MNI ASIA OPEN: Heavy Data, Yields Rise Ahead April Jobs Data

EXECUTIVE SUMMARY

- MNI SECURITY: US-Ukraine Agreement Hints At Continued US Security Assistance

- MNI US OUTLOOK/OPINION: Payrolls To Lose Weather Boost And Returning Strikers

- MNI US: Trump Reiterates Costly Tax Pledges And Commits To 'Saving Medicaid

- MNI US DATA: Mfg PMI Confidence Lowest Since June vs Highest Inflation In Over 2Y

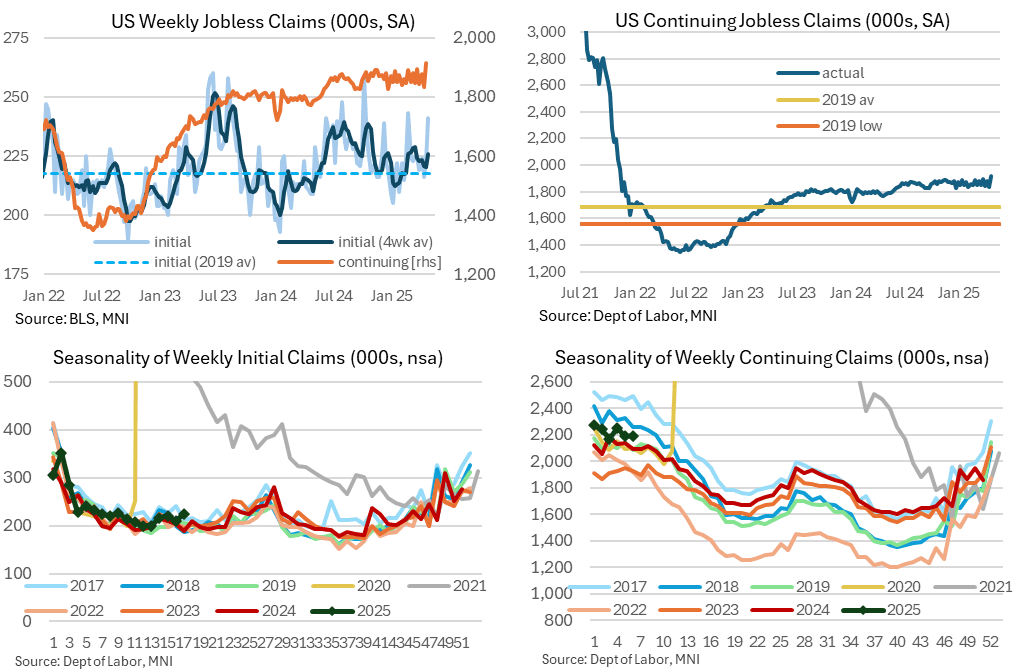

- MNI US DATA: A Rare Surprise Higher For Initial Jobless Claims, Post-Easter Caveat

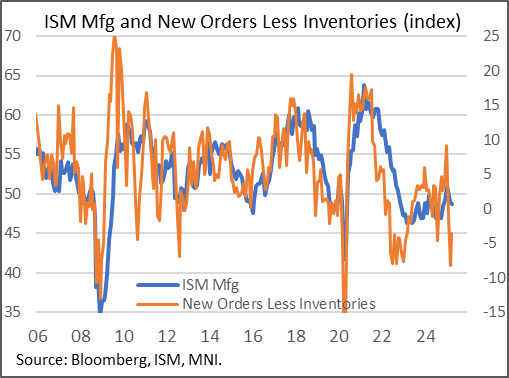

- MNI US DATA: ISM Manufacturing Index Not As Bad As Feared, But Details Are Weak

US

MNI SECURITY: US-Ukraine Agreement Hints At Continued US Security Assistance

Fox News has published the full US-Ukraine reconstruction agreement signed by US Treasury Secretary Scott Bessent and Ukrainian Finance Minister Yuliia Svyrydenko in Washington, D.C, yesterday. The document does not include formal security assurances but inculcates a strategic partnership that the US believes will operate as a deterrent for future Russian aggression.

NEWS

MNI US: National Security Advisor Waltz To Leave Post - CBS

Jennifer Jacobs at CBS reporting on X that US President Donald Trump's National Security Adviser Mike Waltz and his deputy, Alex Wong, "will be leaving their posts," according to "multiple sources familiar with the situation". The news comes after last month's widely-reported controversy over the discussion of sensitive military operational details on the non-governmental messaging platform Signal. Independent journalist Mark Halperin reported earlier today that Waltz and his National Security Council team could be replaced by Trump's frontline negotiator, Steve Witkoff, who has often operated beyond his official remit as special envoy to the Middle East.

MNI US: Trump Reiterates Costly Tax Pledges And Commits To 'Saving Medicaid

US President Donald Trump, speaking at a prayer event in the White House Rose Garden, says he has received an “update” from Congressional leaders on the ‘big beautiful’ Republican reconciliation bill. He notes the bill will be the “biggest ever passed by Congress.” Trump says he had a “really good meeting” with House Speaker Mike Johnson (R-LA), House Majority Leader Steve Scalise (R-LA), Energy, Ways and Means Committee Chair Jason Smith (R-MO), and Energy and Commerce Committee Chair Brett Guthrie (R-KY).

MNI US: House GOP Makes Little Progress In First Week Of Reconcilliation Markups

House Republicans have made little progress in the first week of committee markups towards the ‘big beautiful’ reconciliation bill that will cover President Donald Trump’s tax, spending, energy, and border security agenda. Although House Speaker Mike Johnson (R-LA) says he is targeting a 26 May deadline for completing the House’s work, more realistically, as Johnson confirmed yesterday, the real deadline is the debt limit X date. That date is likely to come in late summer or autumn, but the Treasury Department is yet to publish a formal projection.

MNI UKRAINE: Bessent-Minerals Deal Gives Trump Stronger Hand In Talks w/Russia

Speaking to Fox Business, US Treasury Secretary Scott Bessent says that the US can use the minerals deal signed with Ukraine 'to show the Russian leadership that there is no daylight between the goals of Ukraine and the US'. Says that the partnership will 'accelerate Ukraine's economy'. Bessent claims that the deal 'will allow [President Donald] Trump to negotiate with Russia on a stronger basis.'

MNI SOUTH KOREA: Finance Minister Resigns Amid Impeachment Vote

Choi Sang-mok has resigned as finance minister amid an effort in parliament to impeach him. Choi served as acting president for three months following the impeachment of President Yoon Suk-yeol, and had been slated to serve again following the resignation of Han Duck-soo earlier today, ahead of the acting president's expected presidential bid. The main opposition liberal Democratic Party of Korea (DPK), which holds a majority in the National Assembly, had approved an impeachment bill against Choi.

MNI INDIA: PAKISTAN-Pakistan Army Chief Warns Of 'Military Misadventure'

Wires carrying comments from the chief of the Pakistani army, General Asim Munir, saying that any "military misadventure" by India "will be met with a swift, resolute and notch-up response". Says that Pakistan "remains committed to regional peace, but is prepared to safeguard national interests." Earlier, US Secretary of Defense Pete Hegseth posted on x saying that the US "stands in solidarity with India and support's India's right to defend itself".

US TSYS

MNI US TSYS: Late Stock Retreat, Join Treasuries, Focus on Earnings, Jobs

- US Treasuries are broadly weaker after the bell (late stock retreat to only mildly higher after Amazon, Eli Lilly & Becton Dickinson sell off), near late session lows as focus turns to Friday morning's April employment report. Volatile early trade as markets reacted more to economic data than trade related headlines.

- Treasuries extended early highs after higher than expected weekly and continuing claims, prior for continuing down-revised. Initial jobless claims increased to 241k (sa, cons 223k) in the week to Apr 26 after a marginally upward revised 223k (initial 222k).

- Rates reversed course, extended lows while stocks rallied - caveats to higher than expected ISM New Orders & Employment data as markets apparently overlooked (very weak report that is consistent with recessionary conditions in the manufacturing sector amid policy uncertainty and a giveback of tariff-front loading production in Q1.)

- Tsy Jun'25 10Y currently 9.5 at 111-29.5 vs. 111-24.5 low (10Y yld climbs to 4.2388% high), technical support well below at 111-07.5 (20-day EMA).

- US$ gained (BBDXY +6.09 at 1229.69) , while Gold sold off sharply (-60.63 at 3228.08). Note: Stocks pared gains into the close, finishing mildly higher: SPX eminis +22. at 5609.25.

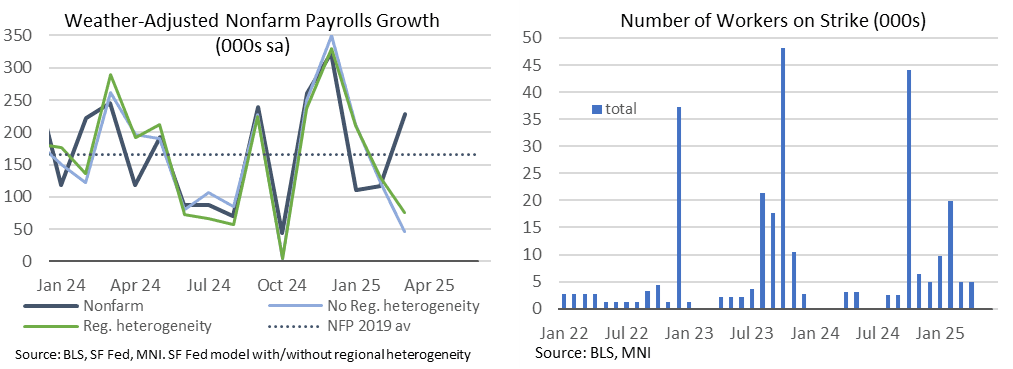

MNI US OUTLOOK/OPINION: Payrolls To Lose Weather Boost And Returning Strikers

- Nonfarm payrolls growth is expected at 135k in April per Bloomberg consensus after a firmly stronger than expected 228k in March. April is likely to lose two tailwinds that were present in March.

- Firstly, we’re unlikely to see a repeat of March’s favorable weather boost. San Francisco Fed staff estimate a huge 152k boost from weather in March after a 14k drag in February and a heavy 100k drag in Jan (using its regional-heterogeneity model). Applying these estimates sees a clear weather-adjusted downward trend in payrolls since a surge in December to 330k, with 211k in Jan, 131k in Feb and just 76k in Mar. These are subjective calculations, with UBS for example seeing a combination of March pull forward and cooler April weather holding April payrolls down by 25-45k after a circa 50k boost in March.

- For a real-time estimate of weather disruption with the April report, we’ll again check the separate household survey question on those not able to work due to bad weather in the reference period. The 87k last month was the lowest for a March since 2000.

- Another positive factor that won’t repeat itself this month is the return of striking workers, with April still seeing 5k on strike in contrast to March seeing a reduction from the 20k in February. On the other hand, some see a temporary positive boost from the timing of a late Easter this year (e.g. Morgan Stanley estimating this at 20k).

OVERNIGHT DATA

MNI US DATA: ISM Manufacturing Index Not As Bad As Feared, But Details Are Weak

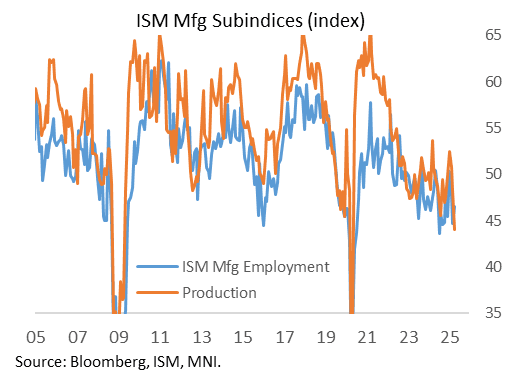

First, the good news from April's ISM Manufacturing report: the headline reading was slightly better than expected at 48.7 (47.9 expected), only a slight downtick from 49.0 in March. There were surprising improvements in both new orders (47.2 vs 45.0 expected, 45.2 prior) and employment (46.5, vs 44.6 expected and 44.7 prior).

- And price pressures didn't rise as much as expected, with the Prices Paid gauge ticking up to 69.8 from 69.4 in March (73.0 had been expected). Indeed the Regional Fed manufacturing gauges had suggested a slightly weaker headline index, with Prices Paid in the 70s. But beyond that, this was a very weak report that is consistent with recessionary conditions in the manufacturing sector amid policy uncertainty and a giveback of tariff-front loading production in Q1.

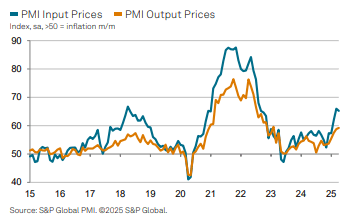

MNI US DATA: Mfg PMI Confidence Lowest Since June vs Highest Inflation In >2 Years

The S&P Global US final manufacturing PMI for April was revised lower to leave no improvement from March, with a second month of only just >50. That does however still look more optimistic than the ISM manufacturing counterpart, at 49.0 in March and due its April release imminently. Confidence is the lowest since June whilst price pressures are clear with the fastest output charge inflation in over two years.

- US S&P Global mfg PMI: 50.2 (cons 50.5, prior 50.7) in April after 50.2 in March.

- Note that the final survey period was 9-25 Apr, for only a slight difference to the 9-22 Apr in the flash release published Apr 23.

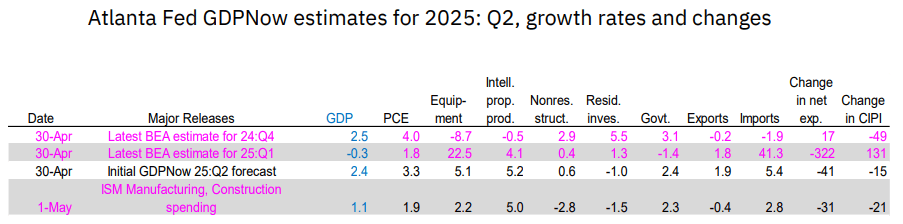

MNI US OUTLOOK/OPINION: Atlanta Fed Q2 GDPNow Pulls Back On Construction, ISM Mfg

The Atlanta Fed's GDPNow estimate for Q2 has dropped sharply to 1.1% Q/Q SAAR from the initial estimate of 2.4% (-0.3% in Q1).

- As we'd pointed out, today's March construction spending report looked weak and of course the April ISM Manufacturing was contractionary, and the latest nowcast reflects relevant downgrades across categories including sharply negative nonresidential and residential investment.

- See graphic from the GDPNow report:

MNI US DATA: A Rare Surprise Higher For Initial Jobless Claims, Post-Easter Caveat

Initial jobless claims surprised higher for the first time since Feb, although with caution needed considering it’s just one week of data and follows a later than usual Easter. We feel the breaking above a well-established range in continuing claims is of greater note but prior increases have seen some downward revisions.

- Initial jobless claims increased to 241k (sa, cons 223k) in the week to Apr 26 after a marginally upward revised 223k (initial 222k).

- That is the first surprise higher since February after an impressive run.

- As always, take single week readings with some caution, especially considering the later timing of Easter this year, whilst noting that the four-week average of 226k. The latter is up from 221k but is still low historically (for example, it averaged 218k without controlling for strong population growth since then).

- Continuing claims meanwhile were more notable as they broke above a range established since late 2024, with 1916k (cons 1865k) in the week to Apr 19 after a downward revised 1833k (initial 1841k).

- These were last above 1900k in Nov 2021 although have had a tendency to being revised lower when probing recent highs.

- One side point ahead of tomorrow’s NFP release: the downward revision to continuing claims makes for a more favorable comparison to prior payrolls reference periods. The 1833k compares with 1847k in both Mar and Feb and 1849k in Jan.

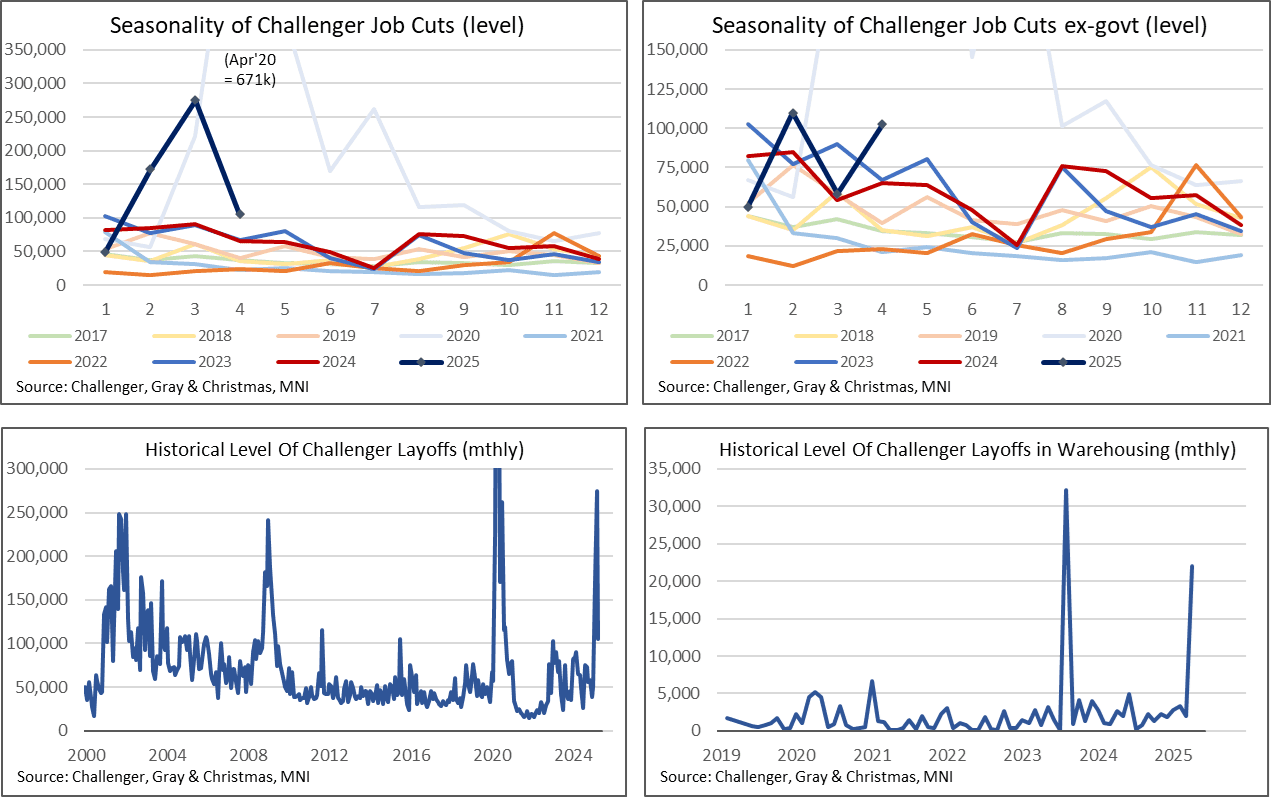

MNI US DATA: Hard to Directly Pin Tariffs On High Challenger Job Cut Announcements

Challenger job cut announcements pulled back in April from particularly high readings with the peak contribution from DOGE actions behind us, but were still high historically with large contributions from tech and warehousing. Press release details show that whilst cut announcements over the first four months of the year are 87% higher than in 2024, strip out direct “DOGE actions” and this would have been -1% suggesting little spillover to other industries from DOGE activity or tariffs.

- Challenger job cut announcements fell back to 105k in April after some particularly high DOGE-related readings of 275k in March (of which 217k govt) and 172k in Feb (62k govt). That is still a 63% Y/Y increase though, compared to 30% Y/Y averaged in 4Q24, 21% in 3Q24 and -2% in 1H24.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 83.6 points (0.21%) at 40752.96

S&P E-Mini Future up 22.25 points (0.4%) at 5610.25

Nasdaq up 264.4 points (1.5%) at 17710.74

US 10-Yr yield is up 4.4 bps at 4.206%

US Jun 10-Yr futures are down 7/32 at 112-0

EURUSD down 0.0034 (-0.3%) at 1.1293

USDJPY up 2.28 (1.59%) at 145.36

WTI Crude Oil (front-month) up $0.79 (1.36%) at $59.00

Gold is down $54.81 (-1.67%) at $3233.91

European bourses closing levels:

EuroStoxx 50 down 0 points (0%) at 5160.22

FTSE 100 up 1.95 points (0.02%) at 8496.8

US TREASURY FUTURES CLOSE

3M10Y +3.423, -9.491 (L: -18.549 / H: -6.406)

2Y10Y -4.161, 51.35 (L: 50.928 / H: 58.572)

2Y30Y -4.916, 102.04 (L: 101.425 / H: 112.845)

5Y30Y -2.646, 92.281 (L: 90.961 / H: 100.027)

Current futures levels:

Jun 2-Yr futures down 4.75/32 at 103-29.625 (L: 103-27.625 / H: 104-06)

Jun 5-Yr futures down 6/32 at 109-0.25 (L: 108-26.75 / H: 109-16.25)

Jun 10-Yr futures down 6.5/32 at 112-0.5 (L: 111-24.5 / H: 112-20.5)

Jun 30-Yr futures down 14/32 at 116-6 (L: 115-24 / H: 117-07)

Jun Ultra futures down 18/32 at 120-15 (L: 119-27 / H: 121-22)

MNI US 10YR FUTURE TECHS: (M5) Sold Hard Off Highs

- RES 4: 113-22 1.382 proj of the Apr 11 - 16 - 22 price swing

- RES 3: 113-04 76.4% retracement of the Apr 7 - 11 bear leg

- RES 2: 112-20+ Intraday high

- RES 1: 112-18 1.0% 10-dma envelope

- PRICE: 111-27+ @ 1515 ET May 1

- SUP 1: 111-07+ 20-day EMA

- SUP 2: 110-16+/109-08 Low Apr 22 / 11 and the bear trigger

- SUP 3: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 4: 108-21 Low Feb 19

Treasury futures reversed off the intraday high on firmer-than-expected ISM Manufacturing data. Prices saw pressure toward the first real support at the 20-day EMA of 111-07+, below which 110-16+ marks the Apr 22 low and next notable downside level. Recent gains resulted in a break of 111-25, 50.0% of the Apr 7 - 11 bear leg. However, the lack of follow through here shows the bullish S/T trend signal may be under threat. The bear trigger remains 109-08, the Apr 11 low.

SOFR FUTURES CLOSE

Jun 25 -0.030 at 95.885

Sep 25 -0.080 at 96.285

Dec 25 -0.10 at 96.595

Mar 26 -0.110 at 96.80

Red Pack (Jun 26-Mar 27) -0.10 to -0.065

Green Pack (Jun 27-Mar 28) -0.055 to -0.03

Blue Pack (Jun 28-Mar 29) -0.03 to -0.02

Gold Pack (Jun 29-Mar 30) -0.025 to -0.015

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.41% (+0.05), volume: $2.830T

- Broad General Collateral Rate (BGCR): 4.37% (+0.02), volume: $1.088T

- Tri-Party General Collateral Rate (TCR): 4.37% (+0.02), volume: $1.047T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $92B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $215B

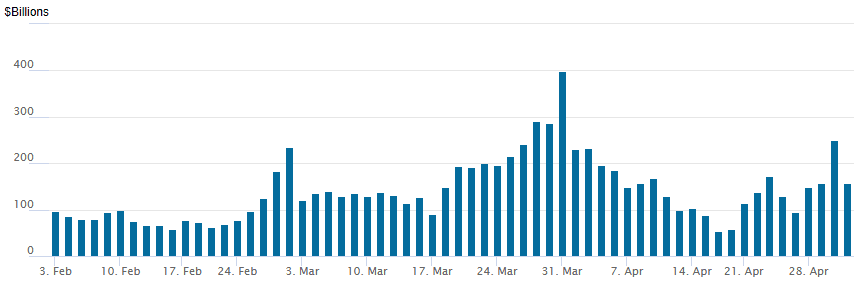

FED Reverse Repo Operation

RRP usage retreats back to $157.353B this afternoon from $250.601B yesterday. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B. The number of counterparties at 37.

MNI PIPELINE: Corporate Bond Update: $5.35B Citigroup 4Pt Launched

$9.75B total to price Thursday:

- Date $MM Issuer (Priced *, Launch #)

- 05/01 $5.35B #Citigroup $2.35B 3NC2 +95, $700M 3NC2 SOFR, $2B 6NC5 +115, $300M 6NC5 SOFR

- 05/01 $1.6B #Mondelez $700M 3Y +65, $500M 5Y +80, $400M 10Y +95

- 05/01 $800M #MassMutual Global 5Y +80

- 05/01 $500M #Coca-Cola Femsa 10Y +93

- 05/01 $500M #ERP Operating LP 7Y +98

- 05/01 $500M #Marex Group 3Y +215

- 05/01 $500M #EQT 10Y +165

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Bear Steepen With EGBs On Holiday

Gilt yields rose sharply Thursday, with EGB trade closed for the May 1 European holiday.

- With much of Europe off, market focus was entirely on the UK.

- Gilts traded steadily through the morning session, with the short end outperforming as oil prices receded, and ticking higher on higher-than-expected US jobless claims data,

- But they turned sharply lower two hours before the cash close as the US ISM Manufacturing index was not as bad as feared. The selloff accelerated into the cash close, led by Treasuries.

- UK data included March lending data which showed a burst of mortgage loans (front-running the expiry of a stamp duty cut), while final April manufacturing PMI was slightly upgraded from the preliminary reading but remained contractionary.

- The UK curve bear steepened: The 2-Yr yield is up 1.8bps at 3.821%, 5-Yr is up 2.6bps at 3.943%, 10-Yr is up 4bps at 4.481%, and 30-Yr is up 5.3bps at 5.26%.

- Friday's calendar is highlighted by Eurozone flash April inflation (recall, national data so far suggests upside risks to consensus for core HICP coming into the week).

MNI FOREX: USDJPY Extends Surge Amid Dovish BOJ and Equities Rally

- Despite the plethora of national holidays on Thursday, currency markets have seen significant swings, with the USD index (+0.78%) notably extending its recovery to trade back above the 100 mark ahead of Friday’s US employment report. The yen has significantly underperformed following a dovish tilt from the Bank of Japan and higher US yields/equities providing additional headwinds.

- As such, USDJPY stands 1.65% firmer on the session having extended a clean break of the recovery highs around the 144 handle. The move coincided with a breach of the 20-day EMA which may have also exacerbated the topside momentum. Highs approaching the APAC crossover are seen at 145.65, and represent a 280 pip rally from session lows. Firmer resistance is located at the 50-day EMA, intersecting at 146.72.

- Elsewhere, losses across the G10 space have been broad based against the dollar. The likes of EUR and GBP are roughly half a percent lower, back below 1.13 and 1.33 respectively.

- The recent pullback in EURUSD is considered corrective and the trend structure is unchanged, it remains bullish. Moving average studies are in a bull-mode position signalling a dominant uptrend, and the latest move down is allowing an overbought condition to unwind. Key support is at the 20-day EMA, at 1.1251.

- USDCHF has also strengthened 0.75% today, with the highs of the session once again coinciding with the 2023 breakdown point at 0.8333, and the 20-day EMA. This could increase the pair’s importance ahead of Friday’s release of the US employment report. Elsewhere, flash inflation data for the Eurozone is a calendar highlight on Friday.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 02/05/2025 | 0630/0730 | DMO to announce details of long syndication for W/C 19 May | ||

| 02/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0900/1100 | *** | HICP (p) | |

| 02/05/2025 | 0900/1100 | ** | Unemployment | |

| 02/05/2025 | 1130/2030 | * | Labor Force Survey | |

| 02/05/2025 | 1230/0830 | *** | Employment Report | |

| 02/05/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |