BONDS: Japanese Investors Sold OATs In December, Foreigners Buying Domestic Debt

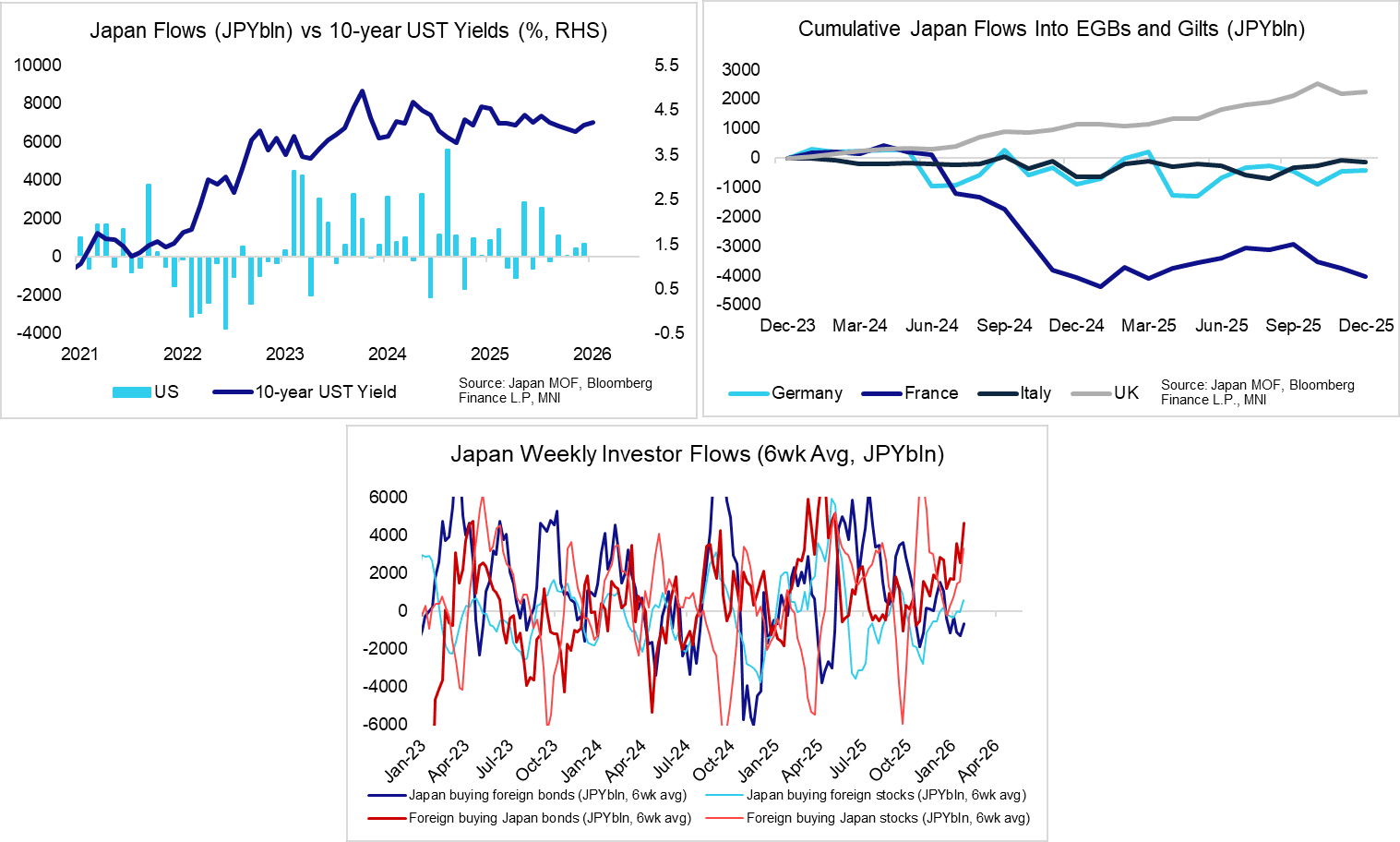

Japanese balance of payments data for December was released yesterday. There wasn’t clear evidence of broad-based foreign bond shedding by domestic investors. The January data may be more interesting given the historic rise in domestic yields, amid familiar fiscal/issuance concerns. More timely weekly data suggests domestic investors were net sellers of foreign bonds in the 6 weeks to Jan 30, but foreign purchases of domestic stocks and bonds presented a far more material dynamic (see chart).

- Japanese investors continued selling French bonds in December, amid acute political/budget uncertainty seen through Q4. Investors net sold JPY2734bln of French bonds, after JPY226bln of net sales in November and JPY576bln in October. A reminder that French political uncertainty subsided notably in January, after PM Lecornu was able to pass the 2026 budget without falling to a censure vote.

- Meanwhile, there were small net purchases of German bonds and small net sales of Italian bonds in December.

- Elsewhere, Japanese investors resumed their purchases of UK bonds in December (JPY56bln) after November saw net sales of JPY351bln in the lead-up to the Autumn budget.

- To end 2025, Japanese investors net purchased JPY711bln of USTs, bringing year-to-date net purchases to JPY7.59trln.

- See below for some analyst views on Japanese portfolio investment flows. These remain in focus following Sunday’s election result:

- Morgan Stanley: “We consider speculation about the possibility of Japan’s pension program increasing its exposure to JGBs (beyond standard rebalancing needs) to be a little overblown, and expect that allocations will continue to depend mostly on the relative performance of each asset class. Taking a holistic view, we believe that the notion that Japanese investors will sell overseas assets and rotate into JGBs is misguided…..“Our impression is that it is probably valuation-sensitive overseas investors who place greatest weight on relative yields. Foreigners have in fact been increasing their allocations to both Japanese equities and Japanese bonds significantly of late"

- Santander: “The recent sell-off in Japanese rates has sharply narrowed both outright and in FX hedged yield pick-ups of foreign bonds versus JGBs. In our view, this is more likely to slow Japanese investors’ overseas bond purchases and redirect flows towards domestic bonds than to trigger outright selling of USTs or EGBs, but it is still significant given Japan’s role as the world’s largest net creditor”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore