Y/Y in the first week (and therefore month-to-date) of February, an acceleration from 6.3% in January though below retailers' targeted 6.9% gain for the month.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 91.64 points (0.18%) at 50230.44

S&P E-Mini Future down 13.5 points (-0.19%) at 6970

Nasdaq down 106.5 points (-0.5%) at 23132.06

US 10-Yr yield is down 6.1 bps at 4.1407%

US Mar 10-Yr futures are up 11/32 at 112-17

EURUSD down 0.0012 (-0.1%) at 1.1902

USDJPY down 1.61 (-1.03%) at 154.27

WTI Crude Oil (front-month) down $0.28 (-0.44%) at $64.09

Gold is down $27.34 (-0.54%) at $5030.77

European bourses closing levels:

EuroStoxx 50 down 11.95 points (-0.2%) at 6047.06

FTSE 100 down 32.39 points (-0.31%) at 10353.84

German DAX down 27.02 points (-0.11%) at 24987.85

French CAC 40 up 4.6 points (0.06%) at 8327.88

US TREASURY FUTURES CLOSE

Curve update:

3M10Y -6.103, 45.68 (L: 45.148 / H: 50.552)

2Y10Y -2.617, 68.665 (L: 68.368 / H: 71.504)

2Y30Y -4.003, 132.89 (L: 132.694 / H: 137.102)

5Y30Y -2.663, 108.522 (L: 108.333 / H: 111.122)

Current futures levels:

Mar 2-Yr futures up 1.625/32 at 104-12 (L: 104-09.75 / H: 104-12.5)

Mar 5-Yr futures up 5.75/32 at 109-10.75 (L: 109-04 / H: 109-12.25)

Mar 10-Yr futures up 11/32 at 112-17 (L: 112-05 / H: 112-19)

Mar 30-Yr futures up 31/32 at 116-17 (L: 115-13 / H: 116-20)

Mar Ultra futures up 1-07/32 at 119-4 (L: 117-21 / H: 119-08)

MNI US 10YR FUTURE TECHS: (H6) Challenging Bearish M/T Condition

- RES 4: 112-31 High Dec 18 and key short-term resistance

- RES 3: 113-04 76.4% retracement of the Nov 25 - Jan 20 bear leg

- RES 2: 112-22 High Jan 7

- RES 1: 112-19 High Feb 10

- PRICE: 112-16+ @ 17:34 GMT Feb 10

- SUP 1: 111-29/09 20-day EMA / Low Jan 20 and the bear trigger

- SUP 2: 111-00 Round number support

- SUP 3: 110-30+ 1.618 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 110-22+ 1.764 proj of the Oct 17 - Nov 5 - 25 price swing

A sharp rally in Treasuries last Thursday helped clear out resistance on the rally to 112-16+, and prices have gained again Tuesday, topping out at 112-19. Much of this week’s strength comes off the back of the break of the 20- and 50-day EMAs, with 112-22 the next notable resistance. This week’s price action challenges the bearish M/T condition - and only a reversal lower here and break of 111-09, the Jan 20 low, can resume the bear cycle.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 +0.015 at 96.410

Jun 26 +0.020 at 96.635

Sep 26 +0.020 at 96.825

Dec 26 +0.025 at 96.905

Red Pack (Mar 27-Dec 27) +0.030 to +0.045

Green Pack (Mar 28-Dec 28) +0.050 to +0.050

Blue Pack (Mar 29-Dec 29) +0.050 to +0.055

Gold Pack (Mar 30-Dec 30) +0.050 to +0.055

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.63% (-0.01), volume: $3.132T

- Broad General Collateral Rate (BGCR): 3.61% (-0.01), volume: $1.322T

- Tri-Party General Collateral Rate (TCR): 3.61% (-0.01), volume: $1.299T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $207B

FED Reverse Repo Operation

RRP usage inches up to $1.447B with 5 counterparties this afternoon vs. $1.306B Monday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $4B Disney, $3B Cencora 5Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 02/10 $4B #Walt Disney $1B 3Y +28, $500M 3Y SOFR+47, $1.5B 5Y +40, $1B 10Y +58

- 02/10 $3B #Cencora $500M 3Y +48, $500M -5Y +60, $500M 7Y +70, $1B 10Y +80, $500M 30Y +90

- 02/10 $2.5B *Bank of England 3Y +5

- 02/10 $1.25B #Sysco $600M +5Y +70, $650M 10Y +85

- 02/10 $800M #Pulte Group $400M 5Y +62, $400M 10Y +87

- 02/10 $750M #Alexandria Real Estate 10Y +115

- 02/10 $750M #IADB 5Y SOFR+28

- 02/10 $500M #Cousins Property 7Y +108

- 02/10 $500M #Loews Corp 10Y +80

- 02/10 $500M #Tyson 10Y +85

- 02/10 $Benchmark Dominican Republic 8Y 6.1%a, 12.25Y 6.5%a

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Strengthen, But Continue To Lag Peers

Gilts once again underperformed Bunds, within a broad curve flattening move across European FI Tuesday.

- Long-end Gilts continued their recovery following vocal support in Monday's session by government ministers for PM Starmer, thereby alleviating near-term fiscal concerns.

- Despite being apparently weighed down by heavy sovereign and corporate supply, Bunds continued to track global peers and outperformed Gilts.

- Indeed, EGBs and Gilts tracked a Treasury rally in afternoon trade, with US data including retail sales and labour costs coming in softer-than-expected.

- On the day, the German curve bull flattened, with the UK's twist flattening.

- Periphery/semi-core EGB spreads were little changed.

- Wednesday's global focus will be the US employment report, though we also get the ECB's latest wage tracker and plenty of sovereign supply including a French syndication.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.9bps at 2.069%, 5-Yr is down 2.3bps at 2.383%, 10-Yr is down 3.2bps at 2.808%, and 30-Yr is down 3.7bps at 3.49%.

- UK: The 2-Yr yield is up 1.7bps at 3.643%, 5-Yr is down 0.6bps at 3.894%, 10-Yr is down 2.1bps at 4.506%, and 30-Yr is down 2.1bps at 5.325%.

- Italian BTP spread down 0.6bps at 60.5bps / French OAT down 0.8bps at 59.8bps

MNI OPTIONS: Sizeable Call Structures Cross Again, Including Euribor CFly

Tuesday's Europe rates/bond options flow included:

- DUH6 106.90/107.00cs 1x2, bought for 1 in 2.4k

- OEH6 116.75/117.5/117.75/119.25 call condor v 116/115.25 put spread, sells the condor at 15-13.5 in 14.9k

- ERH6 98.00/98.0625/98.12c fly, bought for 0.25 in 20k

- SFIM6 96.65/96.75/96.85/96.95c condor, bought for 2.75 in 5k

- SFIU6 96.75/0/96.50ps 1x2, sold at 6.5 in 19.5k (19.5kx39k)

- SFIZ6 96.60 puts 12K sold at 10.0

MNI FOREX: Japanese Yen Extends Post-Election Rally, NOK Firms Following CPI

- Japanese assets have firmed on Tuesday, bolstered by comments from Finance Minister Katayama, who appears to have successfully calmed the markets on the timing and financing of the sales tax cut. Stabilisation across the JGB curve has facilitated an extension of the Japanese yen rebound, with the USDJPY pullback from yesterday’s post-election high reaching 2.35% at today’s 154.06 low.

- Softer-than-expected US retail sales data appeared to have exacerbated the USDJPY decline, although the dollar has shown much broader stability against other G10 currencies. This dynamic has allowed cross/JPY to fall sharply, with the likes of GBPJPY and AUDJPY leading the declines.

- The sharp downswing for the GBPJPY today has seen spot narrow the gap substantially to the 50-day EMA, which intersects at 210.58. This average is notable given the fact we have not posted a daily close below it since October, and it acted as perfect support on Jan 26.

- The lack of any meaningful bounce for USDJPY following the US data despite broader greenback stability may leave the pair vulnerable to a further acceleration as we approach tomorrow’s US employment report. The next support of note is at 152.10, the Jan 27 low.

- In Norway, the January acceleration in CPI-ATE looks broad-based, with start-of-year price resets in the likes of rents and insurance highlighted. Any scope for payback in February won't be enough to ease Norges Bank concerns around inflation persistence, which leads EURNOK 0.65% lower on the session to fresh lows for 2026, narrowing the gap to support at the 2025 lows of 11.2614.

- Gradual downside momentum for EURCHF has been building in recent sessions. Session lows of 0.9095 represent the first test below 0.9100 since the removal of the peg in 2015.

- All focus turns to tomorrow’s US employment data. The report will need to be assessed holistically rather than focusing on any single number, although the unemployment rate should offer the cleanest single take.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 11/02/2026 | 0900/1000 | * | Industrial Production | |

| 11/02/2026 | 1020/1120 | ECB's Cipollone In Digital Finance Conference Fireside Chat | ||

| 11/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 11/02/2026 | 1330/0830 | * | Building Permits | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | *** | Employment Report | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1330/0830 | ** | Final CES Benchmark Revision | |

| 11/02/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 11/02/2026 | 1515/1015 | Fed Vice Chair Michelle Bowman | ||

| 11/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 11/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 11/02/2026 | 1700/1800 | ECB's Schnabel Lecture At Austrian Academy of Sciences | ||

| 11/02/2026 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/02/2026 | 1830/1330 | Bank of Canada meeting minutes | ||

| 11/02/2026 | 1900/1400 | ** | Treasury Budget | |

| 11/02/2026 | 2100/1600 | Cleveland Fed's Beth Hammack |