US DATA: Retail Revisions And Control Group Miss Confirm Q4 PCE Slowdown

December's advance retail sales data was roundly weaker than expected, which in addition to lower revisions in prior months will likely mean a pullback in Q4 personal consumption expenditures estimates in the GDP accounts. Even prior to this report, January had been expected to be a weak month for retail sales given incoming indicators, so there will be concerns about the momentum of consumption going into 2025. And the report is in nominal terms, so in volume terms Q4 2025 suddenly looks to have been closer to flat instead of robust for core goods sales.

- The big surprise is that Control Group sales contracted 0.1% M/M in December vs expectations of a 0.4% expansion, for the first drop in 3 months alternate series including Chicago Fed CARTS had pointed to a decent rise. This was compounded by a downward revision to prior (0.2% from 0.4%) and a second consecutive downward revision to October, which originally printed 0.85%, then was revised down to 0.6%, and now to 0.4%.

- The latter will pull down the base effect for core retail sales growth in Q4 and looks likely to be met with a downgrade in Atlanta Fed GDPNow tracking of PCE of 3.07% Q/Q SAAR for overall consumption which would represent a slowdown from 3.5% prior. The first read of Q4 GDP is out February 20.

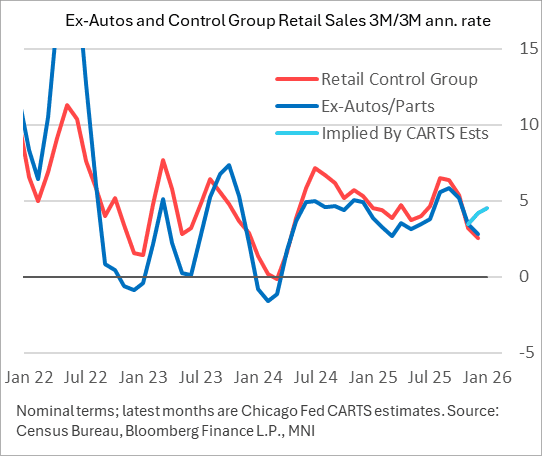

- The 3M/3M annualized rate of Control Group sales is now down to 2.6% in December, vs 6.4% at the end of Q3 (September). If you look at it on a Y/Y basis, sales growth is now just 3.4%, slowest in 19 months. The CARTS estimates in the chart below (which will be revised of course after this release) show how divergent the "actual" data were in December vs expectations.

- Indeed the report brought downgrades across the major aggregates, all of which also missed expectations in December: headline of 0.0% (actually slightly contractionary at -0.02% vs 0.4% survey, 0.4% prior rev from 0.5%) and ex-auto/gas of 0.0% (0.4% survey, 0.3% prior rev from 0.4%).

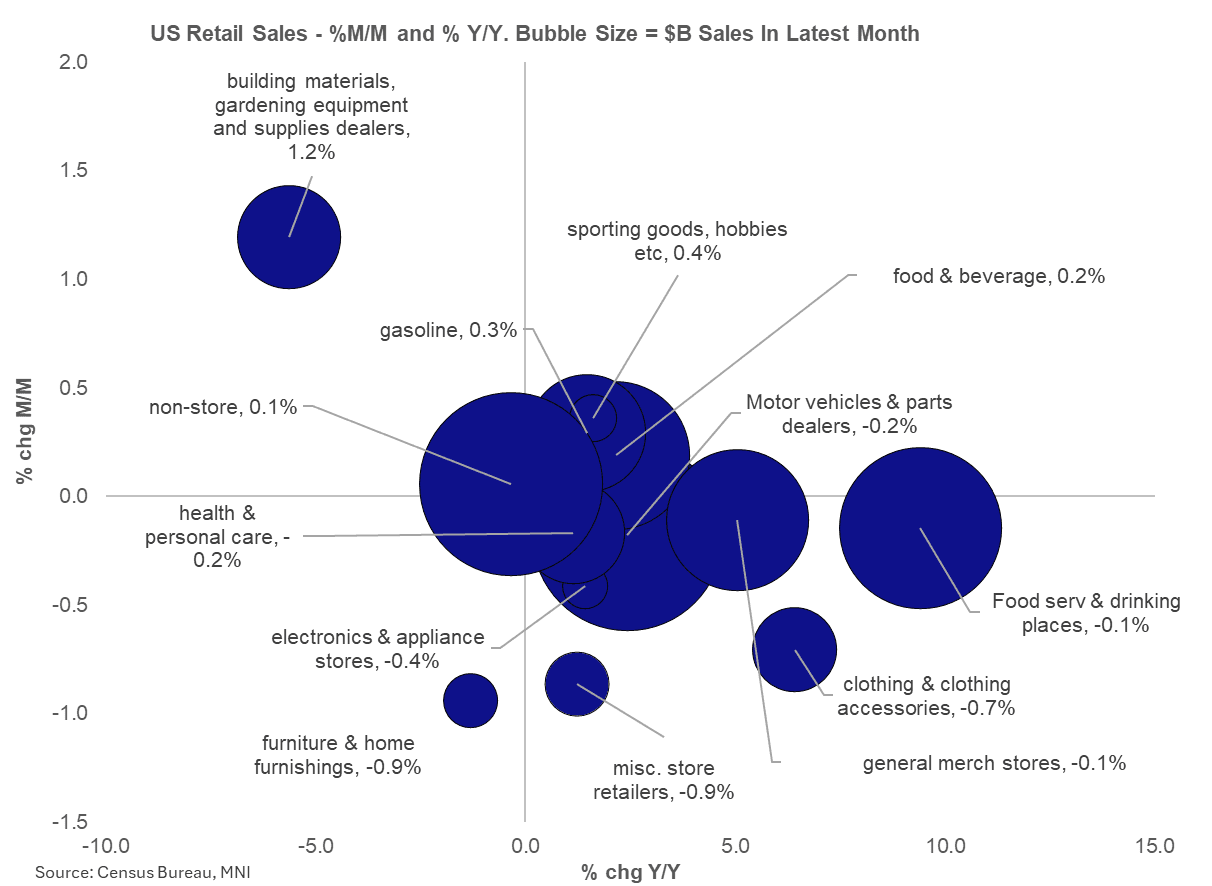

- Looking at the individual categories, December saw an unexpected contraction in vehicle sales (-0.2% M/M, the largest category of retail sales) and food services/dining places (-0.1% after +0.6%), each for the 2nd fall in 3 months (October too).

- Neither of these are in the control group, however: what we did see is broad weakness across major retailer categories, notably non-store (ie internet retailers) flatlining the last 2 months at 0.1% after 0.0% in November; this is the 2nd largest retail sales category and we can't help but note that revisions have been substantial the last couple of months. October was originally reported at +1.8% and November at +0.4%, those readings are now +0.7% and +0.0%, a major component in the overall downward revisions.

- Also general merchandise and miscellaneous stores saw a December contraction, not to mention clothing, furniture, electronics, and health/personal care. We saw a 2nd consecutive strong performance in building materials (1.2% in Nov and Dec) but this isn't in the Control Group.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore