US DATA: Hard to Directly Pin Tariffs On High Challenger Job Cut Announcements

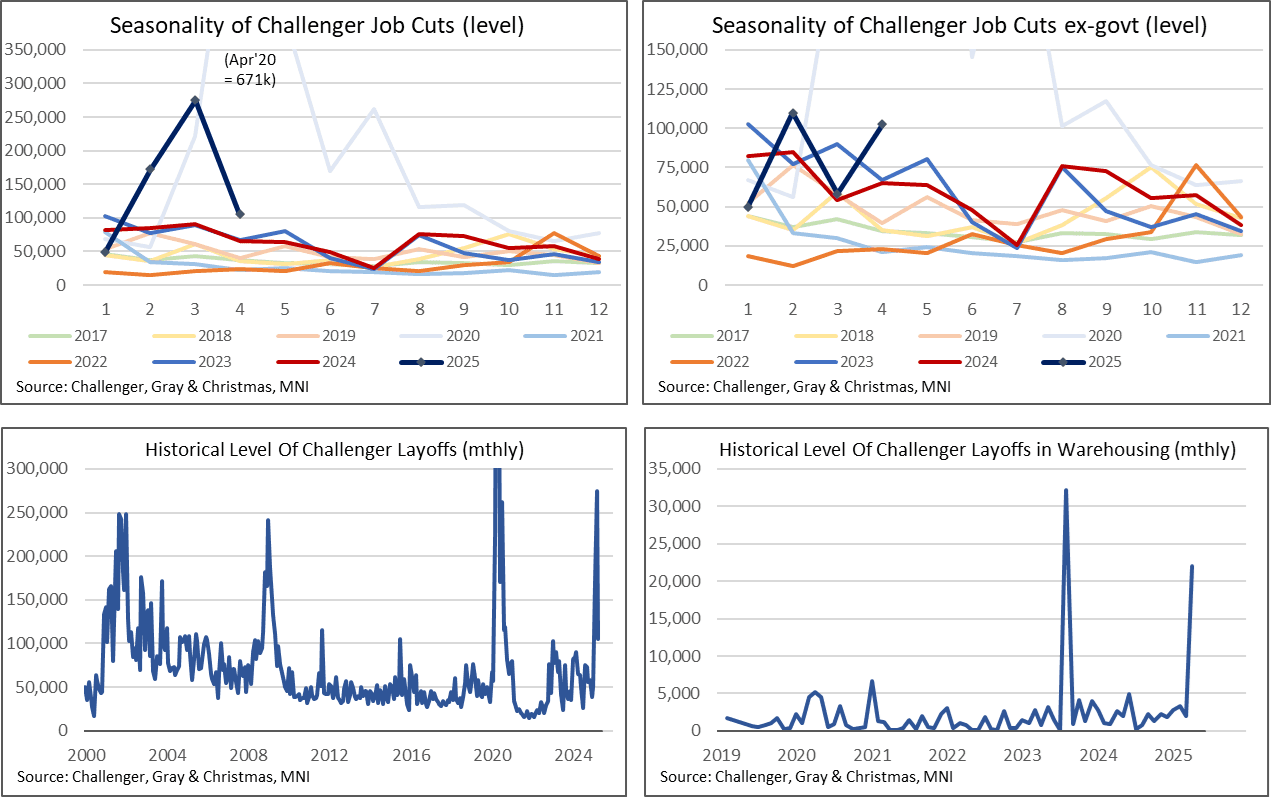

Challenger job cut announcements pulled back in April from particularly high readings with the peak contribution from DOGE actions behind us, but were still high historically with large contributions from tech and warehousing. Press release details show that whilst cut announcements over the first four months of the year are 87% higher than in 2024, strip out direct “DOGE actions” and this would have been -1% suggesting little spillover to other industries from DOGE activity or tariffs.

- Challenger job cut announcements fell back to 105k in April after some particularly high DOGE-related readings of 275k in March (of which 217k govt) and 172k in Feb (62k govt).

- That is still a 63% Y/Y increase though, compared to 30% Y/Y averaged in 4Q24, 21% in 3Q24 and -2% in 1H24.

- With so much attention on tariffs, note the large jump in cut announcements in warehousing to 22k but treat it with caution. That’s the second highest for a series that started in 2019, and averaged 1.9k in 2024, but it’s too soon to tell from just one month of data whether this is a new trend. Further, the press release notes only limited announcements specifically attributed to “tariffs” more broadly in April(although market/economic conditions are a sizeable driver – see below).

- Tech layoff announcements of 27k were the highest since August.

- Government job cut announcements returned to very small levels this month at 2.8k, of which 2.7k were attributed to DOGE actions.

- The press release (in full here) offers a useful summary of reasons for the cumulative 602k layoffs seen in the first four months of the year (vs 322k in the first four months of 2024). Strip out direct “DOGE Actions” and this would have been a very similar 319k:

- ““DOGE Actions” lead all job cut reasons in 2025 with 283,172, 2,919 of which occurred in April.

- Another 6,945 cuts were attributed to “DOGE Downstream Impact” through April, primarily at Non-Profits and Education organizations. These reasons combined (290,117) make up 48% of all job cuts announced so far in 2025.

- Market/Economic Conditions were cited for 95,348 job cuts, as economic uncertainty, consumer spending, and trade difficulties impact US-companies.

- Tariffs were cited for 1,413 cuts so far this year, with 1,350 occurring in April. Restructuring accounted for 67,627, and 60,551 were due to store, unit, or location “Closing.””

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SOFR/Treasury Option Roundup: Calls Bid Ahead Tariff Deadline

Better Treasury call option trade reported overnight, SOFR options look a little more mixed ahead the NY open. April kicks off with underlying futures unwinding yesterday's month/quarter end selling (TYM5 taps 111-27.5, highest since Mar 4). Added support on WaPo report White House aides drafting tariff proposal of appr 20% ahead tomorrow's "Liberation Day" annc (1500ET). Projected rate cuts through mid-2025 rebound from late Monday levels (*) as follows: May'25 at -4.7bp, Jun'25 at -22.3bp (-20.1bp), Jul'25 at -38.6bp (-35.1bp), Sep'25 -56.1bp (-51.4bp).

- Treasury Options:

- 5,200 USM5 119 calls vs. wk1 US 119.5/121 call spds ref 118-18

- 1,000 USK5 120/123/126 call flys ref 118-16

- 8,000 TYK5 112/112.5/113/113.5 call condors ref 111-24.5

- 7,000 Wed wkly TY 111.5/wk1 TY 111.75 call spds

- over 10,200 TYK5 113 calls, 21 last

- 10,000 TYM5 113.5/115.5 call spds ref 111-24

- over 6,700 each: TYK5 111.5 and 112 calls

- over 6,200 TYK5 114 calls 8 last ref 111-22

- 2,000 FVK5 108.75/109 call spds ref 108-11.25

- 8,000 TYK5 113.5/115 call spds ref 111-17.5

- SOFR Options:

- 4,000 SFRQ5 95.50/95.68/95.87 put flys ref 96.225

- 2,100 SFRM5 95.37/95.62 put spds vs. 96.37/96.62 call spds

- 3,200 SFRM5 95.75/95.87/95.93 put trees

- 3,000 SFRU5 96.25/96.50 call spds

- 1,500 SFRU5 95.25/95.50/95.75/96.00 put condors ref 96.22

- 10,000 SFRM5 96.06/96.18 call spds vs. 2QM5 96.75/96.87 call spds

- 2,000 SFRM5 95.62/95.68 put spds ref 95.925

- Block/screen, 6,000 SFRM5 96.12/96.50 call spds, 3.5 ref 95.915

- 2,000 0QM5 97.00 calls vs. 2,500 97.50 calls ref 96.595

- 1,500 2QJ5 96.75 calls ref 96.58

EUROZONE DATA: Solid Labour Market Prior To Potential Tariff Hit

- Looking at today’s labour data more closely, they continue to point to some healthy developments ahead of likely adverse effects from US tariffs.

- As noted earlier, the unemployment rate surprisingly pushed a tenth lower to a new series low of 6.1% in February. Whilst the rounded data can make it hard to get a sense of the scope of the latest improvement, we note that it came with a solid 70k monthly decline in the seasonally adjusted level of unemployment.

- This follows two less promising months, after a modest 30k decline in January and a rare 49k increase in December at what was its largest increase since Jan 2024.

- The limited details available in this monthly release show the latest drop in unemployment came from those >25 years old, down 82k for the largest monthly decline since Aug 2024.

- That kept the >25yrs unemployment rate unchanged on a rounded basis at 5.3%, a joint series low where it’s been in three of the latest four months of data, having averaged 6.75% in 2019 for comparison.

- This is against a backdrop of a stabilisation in participation rates in 2024 according to quarterly data to Q4 after strong increases compared to pre-pandemic levels. That stabilisation in participation rates has come as employment and labour growth moderated to 1% Y/Y and below, with the stronger pace of employment continuing to see the employment-to-population rate trend higher into Q4.

FOREX: USD Strength Pervades, EUR/USD Through Yesterday's Lows

USD strength pervades well into the NY crossover, helping pressure EUR/USD through yesterday's lows at 1.0784, aided lower by renewed weakness for stocks. The e-mini S&P is through the overnight low and has shed 35 points since the publication of the Washington Post piece pointing at the potential for 20% tariffs.

- JPY gains are outpacing the USD rally given the phase of risk-off, and spot weakness through Y149.00 here would open Y148.70 support and the lowest levels since March 21st.

- We noted yesterday the very healthy currency futures volumes for a Monday - it's more mixed Tuesday, with activity lighter than average for JPY futures, but more active in GBP and EUR markets.