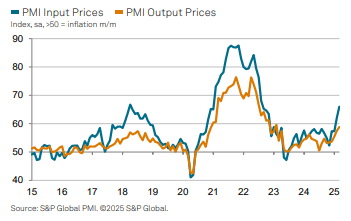

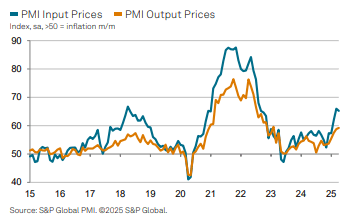

US DATA: Mfg PMI Confidence Lowest Since June vs Highest Inflation In >2 Years

The S&P Global US final manufacturing PMI for April was revised lower to leave no improvement from March, with a second month of only just >50. That does however still look more optimistic than the ISM manufacturing counterpart, at 49.0 in March and due its April release imminently. Confidence is the lowest since June whilst price pressures are clear with the fastest output charge inflation in over two years.

- US S&P Global mfg PMI: 50.2 (cons 50.5, prior 50.7) in April after 50.2 in March.

- Note that the final survey period was 9-25 Apr, for only a slight difference to the 9-22 Apr in the flash release published Apr 23.

Highlights from S&P Global press release (in full here):

- "The US manufacturing sector expanded only marginally in April, amid subdued growth in new work and a further fall in output.

- Although order books were supported by domestic demand, tariffs resulted in heightened uncertainty and a noticeable drop in new export sales. Confidence in the outlook fell to its lowest since last June, while job losses were recorded for the first time in six months.

- On the price front, tariffs reportedly led to steep increases in both input costs and selling prices. Output charges notably rose to the greatest degree in over two years."

Additional comment on tariffs:

- “Tariffs were also reported to have led to some modest supply-side disruptions. Average lead times lengthened for a seventh successive month in April, and to the greatest degree for two-and-a-half years. This was despite a reduction in demand pressure as purchasing activity declined for a second month running. Some firms preferred to utilize their existing inventories in production, which helped to explain a second successive monthly reduction in stocks of purchases.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

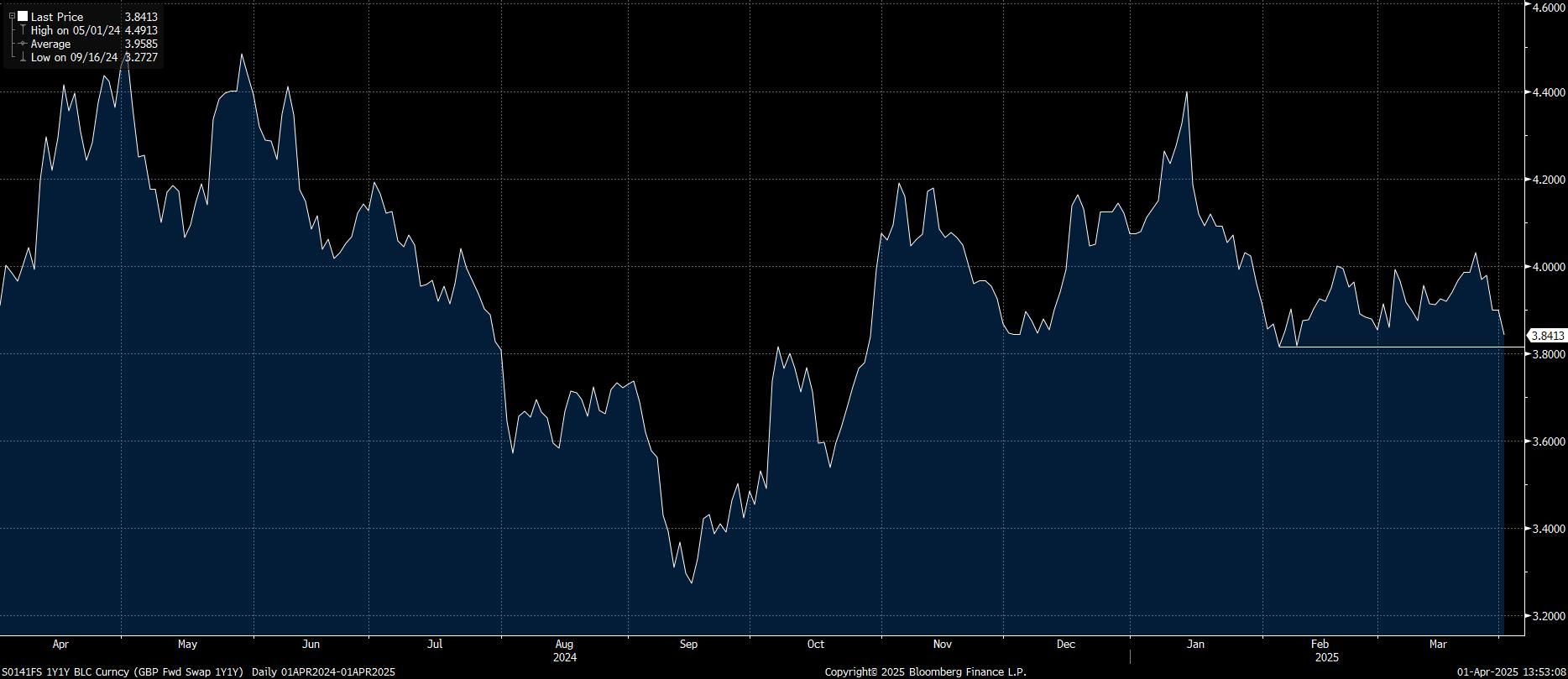

STIR: GBP 1y1y Eyes Feb Lows

Spillover from the move lower in core global yields ahead of “Liberation Day” leaves GBP 1y1y on track to register the first close below 3.85% since February.

- The February closing low/double bottom support area (3.8145%) presents the next notable downside level of interest.

Fig. 1: GBP 1y1y Swap

Source: MNI - Market News/Bloomberg

US TSYS: Post-S&P Global US Manufacturing PMI React

- Treasuries paring gains slightly, still holding higher range after mildly higher than expected S&P Mfg PMI data, stocks pare losses (SPX eminis -5.00 at 5648.25).

- Tsy Jun'25 10Y contract trades 111-18.5 (+11.5), off earlier high of 111-27.5, next technical resistance at 112-01 (High Mar 4 and a bull trigger).

- Curves continue to bull flatten off early week highs: 2s10s -2.694 at 29.105, 5s30s -1.852 at 60.088.

- Cross asset update, Bbg US$ index +.95 at 1275.20, Gold making new highs around 3135.0, crude adding to Monday's rally (WTI +.34 at 71.82.).

- Next up: JOLTS, Construction Spending and ISM mfg data at 1000ET.

US DATA: PMI Mfg Orders Slow, Input Cost Inflation Highest In 2.5 Years

- The manufacturing PMI was revised up slightly in the March final release to 50.2 (cons 49.9, flash 49.8), although still sees a sizeable decline from 52.7 in February (highest since Jun 2022).

- The press releases summarizes the report as: “Production declines in March as order book growth slows on tariff uncertainty”

- It also confirms strong input cost inflation indicated in the flash release, at its highest in “over two-and-a-half years”. The flash release, for both manufacturing and services, had noted that “Input price inflation accelerated sharply, especially in manufacturing, to a near two-year high, often attributed to the impact of tariff policies. However, competition limited the pass-through of higher costs to selling prices.” Here, specifically for manufacturing, output price inflation increased to a 25-month high.

Some highlights from the full press release (here):

- “US manufacturing sector growth stalled in March. Having grown strongly in February, production declined as order books expanded only modestly despite evidence of a stabilization of exports.

- Confidence in the outlook for business activity softened, amid some uncertainty over the impact of federal government policies.

- Employment numbers were unchanged after four months of job gains. Softer trends in output and new orders, plus uncertainty in the outlook, weighed on hiring decisions.

- Cost pressures intensified, largely due to the impact of tariffs, with input price inflation rising to its highest level in over two-and-a-half years.”

- Further on prices: “The steep increase in input prices fed through to a greater rise in manufacturing selling prices during March. Latest data showed that output price inflation picked up for a fourth successive month to a 25-month high.”