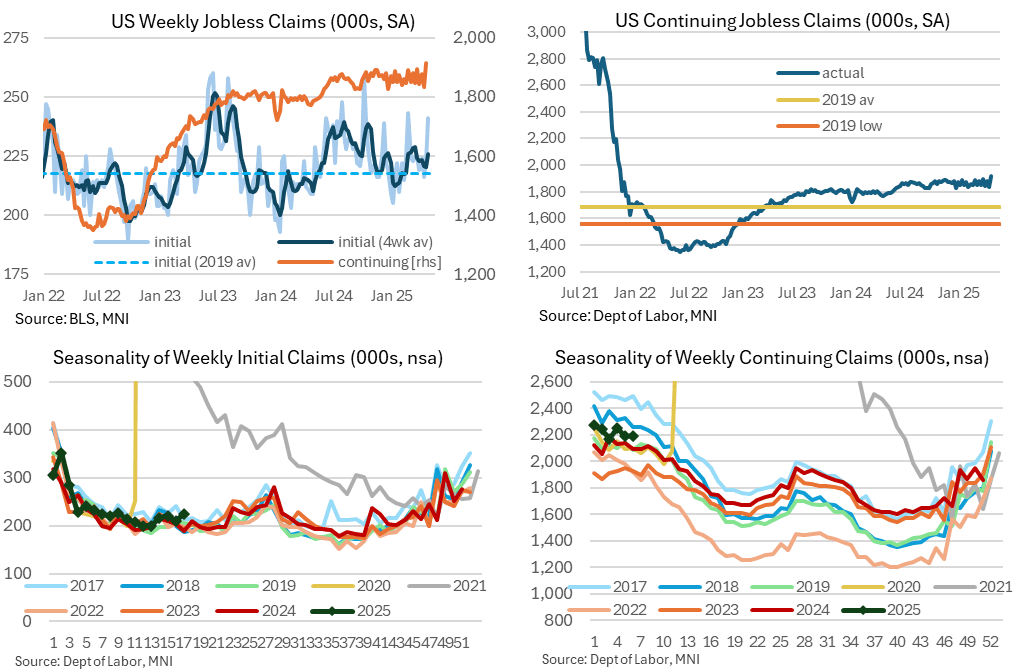

US DATA: A Rare Surprise Higher For Initial Jobless Claims, Post-Easter Caveat

May-01 12:46

Initial jobless claims surprised higher for the first time since Feb, although with caution needed considering it’s just one week of data and follows a later than usual Easter. We feel the breaking above a well-established range in continuing claims is of greater note but prior increases have seen some downward revisions.

- Initial jobless claims increased to 241k (sa, cons 223k) in the week to Apr 26 after a marginally upward revised 223k (initial 222k).

- That is the first surprise higher since February after an impressive run.

- As always, take single week readings with some caution, especially considering the later timing of Easter this year, whilst noting that the four-week average of 226k. The latter is up from 221k but is still low historically (for example, it averaged 218k without controlling for strong population growth since then).

- Continuing claims meanwhile were more notable as they broke above a range established since late 2024, with 1916k (cons 1865k) in the week to Apr 19 after a downward revised 1833k (initial 1841k).

- These were last above 1900k in Nov 2021 although have had a tendency to being revised lower when probing recent highs.

- One side point ahead of tomorrow’s NFP release: the downward revision to continuing claims makes for a more favorable comparison to prior payrolls reference periods. The 1833k compares with 1847k in both Mar and Feb and 1849k in Jan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

INFLATION: EUR 5Y5Y Inflation Swaps Back To Lowest Since Fiscal Shift

Apr-01 12:42

- As noted earlier, Eurozone STIR markets have reversed the hawkish reaction seen on yesterday’s Bloomberg ECB sources piece, aided in part by the Washington Post’s report on potential for 20% tariffs as part of broader concerns ahead of tomorrow’s reciprocal tariffs announcement.

- Yesterday’s hawkish reaction helped stop what had been a modest rise in 5Y5Y inflation swaps (~2bps to 2.125%), although currently at ~2.10% they have reversed that climb along with today’s rates rally.

- It leaves 5Y5Y inflation swaps at what would be the lowest close since the Mar 4 German and EU fiscal announcements, having been at 2.05-2.075% in the days shortly beforehand.

- Those fiscal plans saw idiosyncratic adjustments in EU long-term inflation swaps, narrowing the US-EUR spread from levels closer to 40bps to 16bp on Mar 5. Daily gyrations have more recently shifted back to seeing greater correlation with those in the US though, with a US-EU spread at 30bps +/- 3bps over the past week and a half.

EURIBOR OPTIONS: Call spread vs put

Apr-01 12:38

ERZ5 98.0625/98.25cs vs 97.75p, bought the cs for 2 in 10.5k vs 3.99k at 98.075.

STIR: UPDATE/CORRECTS: Jun'25 SOFR Puts

Apr-01 12:37

- +30,000 SFRM5 95.75 puts, 3.0 ref 95.935 at 0826:16ET, total volumes 72,000 when taking into account +30,000 SFRM5 95.68/95.75/95.87 put trees and other misc trades