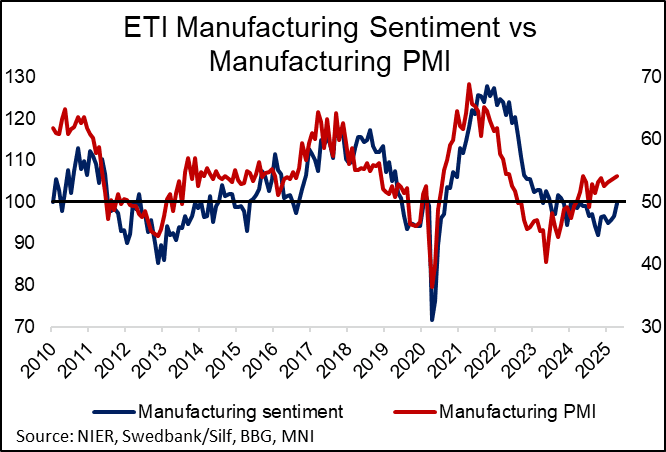

SWEDEN: Solid April Manufacturing PMI, But Still Scope For Dovish RB Next Week

The Swedish April manufacturing PMI climbed to its highest since May 2022 at 54.2 (vs a two tenth upwardly revised 53.8 prior). The five-analyst strong consensus looked for 53.5 (range 52.5-54.0). With the exception of a rise in supplier deliveries to 50.4 (vs 49.2 prior), there aren’t too many clear tariff/trade uncertainty-related impacts to note. Although the report suggests past Riksbank rate cuts are supporting the manufacturing sector, we still think there is scope for a dovish tilt at next week’s decision owing to tariff-related downside growth risks.

- Inventories eased a touch to 51.6 (vs 51.8 prior), and while export orders fell to 49.9 (vs 50.5 prior), it’s still above January’s 49.4 reading.

- Total new orders rose to 55.8 (vs 53.9 prior), the highest since May 2024. Meanwhile, production (58.0 vs 59.2 prior) and employment (52.9 vs 53.0 prior) also remained in expansionary territory.

- Raw material prices fell to 50.9 (vs 55.6 prior), the lowest since October 2024.

- Planned production remained above 60 at 65.1 (vs 63.0 prior) – the highest since May 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: The Kiwi extends gains into the European session

- The Kiwi was the best early performer against the Dollar in G10s Overnight, and the Kiwi is extending higher into the European session, NZDUSD has now gained just over 80 pips from Monday's low, and next upside of interest comes at 0.5773.

- AUDUSD sees a similar chart to the NZDUSD, and the next immediate resistance for the Aussie comes at 0.6331.

- At the other side of G10 Currencies, the Yen is down 0.23% versus the Greenback, with the USDJPY looking to break back above the 150.00, but still short of Monday's high at 150.27, so far the cross printed a 150.00 high.

(Chart source: MNI/Bloomberg).

STIR: Just Over 50bp Of Cuts Priced Through Dec, Liberation Day Eyed

GBP STIRs little changed to incrementally more hawkish vs. settlement.

- “Liberation Day” is upon us and the latest round of source reports have pointed to a slightly more lenient U.S. tariff plan being amongst the options considered by Trump.

- There has been suggestions that the tariffs announced later today will present the worst-case scenario, with countries’ future actions having the potential to reduce the levies going forwards.

- Overnight local news flow was limited.

- SONIA futures flat to -1.5.

- BoE-dated OIS essentially unchanged, showing 18.5bp of cuts for May, 22bp through June, 34bp through August and 51.5bp through year-end.

- Nothing of note on the UK data/speaker calendar today, leaving focus on U.S. trade tariff decisions and data.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

May-25 | 4.271 | -18.4 |

Jun-25 | 4.237 | -21.8 |

Aug-25 | 4.114 | -34.2 |

Sep-25 | 4.063 | -39.3 |

Nov-25 | 3.977 | -47.8 |

Dec-25 | 3.936 | -51.9 |

EQUITY TECHS: E-MINI S&P: (M5) MA Studies Highlight A Dominant Downtrend

- RES 4: 5878.53 50-day EMA

- RES 3: 5837.25 High Mar 25 and a key resistance

- RES 2: 5757.95 20-day EMA

- RES 1: 5694.75 High Apr 1

- PRICE: 5670.25 @ 07:21 BST Apr 2

- SUP 1: 5559.75/33.75 Low Mar 13 and the bear trigger / Low Mar 31

- SUP 2: 5500.00 Round number support

- SUP 3: 5483.50 2.00 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

- SUP 4: 5396.00 2.236 proj of the Dec 6 ‘24 - Jan 13 - Feb 19 swing

S&P E-Minis maintain a softer tone following recent bearish price action. Sights are on key support and the bear trigger at 5559.75, the Mar 13 low. It has been pierced, a clear break of it would confirm a resumption of the downtrend that started Feb 19, and open 5483.30, a Fibonacci projection. MA studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term resistance has been defined at 5837.25, the Mar 25 high.