EUROZONE DATA: April Final Manuf PMI Sees Small Upward Revision; Spain Drags

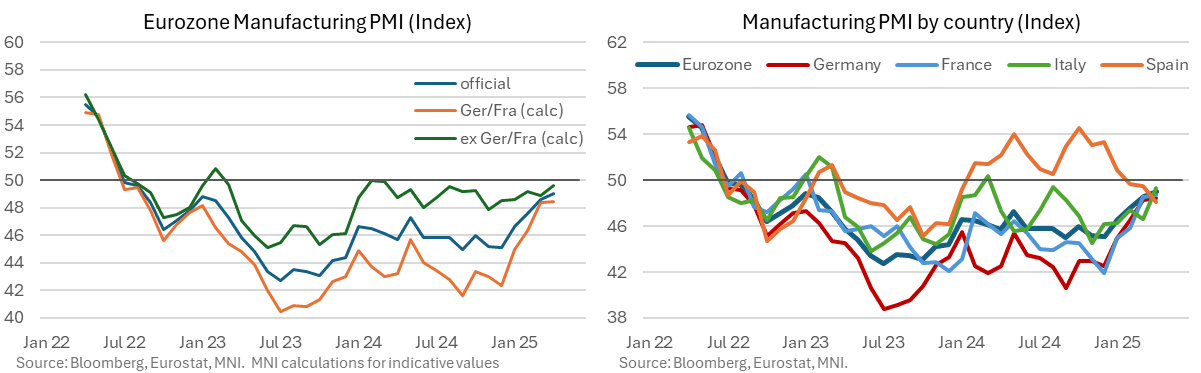

There was a small upward revision to the Eurozone-wide manufacturing PMI to 49.0 (vs 48.7 flash, 48.6 prior). Upward revisions in France (48.7 vs 48.2 flash) and Germany (48.4 vs 48.0 flash) and a stronger-than-expected Italian print were offset by a notable miss in Spain.

- Meanwhile, the Irish PMI reached a 34-month high of 53.0 – no doubt distorted by tariff front-running as has been seen in goods trade and national account data.

- We estimate the Germany and France aggregate manufacturing PMI at 48.5 (vs 48.1 flash, 48.4 prior) and the ex-Germany/France aggregate at 49.6 (vs 49.5 flash, 48.9 prior). Waning momentum is clearly most notable in Spain – see charts.

Two highlights from the aggregate survey were a drag on export sales and increased output charge inflation – the latter presents an upside risk to non-energy industrial goods HICP readings, with flash Eurozone-wide April HICP due at 1000BST. Key notes from the PMI release:

- “Export markets were the main drag on sales, as new business from overseas shrank at a faster pace than that seen for total new work. Still, the drop in new orders from non-domestic customers was its shallowest since April 2022”.

- “Eurozone factories still demonstrated some reservation with regards to the outlook. For instance, purchasing activity fell further in April, as did both stocks of pre- and post-production items”.

- “Quicker lead times coincided with the first reduction in input costs for eurozone factories since last November. However, prices charged for goods were raised more aggressively. In fact, the rate of output charge inflation accelerated to a two-year high”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Citi Retain Long Duration Bias Into Tariff Announcement, Eye IRISH In MT

Citi note that “even after adjusting for fiscal spending, Bunds lag by around 15bp on a regression with a basket of tariff-sensitive EUR equities”.

- They go on to write “into today’s tariff announcement, we prefer bullish/dovish exposure to EUR duration. For EGB spreads, the indifference towards richening Bund swap spreads has tended to be short-lived in the past”.

- “The recent EGB resilience might have been driven by relatively clean positioning, investors waiting for more clarity and prospects of more ECB rate cuts in case of punitive tariffs but ignores their growth implications.”

- As a result, they “retain bearish exposure to periphery spreads into the announcement, with the 10-Year BTP/Bund spread now close to the tight end of its range”.

- At a more granular level, they note that “tariff risks within EMU-11 seem most acute for Germany, Italy, and Ireland while Spain and France seem relatively shielded. This was likely behind the YtD underperformance of IRISH credit, which continued yesterday, despite still-strong fundamentals otherwise. These headwinds are likely to persist for now, although we believe value in the Irish credit is being built for the medium-term”.

FOREX: FX OPTION EXPIRY

Of note:

EURUSD ~1bn at 1.0800.

EURUSD 2.3bn at 1.0800 (thu).

USDJPY 1.19bn at 150.00 (thu).

EURUSD 1.53bn at 1.0800 (fri).

USDCAD 1.19bn at 1.4350 (fri).

AUDUSD ~1bn at 0.6300 (fri).

AUDUSD 1.43bn at 0.6350 (tue).

- EURUSD: 1.0700 (1.11bn), 1.0750 (525mln), 1.0790 (362mln), 1.0800 (972mln).

- USDJPY: 149.80 (278mln), 149.95 (299mln).

- USDCAD: 1.4300 (307mln), 1.4350 (425mln).

- NZDUSD: 0.5775 (427mln).

OPTIONS: Expiries for Apr02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0790-00(E1.9bln)

- USD/JPY: Y149.80-95($577mln)

- USD/CAD: C$1.3780($1.1bln), C$1.4400-15($924mln)

- USD/CNY: Cny7.3500($1.3bln)