US DATA: Wage Growth Moderation Continued In Q4 ECI Report

The Q4 ECI update continued a trend moderation in wage growth. This more comprehensive wage growth metric, which the Fed puts much more weight on when it comes to assessing wage dynamics, offers a softer take than hourly earnings data in recent monthly payrolls reports.

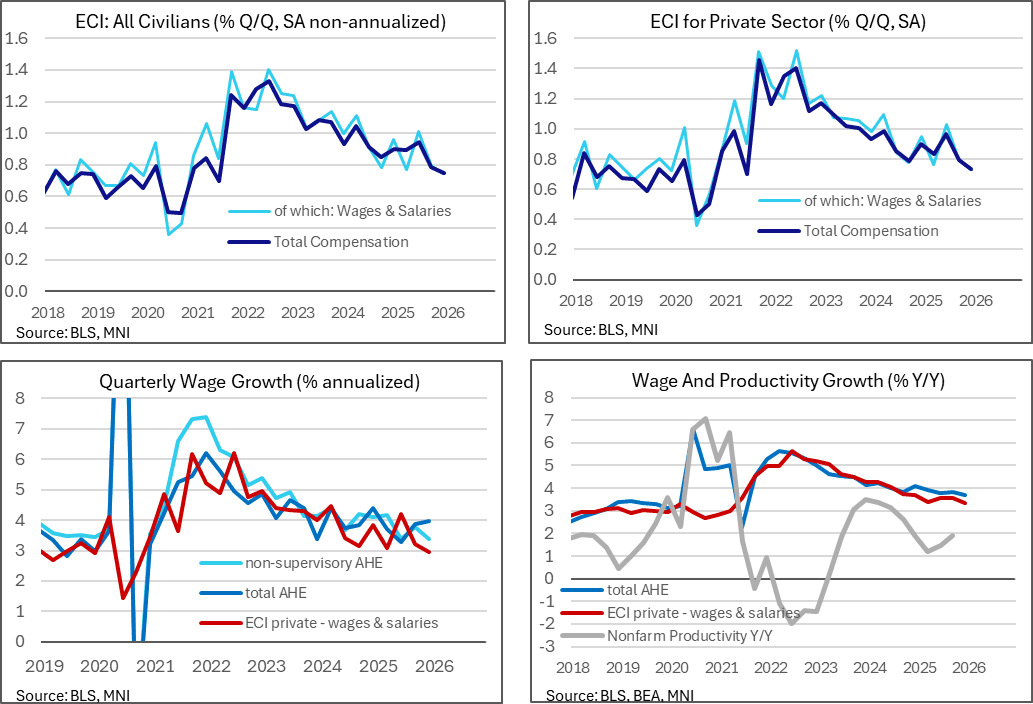

- The employment cost index was on the soft side of expectations in Q4 as it increased 0.75% Q/Q non-annualized (cons 0.8) after 0.79%.

- It left annualized growth of 3.0% annualized in Q4 for its softest since 2Q21 after 3.2% in Q3, 3.8% in Q2 and 3.6% in Q1.

- The wages & salaries component told the same story, easing to 3.0% annualized in Q4 after 3.2% in Q3, with the private sector-only version also at 3.0% after 3.2%.

- These comprehensive wage growth metrics show a more modest backdrop than the average hourly earnings data from the monthly payrolls report, with its 4.0% annualized in Q4 after 3.9% in Q3 in the latest vintage before Wednesday’s update for January. The non-supervisory component, accounting for approximately 80% of employees is a little closer to ECI metrics but still stronger at 3.4% in Q4 after 3.8% in Q3.

- Coupled with still robust productivity growth (4.9% annualized or 1.9% Y/Y in Q3) and nominal wage growth closer to 3% in 2H25 has started to point to disinflationary pressures stemming from the labor market.

- The return to nominal wage growth rates closer to the pre-pandemic period follows quit rates easily falling back into pre-pandemic ranges for some time now.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore