SPAIN DATA: April Manufacturing PMI: Surprisingly Weak; US Tariff Policy Cited

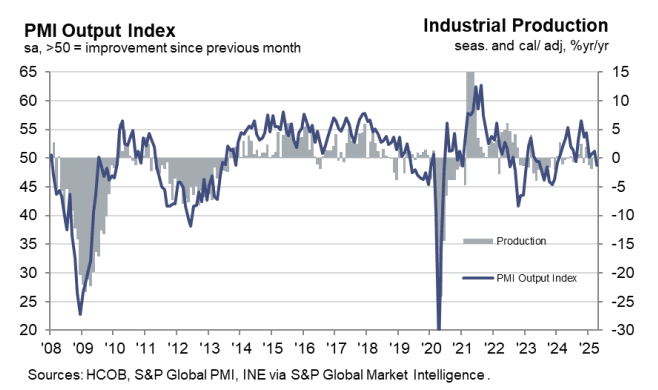

The Spanish April manufacturing PMI surprisingly fell to 48.1 (vs 50.1 cons, 49.5 prior). Following the flash Eurozone-wide release last week, we had estimated the ex-France and Germany average manufacturing PMI at 49.5, and the “rest of Eurozone” commentary had indicated a “solid growth of output, albeit with the pace of expansion easing slightly from that seen in March”.

This marks the fourth consecutive fall in the Spanish manufacturing PMI (from 53.3 in December), which has been followed by a deterioration of industrial production momentum. The recent national electricity outage will further drag on Q2 growth prospects.

Key notes from the release:

- “It was the third month in a row that new work has fallen and was often linked by firms to market instability and client uncertainty. This was attributed in some cases to US tariff policy, which also had a negative impact on international sales during the month”.

- “Production volumes declined for the first time since last August, though relatively modestly in the context of the steep reduction in new work”.

- “Weak current trends in output and new orders, alongside an uncertain outlook, led to a decline in buying activity. There was also a preference to utilise existing inventories”.

- “Confidence in the outlook for production deteriorated further”…”hiring activity broadly stagnated”.

- “Input costs rose only marginally in April”…” Although limited production and stock shortages were reported to have raised supplier prices, lower demand was noted by some panellists to have restricted vendor pricing power”.

- “Similarly, manufacturing selling prices continued to rise, but only slightly and to the weakest degree in 2025 so far”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Looking To Tsys For Cues

Gilts look to Tsys for cues early today, moving away from lows as the overnight weakness in U.S. paper is unwound.

- Futures back to little changed at 92.10.

- The short-term trend in the contract remains bearish, despite the recent correction.

- Initial support and resistance of note located at 91.59 and 92.42.

- Yields essentially flat across the curve.

- 2-Year yields are ~5bp off March lows, with gilt bulls failing to challenge that key short-term level (4.127%) yesterday.

- GBP STIRs now a little more dovish on the day, reversing modest early hawkish adjustments.

- BoE-dated OIS showing 53bp cuts through year-end vs. 52bp ahead of the gilt open.

- SONIA futures flat to +2.0.

- Little of note when it comes to local news.

- Wednesday’s UK speaker and data schedule is empty.

- The only real point of scheduled domestic interest comes via the GBP1.6bln auction of the 1.125% Sep-35 I/L gilt.

- This will leave focus on U.S. tariff decisions and data for much of the session.

CROSS ASSET: Bund is leading gains in Core Bonds

- Treasuries are starting to get dragged higher, European Govies lead, as Bund closed its Opening gap earlier.

The Immediate area of interest for Bund is still at 129.54/129.60. - For the US Tnotes (TYH5), while the March high is at 112.01, the March and the 2025 low in the 10yr Yield of 4.1040%, would equate today to 112.03+.

- US Emini is starting to tilt to the downside.

- USDJPY is paring some gains taking its cue from the move in Yields.

US TSYS: Supported By Screen Buying Programme, Liberation Day Outcome Eyed

Tsys supported by the early downtick in European equities, with the impending “Liberation Day” tariff announcements out of the U.S. front of mind.

- Yields back to little changed on the day, with the Asia-Pac weakness, driven by reports pointing to Trump considering some slightly more lenient tariffs, reversed.

- TY futures comfortably within yesterday’s range.

- A screen buying programme across TU, FV & TY futures ahead of the European cash equity open plays into the bid.