FED: Musalem Open-Minded To Further Easing But Limited Room To Do So

Oct-10 17:28

St Louis Fed's Musalem ('25 voter), one of the more hawkish FOMC members, broadly keeps to his position in the committee - we had seen him as likely one of the six dots looking for no further cuts this year after the 25bp last month. He is open-minded to further easing but there is limited room to do so.

- Paraphrasing: "I supported a 25bp cut in September as a way to provide insurance against labor market weakening, while continuing to lean against inflation. I now perceive monetary policy as somewhere between modestly restrictive and neutral. Looking ahead, I am open-minded about a potential further reduction in interest rates to provide further insurance against labor market weakening. I believe we have to tread with caution because there is limited room for further easing before mon pol could become overly accomodative. I believe mon pol should continue to lean against persistence in inflation, whether that comes from tariffs, a lower growth in labor supply or for any other reason."

Other Bloomberg headlines:

- "FED'S MUSALEM: RIGHT NOW, MANDATES SEEM LIKE THEY'RE IN TENSION

- MUSALEM: INFLATION IS MATERIALLY ABOVE OUR TARGET

- MUSALEM: ONLY 10% OF INFLATION WE'RE SEEING IS TARIFFS

- MUSALEM: EXPECT TARIFF INFLATION IMPACT TO FADE IN 2-3 QUARTERS

- MUSALEM: I EXPECT LABOR MARKET TO SOFTEN SOME, IN ORDERLY WAY" - bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

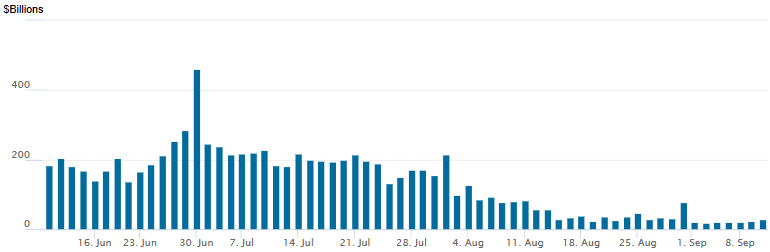

US: FED Reverse Repo Operation

Sep-10 17:18

RRP usage climbs to $29.400B with 18 counterparties this afternoon from $22.915B Tuesday. Compares to $17.923B on Wednesday, Sep 3 - the lowest levels since early April 2021. This year's high usage of $460.731B occurred on June 30.

PIPELINE: Corporate Bond Update: $3B Saudi Aramco 2Pt Launched

Sep-10 17:07

- Date $MM Issuer (Priced *, Launch #)

- 09/09 $3B #Saudi Aramco $1.5B each: 5Y Sukuk +70, 10Y +80 (books were over $16.5B)

- 09/09 $3B *IDA (International Development Assn) 7Y SOFR+55

- 09/10 $3B *KFW 3Y SOFR+30

- 09/10 $1B *Federal Home Loan 2Y +3.5

- 09/10 $1B Light and Wonder 8NC3 6.5%a

- 09/10 $900M K Hovnian Ent $450M each: 5.5NC2.5, 8NC3

- 09/09 $500M *Korea Housing Finance Corp (KHFC) 5Y +40

- 09/10 $500M #Bidvest WNG 7NC3 6.2%

- 09/09 $500M #Komatsu Finance AM 5Y +62

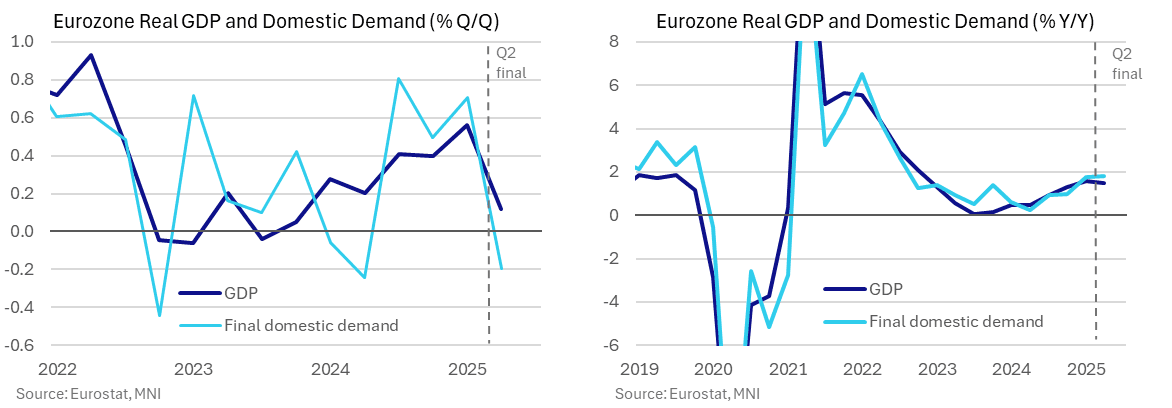

ECB: Macro Since Last ECB: Growth - Domestic Demand Falls After Solid Run [1/2]

Sep-10 17:05

- Released shortly after the July ECB meeting, real GDP growth was a little better than analysts expected in the Q2 advance release at 0.1% Q/Q (cons 0.0) after a strong 0.6% Q/Q in Q1. Subsequent revisions haven’t materially altered this trend, if anything marginally on the stronger side with the Y/Y rounding up to 1.5% Y/Y.

- The recent final release put real GDP growth at 0.12% Q/Q in Q2, helped by a large +0.5pp coming from change in inventories whilst final domestic demand dragged -0.2pps for its joint largest decline since late 2022.

- The latter points to a marked cooling in underlying demand although it does follow a strong 0.7pp in Q1 and 0.6pp averaged in 2H24. As such, final domestic demand growth at 1.8% Y/Y remained a little above that of real GDP growth.

- The final report also showed that nominal GDP grew 0.8% Q/Q (vs 0.7% prior) and 4.0% Y/Y (vs 3.9% prior) in Q2. On a sequential basis, Q2 nominal growth was mostly inflationary – real growth was 0.1% Q/Q while GDP deflator growth was 0.7% Q/Q. However, on an annual comparison there is a growing contribution from real growth to nominal GDP, reflecting a gradual recovery in activity as ECB past rate cuts feed through the system (real growth was 1.5% Y/Y in Q2, versus deflator growth of 2.5% Y/Y).

- We calculate that profits contributed 0.6pp to annual nominal GDP growth after just 0.1pp in Q1 and negative contributions in the three quarters prior, with the impact of US tariffs on Eurozone exporters' profits key to watch in the quarters ahead.