MNI ASIA OPEN: Broad Based Risk-Off/Trump Sours on China Trade

EXECUTIVE SUMMARY

- MNI US-CHINA: Trump Threatens To Withdraw From Meeting w/Xi And Increase Tariffs

- MNI FED: StL Fed Musalem Open-Minded To Further Easing But Limited Room To Do So

- MNI FED Gov Waller: Labor Market Not Tight, But Notable GDP Vs Payrolls Disconnect

- MNI US DATA: Continuing Claims Look To Have Increased Only Modestly Last Week

- MNI US DATA: No Real Surprises In Preliminary U.Mich Survey For October

US

MNI FED: StL Fed Musalem Open-Minded To Further Easing But Limited Room To Do So

St Louis Fed's Musalem ('25 voter), one of the more hawkish FOMC members, broadly keeps to his position in the committee - we had seen him as likely one of the six dots looking for no further cuts this year after the 25bp last month. He is open-minded to further easing but there is limited room to do so.

- Paraphrasing: "I supported a 25bp cut in September as a way to provide insurance against labor market weakening, while continuing to lean against inflation. I now perceive monetary policy as somewhere between modestly restrictive and neutral. Looking ahead, I am open-minded about a potential further reduction in interest rates to provide further insurance against labor market weakening. I believe we have to tread with caution because there is limited room for further easing before mon pol could become overly accommodative. I believe monetary pol should continue to lean against persistence in inflation, whether that comes from tariffs, a lower growth in labor supply or for any other reason."

MNI FED Gov Waller: Labor Market Not Tight, But Notable GDP Vs Payrolls Disconnect

In his first comments on monetary policy since the September FOMC meeting, Gov Waller (dove, permanent FOMC voter and reportedly a Fed Chair finalist) interviewed on CNBC Friday unsurprisingly affirmed his view that the Fed should follow through with a series of cuts in light of developing labor market weakness (saying the labor market is "not tight in any way, shape or form"). While it's clear he's among the most dovish members on the Committee, eyeing 2 more rate cuts this year, he doesn't advocate too aggressive an easing: "I'm still in the belief we need to cut rates, but we need to kind of be cautious about it."

NEWS

MNI US-CHINA: Trump Threatens To Withdraw From Meeting w/Xi And Increase Tariffs

US President Donald Trump has threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping, in a lengthy statement on Truth Social, citing a letter from Beijing which he claims lays out new rare earth export control measures.

- Trump writes that China is, “becoming very hostile” regarding export controls on rare earths and “virtually anything else they can think of, even if it’s not manufactured in China.” Trump says, “Our relationship with China over the past six months has been a very good one, thereby making this move on Trade an even more surprising one,” arguing that Beijing is holding the world “captive” with “monopoly positions.”

MNI US-CHINA: Trump Threatens To Withdraw From Meeting w/Xi And Increase Tariffs

The new Chinese rare earth export control measures are scheduled to take effect on December 1. Starting November 8, Beijing will also restrict exports of equipment needed to manufacture batteries for electric cars in a bid to protect the competitiveness of Chinese autos, per The New York Times.

- In the past week, the US and China have also announced tit-for-tat port fees and levies. The Chinese measure, itself a retaliation for a US port fee on Chinese ships, is scheduled to take effect on October 14, per Bloomberg. The rapid escalation of tensions could be interpreted as posturing ahead of the Trump-Xi talks, which were also expected to include a parallel fifth round of talks between Treasury Secretary Scott Bessent and Chinese Vice Premier He Lifeng at the APEC Summit in South Korea, October 31-November 1.

MNI US: OMB Director Vought Suggests That Mass Government Layoffs Have Begun

White House Office of Management and Budget Director Russell Vought writes on X, "The RIFs have begun." The message, which provides no additional details, appears a reference to the 'reduction-in-force' threat Vought issued ahead of the shutdown, promising mass layoffs at federal government agencies. Vought wrote in a memo on September 24, a week before the government shutdown, that federal agencies should prepare reduction-in-force plans for mass firings targeting employees who work for non-legally-mandated programs.

- "In the memo, OMB told agencies to identify programs, projects and activities where discretionary funding will lapse Oct. 1 and no alternative funding source is available. For those areas, OMB directed agencies to begin drafting RIF plans that would go beyond standard furloughs, permanently eliminating jobs in programs not consistent with President Donald Trump’s priorities in the event of a shutdown," per Politico.

US TSYS

MNI US TSYS: Extending Late Session Highs

- Treasury futures continue to extend session highs in late trade - Initially gained this morning on the back of dovish comments from Fed Gov Waller.

- Treasuries gapped higher late morning Friday after Pres Trump threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping. Pres Trump wrote that China is “becoming very hostile” regarding export controls on rare earths and “virtually anything else they can think of, even if it’s not manufactured in China.”

- Currently, Tsy Dec'25 10Y contract trades 113-05.5 (+22), yld 4.0494% -.0889; curves mixed: 2s10s -1.441 at 52.923, 5s30s +1.222 at 99.573. Approaching resistance at 113-12/29 (High Sep 18 / High Sep 11 and the bull trigger).

- Projected rate cut pricing continues to gain vs. late Thursday levels (*): Oct'25 at -24.2bp (-23.7bp), Dec'25 at -47.3bp (-44.8bp), Jan'26 at -59.7bp (-54.7bp), Mar'26 at -71.2bp (-65.2bp).

- Look ahead, cash Tsys closed for Columbus day holiday Monday - futures open along with stocks. Should be a quiet session with NFIB Small Business Optimism data at 0600ET. Philly Fed Paulson economic outlook at 1255ET, (text, Q&A).

OVERNIGHT DATA

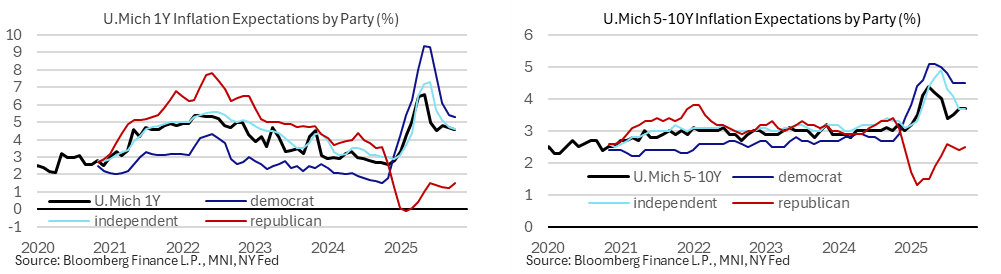

MNI US DATA: No Real Surprises In Preliminary U.Mich Survey For October

The preliminary U.Mich consumer survey for October was broadly as expected, with consumer sentiment holding steady and revealing little impact from the federal government shutdown whilst inflation expectations were also little changed. U.Mich consumer sentiment was mildly stronger than expected as it held “virtually unchanged” at 55.0 (cons 54.0) in the preliminary October release after 55.1 in September.

- “Improvements this month in current personal finances and year-ahead business conditions were offset by declines in expectations for future personal finances as well as current buying conditions for durables.”

- The inflation expectations metrics were close to consensus estimates but are prone to revisions come the final release which appears related to sensitivity to when those of differing political affiliation submit their results.

- 1Y inflation expectations: 4.6% (cons 4.7) after 4.7% in September.

- 5-10Y inflation expectations: 3.7% (cons 3.7) after 3.7% in September.

MNI US DATA: Continuing Claims Look To Have Increased Only Modestly Last Week

- Adding to our earlier comments on initial jobless claims, MNI estimates that continuing claims stood at a seasonally adjusted 1923k in the week to Sep 27. That’s crudely using a four-week moving average for some missing states, whilst GS (1924k) and JPM (1927k) are a little higher.

- We tentatively estimate this to have been a second weekly increase in continuing claims from ~1909k two weeks prior in the week to Sep 13. If accurate, the latter would be its lowest since May (and a downward revision from 1926k in the last official data), holding off recent cycle highs in the 1960k’s.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 671.53 points (-1.45%) at 45692.02

S&P E-Mini Future down 142.5 points (-2.1%) at 6637

Nasdaq down 630.2 points (-2.7%) at 22397.33

US 10-Yr yield is down 8.5 bps at 4.0533%

US Dec 10-Yr futures are up 20.5/32 at 113-4

EURUSD up 0.0044 (0.38%) at 1.1608

USDJPY down 1.33 (-0.87%) at 151.74

WTI Crude Oil (front-month) down $2.71 (-4.41%) at $58.79

Gold is up $21.05 (0.53%) at $3997.48

European bourses closing levels:

EuroStoxx 50 down 94.24 points (-1.68%) at 5531.32

FTSE 100 down 81.93 points (-0.86%) at 9427.47

German DAX down 369.79 points (-1.5%) at 24241.46

French CAC 40 down 123.36 points (-1.53%) at 7918

US TREASURY FUTURES CLOSE

3M10Y -7.305, 10.584 (L: 9.364 / H: 17.954)

2Y10Y -1.472, 52.892 (L: 51.546 / H: 54.585)

2Y30Y -1.584, 111.058 (L: 109.191 / H: 113.65)

5Y30Y +0.066, 98.417 (L: 96.549 / H: 100.264)

Current futures levels:

Dec 2-Yr futures up 4.625/32 at 104-10.625 (L: 104-06.25 / H: 104-11.375)

Dec 5-Yr futures up 12.75/32 at 109-17.25 (L: 109-05.25 / H: 109-19.25)

Dec 10-Yr futures up 20.5/32 at 113-4 (L: 112-16.5 / H: 113-06.5)

Dec 30-Yr futures up 1-13/32 at 118-1 (L: 116-22 / H: 118-06)

Dec Ultra futures up 1-30/32 at 122-1 (L: 120-08 / H: 122-08)

MNI US 10YR FUTURE TECHS: (Z5) Boosted

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 113-04+ High Oct 10

- PRICE: 113-01 @ 17:19 BST Oct 10

- SUP 1: 112-14/01 50-day EMA / 50.0% of Jul 15 - Sep 11 upleg

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Prices rallied sharply just ahead of the London close, putting Treasury futures back above the 113-00 handle for the Friday close. This tops the late September highs, and opens 113-12 as the next notable upside level. Support at the 50-day EMA, currently at 112-14, remains intact. The trend structure is bullish and recent weakness appears to have been a correction. A clear break of the 50-day EMA is required to undermine the trend and this would expose 111-13+, the Aug 18 low and a key support.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.035 at 96.360

Mar 26 +0.070 at 96.580

Jun 26 +0.085 at 96.80

Sep 26 +0.090 at 96.945

Red Pack (Dec 26-Sep 27) +0.085 to +0.090

Green Pack (Dec 27-Sep 28) +0.095 to +0.095

Blue Pack (Dec 28-Sep 29) +0.095 to +0.10

Gold Pack (Dec 29-Sep 30) +0.090 to +0.095

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.13% (+0.01), volume: $2.923T

- Broad General Collateral Rate (BGCR): 4.10% (+0.01), volume: $1.148T

- Tri-Party General Collateral Rate (TCR): 4.10% (+0.01), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.10% (+0.00), volume: $84B

- Daily Overnight Bank Funding Rate: 4.10% (+0.00), volume: $174B

FED Reverse Repo Operation

RRP usage extends to new low of $4.124B (lowest level since early April 2021) with 10 counterparties this afternoon vs. $4.496B low yesterday. Compares to this year's high usage of $460.731B on June 30.

MNI BONDS: EGBs-GILTS CASH CLOSE: Late Risk-Off Rally Seals Gilt, Bund Weekly Gains

European core instruments rallied late Friday to seal a weekly drop in yields.

- Just ahead of the European cash close and the weekend, US President Trump announced on Truth Social that he was considering imposing "massive increase" of tariffs on Chinese goods after China "made a sinister move with rare earth controls".

- That triggered a significant global risk-on move, turning what had been a steadily constructive session into an outright rally for Bunds and Gilts, with bull flattening in both the German and UK curves.

- Conversely, periphery/semi-core spreads which looked to close flat/tighter to Bunds widened, and closed as such.

- OATs underperformed ahead of French President Macron's expected naming of a new Prime Minister late Friday (given the day's developments it appears likely he will opt for a candidate from the centrist/centre-right bloc or a technocrat).

- For the week, the UK curve bull flattened (2Y -0.8bp, 10Y -1.5bp) with Germany's bull steepening (2Y -6.0bp, 10Y --5.4bp).

- After hours we await Macron's announcement as well as ratings reviews of Belgium and Italy. Next week's scheduled highlight is UK August / September Labour Market Data on Tuesday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.8bps at 1.959%, 5-Yr is down 5.9bps at 2.236%, 10-Yr is down 5.9bps at 2.644%, and 30-Yr is down 5.4bps at 3.225%.

- UK: The 2-Yr yield is down 4.6bps at 3.958%, 5-Yr is down 5.8bps at 4.118%, 10-Yr is down 7bps at 4.675%, and 30-Yr is down 7.4bps at 5.472%.

- Italian BTP spread up 1.3bps at 81.8bps / French OAT up 1.3bp at 83.4bps

MNI FOREX: Steady Session Gives Way to Sharp Vol

- A steady Friday session gave way to volatility just ahead of the London close, as President Trump raised a threat of further trade measures and tariffs against China as a result of Beijing's recent actions on rare earths. Risk proxies were sold hard in response, with the same names that were exposed to the tariff disputes earlier this year again being hit the hardest: AUD, NOK, ZAR and NZD are the softest currencies on the day.

- Follow-through USD sales on the Trump post have changed the intraday picture for GBP/USD, which has surged to briefly trade back above 1.3350, and help cool this week's USD rally somewhat. Focus in the coming week shifts to a busy week for the BoE, with several MPC members set to speak, while UK jobs numbers are also due. Commentary across this week flagged the sensitivity of the MPC to inflation expectations, suggesting the bar to another BoE rate cut in 2025 as a result of a weak labour market is rather high.

- With JPY rallying and AUD falling sharply on Trump's renewed tariff threat, AUD/JPY is very close to erasing the Takaichi gap. A further ~90 pip slip puts the price back to 97.35, last week's close, and would help form a long wick candlestick pattern on the weekly chart. Price action in the cross shows the real sensitivity of these two currencies to renewed tension in a trade war scenario.

- Trump's potential withdrawal from a face-to-face meeting with Xi is significant; but with two weeks to go until the APEC conference in South Korea - there still appears to be room for diplomacy - which would work against Friday's price action.

- US earnings season is set to kick off in the coming week, although the data schedule is thinner. September US CPI was originally due for release, however the US government shutdown has delayed this print until October 24th.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 13/10/2025 | 1105/1205 | BOE Greene at Society of Professional Economists Conference | ||

| 13/10/2025 | - | *** | Trade | |

| 13/10/2025 | - | *** | Money Supply | |

| 13/10/2025 | - | *** | New Loans | |

| 13/10/2025 | - | *** | Social Financing | |

| 13/10/2025 | - | ECB Lagarde and Cipollone at IMF/World Bank Meetings | ||

| 13/10/2025 | 1655/1255 | Philly Fed's Anna Paulson | ||

| 13/10/2025 | 1910/2010 | BOE Mann in MonPol Panel, National Association of Business Economists | ||

| 14/10/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor |