MNI US OPEN - Watching for Weakness in April Payrolls

EXECUTIVE SUMMARY

- MNI US PAYROLLS PREVIEW - TAILWINDS EBB AS STORM GATHERS

- CHINA SAYS IT’S ASSESSING US TALKS, HINTING AT POSSIBLE THAW

- TRUMP TO PROPOSE SLASHING $163BN IN GOVERNMENT PROGRAMS IN BUDGET BLUEPRINT

- SPAIN MANUFACTURING PMI SURPRISINGLY WEAK; US TARIFF POLICY CITED

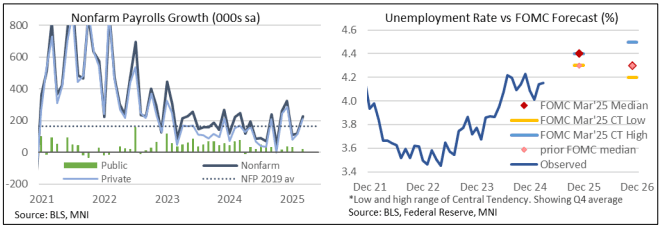

Figure 1: Recent US labour market developments

NEWS

MNI US PAYROLLS PREVIEW: Tailwinds Ebb as Storm Gathers

Nonfarm payrolls are seen increasing a seasonally adjusted 135k in April in the Bloomberg survey after a stronger than expected 228k in March. Primary dealer analysts also see 135k whilst the Bloomberg whisper is weaker again, currently at 120k. April won’t benefit from the favorable weather and returning strikers that helped March employment growth. Immigration restrictions are likely to increasingly drag on employment growth ahead although this month’s report could be a little early.

MNI POLITICAL RISK ANALYSIS: Australia Election Preview

The incumbent centre-left Australian Labor Party (ALP) is on course win a second term in office in the 3 May federal election. Just months ago, it appeared likely that the conservative Liberal/National coalition were set to return to power after just one term on the opposition benches. However, public sentiment appears to have shifted notably over the course of the campaign. In this election preview we will provide a short briefing on how the election works and who the main parties are, a chartpack of opinion polling and betting market data ahead of the vote, a scenario analysis examining the probabilities and implications of various outcomes, and some sell-side views on the contest.

US/CHINA (BBG): China Says It’s Assessing US Talks, Hinting at Possible Thaw

China said it is assessing the possibility of trade talks with the US, the first sign since Donald Trump hiked tariffs last month that negotiations could begin between the two sides. China’s Commerce Ministry said in a Friday statement that it had noted senior US officials repeatedly expressing their willingness to talk to Beijing about tariffs, and urged officials in Washington to show “sincerity” toward China.

US/JAPAN (WSJ): Japan Wary of China Import Surge, Finance Minister Says

Japan will act in response to any surge in Chinese imports if U.S. tariffs push unsold Chinese goods onto global markets, the country's finance minister said, a sign of concern about the knock-on effects of President Trump's trade war. In an interview at his office in Tokyo on Friday, Katsunobu Kato also said currency management hasn't been part of U.S.-Japan trade talks and exchange rates should be determined by market forces. Trump has repeatedly criticized Japan for pursuing policies that weaken the yen and boost exports.

US/JAPAN (BBG): Japan Sees Trade Talks Speeding Up, Hopes for June Agreement

Japan aims to achieve a trade agreement with the US in June, with the high-stakes bilateral discussions expected to gain momentum in mid-May, Tokyo’s chief negotiator said after concluding the latest round of talks in Washington. The second meeting between US officials, including Treasury Secretary Scott Bessent, Trade Representative Jamieson Greer, Commerce Secretary Howard Lutnick and Japan’s top trade representative Ryosei Akazawa was a frank and open one, although many areas of the discussions still need to be made concrete, Akazawa said.

UK (MNI): ReformUK By-Election Win Will Concern Gov't, But Major Policy Shift Unlikely

The narrow win for the right-wing populist Reform UK in the Runcorn and Helsby by-election will garner significant headlines, but at least in the short-to-medium term is unlikely to notably alter gov't policy or stability. Nigel Farage's party won the seat by just six votes, overturning a 14k majority for the incumbent centre-left Labour party of PM Sir Keir Starmer. To date, right wing and eurosceptic parties have struggled to win elections outright with the UK's first-past-the-post electoral system allowing centrist and left-wing voters to vote tactically to shut them out. The exception being the European Parliament elections in 2019 in which Reform UK's predecessor, the Brexit Party, won a plurality of the vote. The Reform UK breakthrough, likely to continue through the day as results come in from local elections across England, will be as much, if not greater, concern for the main opposition centre-right Conservatives, which are poised for significant losses, as they are for Labour.

US/EU (FT): Europe Ready to Make Trump a €50bn Trade Offer, Says EU Negotiator

Brussels wants to increase purchases of US goods by €50bn to address the “problem” in the trade relationship, the EU’s top negotiator has said, adding that the bloc is making “certain progress” towards striking a deal. But Maroš Šefčovič, the EU’s trade commissioner, suggested in an interview with the Financial Times that the bloc would not accept Washington keeping in place 10 per cent tariffs on its goods as a fair resolution to trade talks.

US (WSJ): Trump to Propose Slashing $163 Billion in Government Programs in Budget Blueprint

President Trump is expected to propose far-reaching cuts to federal environmental, renewable energy, education and foreign-aid programs in a budget blueprint that slashes nondefense discretionary spending by more than $160 billion, according to administration officials. The fiscal 2026 budget proposal, which the White House is planning to release on Friday, is a largely symbolic wish list that lays out the president’s spending and political priorities. Congress, which Republicans control by narrow majorities in both chambers, will spend months debating which elements of the proposed plan should be turned into law.

US/INDIA/PAKISTAN (BBG): US Seeks to Stop India-Pakistan Tensions Sparking Wider Conflict

Vice President JD Vance said the US was working to ensure tensions between India and Pakistan don’t escalate into a broader regional conflict in the wake of an attack last week that killed dozens of people in Indian-controlled Kashmir. “I’m worried about any time you see a hot spot breaking out, especially between two nuclear powers,” Vance said in a podcast interview with Bret Baeir of Fox News.

US/IRAN (BBG): Trump Moves to Cut Iran’s Oil Sales as Nuclear Talks Stall

President Donald Trump said he would impose secondary sanctions on nations or companies buying Iranian oil, ratcheting up pressure on Tehran as nuclear talks with the US hit a snag. “Any Country or person who buys ANY AMOUNT of OIL or PETROCHEMICALS from Iran will be subject to, immediately, Secondary Sanctions,” Trump said in a Thursday post on social media, without providing further details on the measures. “They will not be allowed to do business with the United States of America in any way, shape, or form.”

US/NATO (BBG): Trump May Skip NATO Summit If No Spending Progress Made: Spiegel

US Ambassador to NATO Matthew Whitaker has been pressing allies to make a formal commitment to a defense spending target of 5% of GDP, Spiegel reports, citing European NATO officials. Whitaker wants allies to make the commitment at the NATO summit in late June. Whitaker told allies that Trump may not attend the summit if they don’t make progress on US spending demands.

EUROPE (MNI): China Diverted Trade to EZ in Trump First Term - ECB Bulletin

The euro area saw imports from China rise around 2-3% of as a direct result of trade tensions between the U.S. and China during president Donald Trump's first term, according to the ECB's latest economic bulletin, which notes "the effective tariff rate" between the two nations increased by almost 18 percentage points. The paper shows a significant decline in China exports to the U.S. that led China to seek other markets, in which the Eurozone played an important role, although the impact was bigger in other East and South Asian countries. The increase of flows to Canada and Mexico was slightly less than to Europe.

BOJ (MNI): BOJ Warns of Forex Impact on Inflation; Cites Four Risks

The Bank of Japan warned of the inflationary risks posed by sharp fluctuations in foreign exchange markets and emphasised the complex channels through which global trade policy changes could affect the Japanese economy, according to the full text of its April Outlook Report released Friday. The BOJ stated it will continue to monitor closely the economic and price impacts using its nationwide network of head office, branches, and overseas offices. It highlighted that significant shifts in trade policies in other countries could influence Japan’s economy through several key channels, listing four specific risks.

CORPORATE (WSJ): Apple Says Most of Its Devices Shipped Into U.S. Will Be From India, Vietnam

Apple said a majority of its devices shipped into the U.S. in the June quarter will originate in India and Vietnam, a move to allay investor concerns about the impact of tariffs on its operations. The company was among the hardest-hit of the tech giants last month because of its exposure to China, a primary target of the Trump administration’s global tariff pressure. Most of Apple’s devices are assembled in the country, and investors are closely watching its efforts to shift final assembly of devices bound for the U.S. to India and other countries.

DATA

EUROZONE DATA (MNI): EZ Services HICP 3.93%, Firmer Than Highest Analyst Estimate

- EUROZONE APR FLASH CORE HICP +2.7% Y/Y

- EUROZONE APR FLASH CORE HICP +2.7% Y/Y

Eurozone April flash HICP Y/Y inflation came in at 2.16%, 6 hundredths above the rounded consensus of 2.1% (vs 2.18% March). On a monthly basis, Eurozone inflation came in at 0.56% (0.5% cons, 0.61% prior). The data in the release points towards a firm services rebound. Core HICP also printed above consensus, at 2.72% Y/Y and 0.99% M/M (2.5% cons; Mar 2.43% Y/Y, 0.97% M/M). Looking at the individual categories: Services inflation notably accelerated to 3.93% (3.45% Mar) - this means the category is back up to levels seen last in January, and the print was above the highest estimate we've seen ahead of the national level data (there has been a 3.4% - 3.8% range).

EUROZONE DATA (MNI): Unemployment Rate at 6.2%, But Weakening Employment Prospects

- EUROZONE MAR UNEMPLOYMENT RATE 6.2%

The Eurozone unemployment rate was 6.2% in March, a tenth higher than consensus. The unemployment rate has been at this level for six consecutive months now, after February's reading was revised up a tenth. The unemployment rate remains at historic lows. However, the EC's expected employment indicator was steady at 96.5, the joint

weakest since February 2021. Momentum in services, retail and construction expected employment has weakened in recent months, potentially adding upside risks to future unemployment readings. However, these risks are somewhat offset by a coincident drift higher in the labour hoarding indicator.

EUROZONE DATA (MNI): April Final Manuf PMI Sees Small Upward Revision; Spain Drags

- EUROZONE APRIL FINAL MANUF PMI 49.0 (48.7 FLASH, 48.6 MARCH)

- GERMANY APRIL FINAL MANUF PMI 48.4 (48.0 FLASH, 48.3 MARCH)

- FRANCE APRIL FINAL MANUF PMI 48.7 (48.2 FLASH, 48.5 MARCH)

There was a small upward revision to the Eurozone-wide manufacturing PMI to 49.0 (vs 48.7 flash, 48.6 prior). Upward revisions in France (48.7 vs 48.2 flash) and Germany (48.4 vs 48.0 flash) and a stronger-than-expected Italian print were offset by a notable miss in Spain. Meanwhile, the Irish PMI reached a 34-month high of 53.0 - no doubt distorted by tariff front-running as has been seen in goods trade and national account data. We estimate the Germany and France aggregate manufacturing PMI at 48.5 (vs

48.1 flash, 48.4 prior) and the ex-Germany/France aggregate at 49.6 (vs 49.5 flash, 48.9 prior).

SPAIN DATA (MNI): Manufacturing PMI Surprisingly Weak; US Tariff Policy Cited

- SPAIN APRIL MANUF PMI 48.1 (50.1 FCAST, 49.5 MARCH)

The Spanish April manufacturing PMI surprisingly fell to 48.1 (vs 50.1 cons, 49.5 prior). Following the flash Eurozone-wide release last week, we had estimated the ex-France and Germany average manufacturing PMI at 49.5, and the "rest of Eurozone" commentary had indicated a "solid growth of output, albeit with the pace of expansion easing slightly from that seen in March". This marks the fourth consecutive fall in the Spanish manufacturing PMI (from 53.3 in December), which has been followed by a deterioration of industrial production momentum. The recent national electricity outage will further drag on Q2 growth prospects.

ITALY DATA (MNI): Manufacturing PMI Better Than Feared, But Still Contraction

- ITALY APRIL MANUF PMI 49.3 (47.0 FCAST, 46.6 MARCH)

In contrast to Spain, the Italian manufacturing PMI was stronger-than-expected at 49.3 (vs 47.0 cons, 46.6 prior), the highest since August 2024. However, it's worth remembering that the PMI has now been in contractionary territory for 24 of the last 25 months. There was early evidence of tariff uncertainty weighing on demand, but more

data will be needed to confirm this trend. As in Spain, output charges rose in April.

SWEDEN DATA (MNI): Solid April Manufacturing PMI, But Still Scope for Dovish RB Next Week

The Swedish April manufacturing PMI climbed to its highest since May 2022 at 54.2 (vs a two tenth upwardly revised 53.8 prior). The five-analyst strong consensus looked for 53.5 (range 52.5-54.0). With the exception of a rise in supplier deliveries to 50.4 (vs 49.2 prior), there aren't too many clear tariff/trade uncertainty-related impacts to note. Although the report suggests past Riksbank rate cuts are supporting the manufacturing sector, we still think there is scope for a dovish tilt at next week's decision owing to tariff-related downside growth risks.

NORWAY DATA (MNI): Solid Labour Market Conditions Should Keep Norges Bank Cautious

With labour market data showing no signs of deterioration and CPI-ATE inflation still above target, this may keep Norges Bank cautious with respect to future cut guidance at next week's May 8 decision (rates will almost certainly be held at 4.50%). On April 8, Norges Bank Governor Wolden Bache said that "our interpretation of Norges Bank's mandate is that considerable weight shall be given to employment - also at times when inflation deviates significantly from the target".

JAPAN DATA (MNI): Jobless Rate Edges Higher, But Still Close to Cycle Lows

- JAPAN MARCH JOBLESS RATE RISES TO 2.5% FROM FEB 2.4%

Japan's jobless rate for March edged up to 2.5%, against a 2.4% forecast, which was also the prior outcome. The job-to-applicant ratio firmed to 1.26, versus a 1.25 forecast and 1.24 recorded in Feb. The unemployment rate has risen but only from recent cycle lows, while the slight uptick in the job-to-applicant ratio modestly closes some of the wedge between the two series. In terms of the detail, the number of employed people fell by 80k m/m following the -110k drop in Feb. The participation rate edged up to 63.3%, but is sub late 2024 highs. A still tight labor market should supporting underlying wage momentum, but some slowing in total people employed will be a watch point.

AUSTRALIA DATA (MNI): March Retail Spend Near Estimates, But Q1 Volume Spend Flat

- AUSTRALIA MAR RETAIL SALES +0.3% M/M

The headline retail sales print for March was close to expectations, rising 0.3%m/m (+0.4% was forecast, while the Feb rise was 0.2%). The strongest segments were food up 0.7%m/m, while other retailing rose 0.7%. Drags came from department stores, off 0.5%, which was its first decline since Sep last year. Cafes, restaurants were down 0.5%m/m as well. The ABS noted: Retail turnover rose in all states and territories, except for Queensland (-0.4 per cent) as Ex-Tropical Cyclone Alfred negatively impacted

spending. 'The extreme weather early in the month led to significant disruptions for businesses and households throughout Queensland."

FOREX: Greenback Fades with Yields Headed into April Payrolls

- The greenback is weaker against all others early Friday, with the USD Index reversing off yesterday's recovery high at 100.375. GBP is similarly weak, helping EUR/GBP snap the weakness posted through support earlier this week.

- Potential trade talks remain a focus for markets - with deals made between the US and Japan, US and India seen as particularly advanced. The Japanese finance minister Kato noted that currency management has not been a feature of talks so far, nor has any Plaza Accord 2.0 concept come up - meaning any potential agreements are likely to be highly trade oriented - conversations which have helped allow USD/JPY to hold the majority of the rally posted on yesterday's dovish turn from the BoJ on Thursday.

- We noted yesterday the extended consolidation phase for AUD/USD, which has now stretched to 10 consecutive sessions of the price trading either side of $0.64. This is a relatively uncommon pattern that rarely extends beyond this streak, and historically resolves with a weaker AUD/USD and a break lower. Weakness from here would heighten focus on the 50-day EMA support at 0.6316.

- Focus shifts to the upcoming US jobs report. Nonfarm payrolls growth is expected at 135k, although potential weather distortions have made it harder to get a sense of underlying trends in recent months. Central bank speak is quiet - with no notable appearances due. The Fed remain inside their pre-decision media blackout period.

EGBS: Bunds Look Through Firm EZ Data; Focus Shifts to US NFP

Bund futures have been largely undeterred by the stronger-than-expected Eurozone flash April core HICP print and upward revisions to the April manufacturing PMIs. After gapping lower at the open in response to a more optimistic US trade deal backdrop, RXM5 has recovered well from session lows of 131.34, with yesterday’s low of 131.33 containing downside. The contract is -14 ticks versus Wednesday’s settlement at 131.64.

- Initial resistance in Bund is still at the opening gap, situated at 131.93, but most are still eyeing the April 7 high and bull trigger at 132.03.

- The firmer-than-expected Eurozone data has somewhat limited the recovery at the short-end though, with Schatz yields up 3.5bps and the curve bear flattening.

- Eurozone flash April core HICP was 2.72% Y/Y (vs 2.43% prior), above the highest analyst estimate we had seen ahead of the release. Services inflation was biased higher by Easter-timing related effects.

- Meanwhile, the April EZ manufacturing was 49.0 (vs 48.7 flash, 48.6 prior) and March unemployment was 6.2% (vs 6.1% cons, 6.2% prior).

- 10-year EGB spreads to Bunds are mixed. The BTP/Bund spread is little changed on the week at 111.5bps.

- Focus turns to the US labour market report at 1330BST/1430CET.

GILTS: Early Outperformance vs. Bunds Extends

Gilts have extended on the rally that we flagged at the open.

- While a bid in wider core global FI has developed in the time since, with e-minis and oil ticking away from Asia-Pac highs, the earlier bid in gilts bucked the broader trend and UK paper continues to outperform.

- There hasn’t been an overt driver for the move. ReformUK’s local and byelection results shouldn’t be much of a needle mover at this stage.

- Futures as high as 93.93 as the recent bullish move extends. Yesterday’s high (93.86). Bulls now eye 94.00, followed by the April 7 high and key resistance level (94.50).

- Yields 4-6bp lower, 10s outperform.

- Uptrend support in 10s, drawn off the Dec ‘21 lows (4.420%), has been pierced, exposing the year-to-date low

- Spread vs. Bunds in to ~195bp, set for the lowest close since April 4.

- GBP STIRs adjust to the rally in gilts after a modestly hawkish start on increased optimism surrounding a Sino-U.S. trade discussion was reversed.

- BoE-dated OIS shows 98bp of cuts through December vs. ~95bp at the open, a reminder that over 100bp of cuts were priced in over that horizon yesterday. ’25 meeting contracts are 0.5-2.0bp more dovish on the day.

- SONIA futures flat to +3.5.

- Little of note on the UK calendar today, which will leave focus on tariff headlines and macro data (U.S. NFP & Eurozone CPI provide the focal points).

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

May-25 | 4.196 | -26.3 |

Jun-25 | 4.057 | -40.2 |

Aug-25 | 3.842 | -61.7 |

Sep-25 | 3.695 | -76.4 |

Nov-25 | 3.536 | -92.3 |

Dec-25 | 3.484 | -97.5 |

EQUITIES: Eurostoxx 50 Futures Build on Recent Gains, Above 20-, 50-Day EMAs

Eurostoxx 50 futures maintain a positive tone and are building on recent gains. The contract has cleared the 20-day EMA and the 50-day EMA, at 5102.56. A clear break of this average would strengthen the current bull cycle and signal scope for a continuation of the corrective uptrend. This would open 5165.00 next, the Apr 3 high. Support to watch lies at 4812.00, the Apr 16 low. Clearance of this level would highlight a reversal. The recovery in the e-mini S&P continues, with a tenth consecutive session of higher highs - the longest winning streak of the year so far, underpinning the short-term positive momentum for stocks. The bull cycle that started on Apr 7, remains in play and has breached a number of important short-term resistances. The index has topped 5618.25, the 50-day EMA, opening layered resistance at 5773.25-5774.43.

- Japan's NIKKEI closed higher by 378.39 pts or +1.04% at 36830.69 and the TOPIX ended 8.34 pts higher or +0.31% at 2687.78.

- Across Europe, Germany's DAX trades higher by 358.91 pts or +1.6% at 22852.32, FTSE 100 higher by 71.45 pts or +0.84% at 8568.15, CAC 40 up 112.26 pts or +1.48% at 7705.21 and Euro Stoxx 50 up 68.18 pts or +1.32% at 5227.76.

- Dow Jones mini up 236 pts or +0.58% at 41081, S&P 500 mini up 27.75 pts or +0.49% at 5649.5, NASDAQ mini up 54.75 pts or +0.28% at 19918.75.

Time: 09:55 BST

COMMODITIES: Gold Remains Within Range of Recent Lows

A medium-term bearish trend in WTI futures strengthened this week and the latest move down reinforces this theme, signalling the end of the correction between Apr 9 - 23. The correction allowed an oversold trend condition to unwind. A clear resumption of the bear cycle would open $53.72, a Fibonacci projection. Initial support has broken at $58.29, the Apr 29 low. Resistance to watch is $64.87, the 50-day EMA. Gold is off lows early Friday, but remains within range of recent lows after markets pressuring prices toward multi-week lows and opening a sizeable gap with the recent high. The S/T weakness has pressured support at the 20-day EMA at $3243.7, which could begin to signal a short-term top should the price stay fragile. $3167.8 marks the next key downside level, the April 3 high and recent breakout. For now, moving average studies are in a bull-mode position highlighting a dominant uptrend. The next objective is $3547.9, a Fibonacci projection.

- WTI Crude down $0.18 or -0.3% at $59.03

- Natural Gas down $0.05 or -1.41% at $3.429

- Gold spot up $20.75 or +0.64% at $3258.9

- Copper up $5.1 or +1.1% at $467.65

- Silver up $0.08 or +0.25% at $32.4932

- Platinum up $2.11 or +0.22% at $970.68

Time: 09:55 BST

| Date | GMT/Local | Impact | Country | Event |

| 02/05/2025 | 1230/0830 | *** | Employment Report | |

| 02/05/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |