US DATA: ISM Manufacturing Index Not As Bad As Feared, But Details Are Weak

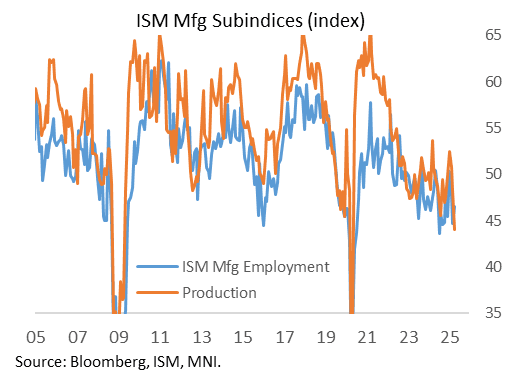

First, the good news from April's ISM Manufacturing report: the headline reading was slightly better than expected at 48.7 (47.9 expected), only a slight downtick from 49.0 in March. There were surprising improvements in both new orders (47.2 vs 45.0 expected, 45.2 prior) and employment (46.5, vs 44.6 expected and 44.7 prior).

- And price pressures didn't rise as much as expected, with the Prices Paid gauge ticking up to 69.8 from 69.4 in March (73.0 had been expected). Indeed the Regional Fed manufacturing gauges had suggested a slightly weaker headline index, with Prices Paid in the 70s.

- But beyond that, this was a very weak report that is consistent with recessionary conditions in the manufacturing sector amid policy uncertainty and a giveback of tariff-front loading production in Q1.

- While the headline index beat expectations, it was flattered by an acceleration in Supplier Deliveries (55.2 vs 53.5 prior) and a still-positive reading in Inventories (50.8 vs 53.4 prior), the 2 categories of the 5 that make up the ISM index, and as the report put it: "Slower supplier deliveries and slightly expanded inventories in April are not considered positives for the economy: Both conditions figure to be temporary and are driven by tariff concerns, either delaying buyer/seller negotiations or advancing material deliveries that will be reversed after tariffs are deployed, leading to a drawdown of manufacturing inventory."

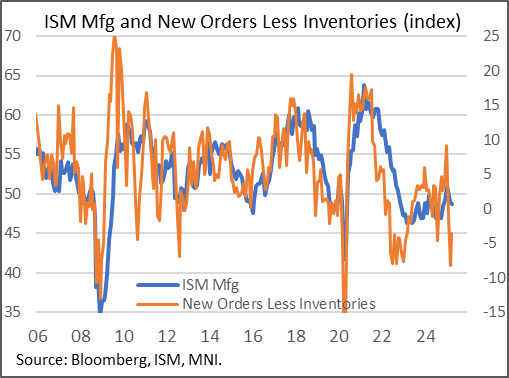

- Inventories in particular still look like they have a large overhang after being in contractionary territory for much of 2023-24. The report notes "Inventory growth is not a positive sign when demand is moving in the opposite direction; the recent expansion is considered a temporary move to avoid tariffs, and levels will decline when such trade issues are resolved. " New Orders less inventories may have picked up from March's lows but they remain contractionary.

- The ISM overall assesses both output and demand as having "weakened" in the month. Production (-4.3 points to 44.0) and New Export Orders (-6.5 to 43.1) fell the most of any categories, both at post-May 2020 lows (ex-Covid period, export orders were the weakest since the Global Financial Crisis), while Backlogs also declined and customers' inventories remained in "too low" territory.

- On employment, the report noted somewhat ominously that "Companies generally opted for layoffs because they are quicker to implement than attrition." And prices, while not increasing as much as expected, were still the highest since June 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT AUCTION PREVIEW: On offer next week

The DMO has announced it will be looking forward to sell GBP2.25bln of the 4.375% Jul-54 Gilt (ISIN: GB00BPSNBB36) at its auction next Tuesday, April 8.

PIPELINE: Kommunalbanken Norway 4Y SOFR Upsized & Launched

- Date $MM Issuer (Priced *, Launch #)

- 04/01 $1B *DBJ 5Y SOFR+59

- 04/01 $850M #Kommunalbanken Norway 4Y SOFR+41 (upsized from $500M)

- 04/01 $500M Nexa WNG 12Y +250

- 04/01 $Benchmark LPL Holdings 3Y +135a, 5Y +150a, 10Y +187a

- 04/01 $Benchmark Realty Income 10Y +145a

- 04/01 $Benchmark NRW Bank 5Y SOFR+49a

OAT: Natixis Leave OAT/Bund Call Unchanged After Le Pen Verdict

Natixis note that “the consequences of the Le Pen judgment on the French political landscape are still difficult to predict, but recent polls suggest her ineligibility for the next presidential elections would not be a disadvantage for the National Rally”.

- They maintain their end ’25 10-Year OAT/Bund target at 70bp, with the “risk of snap elections after the summer and uncertainties surrounding the 2026 budget” risking a move to 75-80bp over that horizon.