US TSYS: Extending Late Session Highs

Oct-10 18:26

- Treasury futures continue to extend session highs in late trade - Initially gained this morning on the back of dovish comments from Fed Gov Waller.

- Treasuries gapped higher late morning Friday after Pres Trump threatened to raise tariffs on China and withdraw from a high-profile upcoming meeting with Chinese President Xi Jinping. Pres Trump wrote that China is “becoming very hostile” regarding export controls on rare earths and “virtually anything else they can think of, even if it’s not manufactured in China.”

- Currently, Tsy Dec'25 10Y contract trades 113-05.5 (+22), yld 4.0494% -.0889; curves mixed: 2s10s -1.441 at 52.923, 5s30s +1.222 at 99.573. Approaching resistance at 113-12/29 (High Sep 18 / High Sep 11 and the bull trigger).

- Projected rate cut pricing continues to gain vs. late Thursday levels (*): Oct'25 at -24.2bp (-23.7bp), Dec'25 at -47.3bp (-44.8bp), Jan'26 at -59.7bp (-54.7bp), Mar'26 at -71.2bp (-65.2bp).

- Look ahead, cash Tsys closed for Columbus day holiday Monday - futures open along with stocks. Should be a quiet session with NFIB Small Business Optimism data at 0600ET. Philly Fed Paulson economic outlook at 1255ET, (text, Q&A).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US PREVIEW: August CPI: Risks Seen Skewed To Core Tickup To 0.4% M/M (1/4)

Sep-10 18:23

Despite coming in softer than expected on the headline reading, the PPI release doesn't appear to have a significant impact on expectations for Thursday's CPI (0830ET) compared with our preview out yesterday - Download PDF Here.

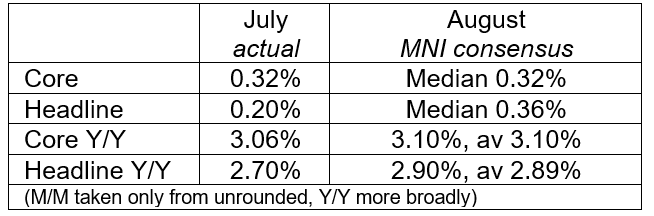

- Consensus (Bloomberg median) is for core CPI to come in at 0.3% M/M rounded in August, same as July (0.32% unrounded).

- Unrounded core CPI expectations suggest a slight skew toward risks of a rounded-up 0.4%, with an unrounded MNI median of 0.32% and range of estimated of 0.29% to 0.36%. That would be steady from 0.32% in July for the joint-highest M/M since January.

- Headline inflation is seen picking up more forcefully, to 0.36% M/M (also would be a post-January high) from 0.20%. The food and energy headline categories are both seen accelerating sharply vs July, resulting in the divergence with the core metric.

- We haven't seen much of a discernable impact on core or headline CPI expectations from the PPI data, whose downside surprise mainly stemmed from weakness in trade services prices (which aren't reflected in CPI).

- Those monthly readings would bring Y/Y core to 3.1% (unch from Jul rounded though a little higher unrounded for a 6-month high), and headline at 2.9% (up from 2.7% prior).

- Recall that the July CPI report saw further acceleration in monthly core inflation but the details defied expectations. The rise was driven by volatile services categories and - in a counter-intuitive finding amid continued tariff concerns - core goods were surprisingly soft (and inflation breadth appeared to moderate). But very strong July PPI data released subsequently, with undertones of businesses passing along higher tariff-related costs to consumers, reversed those dovish cues.

ECB: Macro Since Last ECB: Labour - U/E Rate At Series Lows After More Revisions

Sep-10 18:05

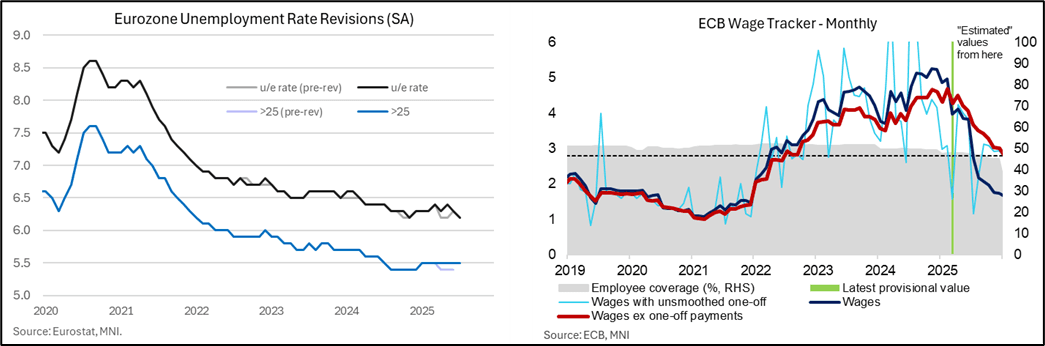

- The Eurozone unemployment rate printed at 6.2% in July as expected, a joint series low, but revisions have again altered recent trends. The data have quite often been revised and June saw a fairly typical 0.1pp upward revision to 6.3%, although the +0.2pp to 6.4% in May was more surprising.

- It leaves a trend of recent improvement but with question marks over the data. What had been seen as three months at joint cycle lows of 6.2% through Apr-Jun, tying with 6.2% in Oct-Nov 2024, Eurostat now estimate a latest pattern of 6.3% in Apr, 6.4% in May, 6.3% in Jun and 6.2% in July, tying with 6.2% only in Nov 2024.

- ECB’s Lagarde has pointed to these at-the-time historically low unemployment rates when citing the health of the labour market in recent meetings. Outright employment growth remains subdued however, with just 0.1% Q/Q and 0.6% Y/Y in Q2.

- As for inflationary pressures stemming from the labour market, Eurozone unit labour costs grew 3.1% Y/Y in Q2, down from 3.3% in Q1 for the seventh consecutive annual deceleration. This was above the ECB's 2.9% projection made in June, seemingly driven by the smaller-than-expected deceleration in total compensation per employee growth (3.9% Y/Y vs 4.0% prior, 3.4% ECB).

- While a declaration in ULC growth has allowed the ECB to deliver 200bps of easing this cycle, the data is too lagged to help determine whether further fine-tuning of the policy stance is necessary. Given the modest upward surprise to compensation per employee growth, it argues in favour of steady rates at 2.00% for now.

- ULC growth may have moderated at a steadier pace than the ECB forecast but its forward looking wage tracker released earlier in the inter-meeting process points to a continued decline in negotiated wage growth. Now with estimates out to 1Q26, it eyes wage growth excluding one-off payments at 2.6% Y/Y in 1Q26 after 3.1% in 4Q25. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling.

EURGBP TECHS: Corrective Pullback

Sep-10 18:00

- RES 4: 0.8769 High Jul 28 and the bull trigger

- RES 3: 0.8744 High Aug 7

- RES 2: 0.8728 76.4% retracement of the Jul 28 - Aug 14 bear leg

- RES 1: 0.8713 High Sep 2

- PRICE: 0.8653 @ 16:30 BST Sep 10

- SUP 1: 0.8636/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8514 61.8% retracement May 29 - Jul 28 upleg

EURGBP traded lower Tuesday and has breached the 20-day EMA. Short-term weakness is considered corrective - for now - and support to watch lies at 0.8597, the Aug 14 low. Clearance of this level would reinstate a recent bearish threat. A resumption of gains would open 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high. Note that MA studies are in a bull-mode position highlighting a dominant uptrend.

Trending Top

Jun-25 06:23