MNI US OPEN - Tsunami Waves Reach Coast of California

EXECUTIVE SUMMARY

- MNI FED PREVIEW - DIVIDING LINES

- TSUNAMI WAVES REACH CALIFORNIA AFTER WASHING ONTO HAWAII

- TRUMP SET TO MAKE FINAL CALL ON CHINA TARIFF TRUCE EXTENSION

- UPSIDE RISKS TO Q2 EUROZONE GDP MATERIALIZE

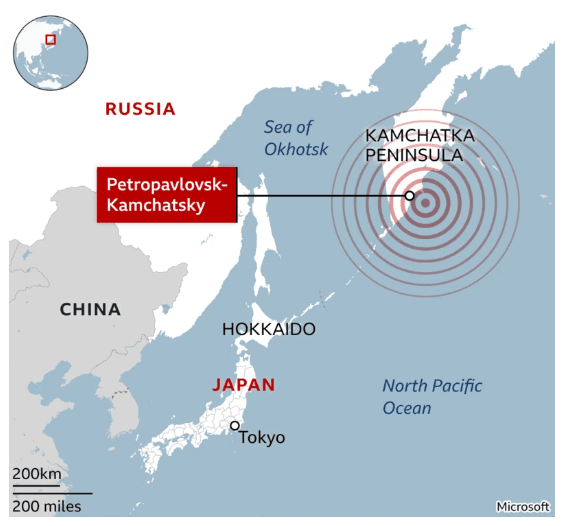

Figure 1: Magnitude 8.8 earthquake strikes off Russia's far eastern coast

Source: BBC graphic, United States Geological Survey (29 July 2025, 23:24 UTC)

NEWS

MNI FED PREVIEW - JULY 2025: Dividing Lines

With the Fed almost certain to hold the funds rate at 4.25-4.50% again at the July 29-30 meeting, focus will be on the degree to which the Committee signals openness to rate cuts resuming in the fall. The policy statement is unlikely to see meaningful changes, though Governor Waller and Vice Chair Bowman are widely expected to dissent in favor of a rate cut. The message from July is likely to look similar to that of June: a fairly divided Committee retains its overall easing bias but individual participants need varying degrees of certainty before supporting a resumption of the easing cycle.

MNI BOJ PREVIEW - JULY 2025: Focus On Presser After Trade Deal

The two-day Bank of Japan (BoJ) policy meeting concludes on 31 July, with the central bank set to release its quarterly “Outlook for Economic Activity and Prices”, its monetary policy statement, and hold a press conference with Governor Kazuo Ueda. The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting. Most analysts continue to expect the next rate hike to occur in late 2025 or January 2026. However, timing remains fluid.

GLOBAL (NYT): Tsunami Waves Reach California After Washing Onto Hawaii

An 8.8-magnitude earthquake that experts said could be the sixth largest on record struck in the North Pacific off Russia early Wednesday, prompting tsunami warnings and evacuations in Hawaii, Alaska, California and Japan and leaving millions anxiously awaiting waves that forecasters said could approach 10 feet in places. Tsunami waves reached the West Coast of the United States just before 1 a.m. local time, hitting parts of California and Washington State, and were expected to build through the night, according to the National Weather Service.

US/CHINA (BBG): Trump Set to Make Final Call on China Tariff Truce Extension

US President Donald Trump is set to make the final call on maintaining a tariff truce with China before it expires in two weeks, an extension that would mark a continued stabilization in ties between the world’s two biggest economies. The two sides agreed to extend their tariff truce, Chinese trade negotiator Li Chenggang told reporters in Stockholm without providing further details. Treasury Secretary Scott Bessent, who led the US delegation with Trade Representative Jamieson Greer, later said “our Chinese counterparts have jumped the gun a little.”

US/INDIA (BBG): Trump Says India May Get 20% to 25% Tariff But Not Yet Final

President Donald Trump said that India may be hit with a tariff rate of 20% to 25%, while cautioning that the final levy still hadn’t been finalized as the nations negotiate a trade deal ahead of an Aug. 1 deadline. “I think so,” Trump told reporters Tuesday when asked if that was a possible tariff rate for New Delhi. “India has been a good friend, but India has charged basically more tariffs than almost any other country,” Trump said aboard Air Force One as he returned to Washington from a five-day visit to Scotland. “You just can’t do that.”

US/RUSSIA (NYT): Trump Admits Financial Penalties on Russia ‘May or May Not’ Work

Just 24 hours after President Trump threatened Russia with financial penalties over the war in Ukraine, he seemed unsure on Tuesday about whether the strategy would even work. Speaking to reporters aboard Air Force One, Mr. Trump said that in 10 days, the United States may have to impose “tariffs and stuff.” “I don’t know if it’s going to affect Russia, because he wants to, obviously, probably keep the war going,” Mr. Trump said, referring to President Vladimir V. Putin. “But we’re going to put on tariffs and the various things you put on. It may or may not affect them. But it could.”

RUSSIA/UKRAINE (BBG): Poland’s Tusk Sees Signs Ukraine-Russia War May Be Halted

Poland’s Prime Minister Donald Tusk sees a chance that Russia’s ongoing full-scale invasion of Ukraine may be halted in the near future, he said at a press conference in Warsaw on Wednesday. “There are many signs pointing to the fact that the Russia-Ukraine war may be at least suspended in the nearest time,” he told reporters, without elaborating further.

CANADA (MNI): Canada Firms Are Mostly Absorbing Tariffs - CFIB

Canada's Federation of Independent Business said Tuesday its members are absorbing the cost of tariffs on shipments to and from the U.S., evidence why the trade dispute haven't boosted inflation much this year. Some 63% of CFIB members surveyed are sharing or paying the full cost of U.S. tariffs. For imports from the U.S. to Canada, about 70% are paying the full tariff. The online survey with 2,090 responses was taken July 10-24.

CHINA (MNI): China to Step Up Policy Support as Needed

MNI (Beijing) China will further enhance its proactive fiscal stance and moderately loose monetary policy to unlock existing policy effects fully, while stepping up intensity when needed, according to Xinhua News Agency following Wednesday’s Politburo meeting. Authorities pledged to accelerate the issuance and use of government bonds and improve the efficiency of fund deployment. The People’s Bank of China was tasked with maintaining ample liquidity, guiding lower social financing costs and increasing support for technology, consumption, small and medium-sized enterprises, and foreign trade.

CHINA (BBG): China’s Ruling Party to Hold Plenum on Five-Year Plan October

China’s ruling Communist Party will hold its next key conclave in October to chart development plans for the next five years, as the nation contends with risks to the economy at home and abroad. The 24-member Politburo announced the month for the gathering known as the fourth plenum after wrapping a meeting on Wednesday, according to the official Xinhua News Agency. The decision-making body didn’t reveal specific dates for the huddle of some 400 Central Committee members.

CHILE (BBG): Chile Cuts Rates to 4.75% and Keeps Guidance on More Easing

Chile’s central bank cut its interest rate for the first time this year and kept guidance for more monetary easing in coming quarters as a weak labor market crimps activity and inflation slows down. Policymakers led by Rosanna Costa voted unanimously to lower borrowing costs by a quarter-point to 4.75% late on Tuesday, as expected by all economists in a Bloomberg survey. In a statement, they wrote headline inflation eased more than forecast while job creation remains slow and unemployment is rising.

THAILAND (MNI): Constitutional Court Gives Suspended PM Until Aug 4 to File Defence

The Constitutional Court granted suspended Prime Minister Paetongtarn Shinawatra a 'final extension' and gave her until August 4 to file her defence paperwork in a case that may see her removed from the position of head of government. The Court added that it will proceed with the case regardless of whether Paetongtarn submits the documents on time.

DATA

EUROZONE DATA (MNI): Upside Risks to Q2 Eurozone GDP Materialize

- EUROZONE Q2 PRELIM FLASH GDP +0.1% Q/Q

- EUROZONE Q2 PRELIM FLASH GDP +1.4% Y/Y

Eurozone GDP printed 0.1% Q/Q in Q2, slightly stronger than consensus of 0.0% and slightly softer than the ECB's 0.2% staff projection. It was below Q1's outsized 0.6%. Ireland, which had a strong upward contribution in Q1, dragged the print lower this time at -1.0% Q/Q. Across the four major economies, detailed information on the Q1 data is lacking. Drivers across countries are mixed, with Germany mentioning stronger private and government consumption but weak investment, France seeing a material inventory contribution but weak domestic demand, while Italy and Spain both see positive domestic demand.

ECB DATA (MNI): July Wage Tracker Points to Continued Softening in Q1 2026

The ECB's forward looking wage tracker points to a continued decline in negotiation wage growth in Q1 2026. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling. Wage growth excluding one-off payments is seen at 2.61% Y/Y, down from an estimated 3.11% in Q4 2025. Note that the June iteration only captured negotiations up to Q4 2025. Revisions between the June and July iterations were minimal for 2025, but on net downward for 2024.

GERMANY DATA (MNI): Q2 Flash GDP as Weak as Expected, Negative Investment Contribution

- GERMANY PREL Q2 GDP SA -0.1% Q/Q, WDA +0.4% Y/Y

German Q2 flash GDP came in as expected, at -0.1% Q/Q (-0.1% consensus, +0.3% Q1 downwardly revised by 0.1pp). "Investment in equipment and construction in the second quarter of 2025 was lower than in the previous quarter, according to preliminary findings. Private and government consumption expenditure, on the other hand, rose after adjustment for price, seasonal and calendar effects", Destatis notes.

GERMANY DATA (MNI): Retail Sales Carry Little Signal for Q2 GDP Contribution

German retail sales printed stronger then consensus in June, at 1.0% M/M (0.5% cons; -0.6% prior, note that that was revised from -1.6%, underpinning the strength seen in June). Nonetheless, this means that on a 3m/3m comparison, retail sales printed a mere +0.3% in Q2, which is likely not enough to carry any strong signal for a Q2 GDP consumer spending contribution.

FRANCE DATA (MNI): June Consumer Spending Saved French GDP in Q2

French Q2 flash GDP was slightly stronger than expected at 0.3% Q/Q (vs 0.1% cons and prior). The details of the print were weak - consistent with much of the hard and soft economic data released through Q2. Total household consumption growth was 0.1% Q/Q (vs -0.3% prior). This component was likely saved by a much stronger-than-expected June consumer spending reading (0.6% M/M vs -0.3% cons, 0.1% prior). Prior to June, consumer spending was tracking at a -0.9% 3m/3m clip.

SPAIN DATA (MNI): Inflation Slightly Higher-Than-Expected in July

- SPAIN JUL FLASH CPI -0.1% M/M, +2.7% Y/Y

- SPAIN JUL FLASH CORE CPI +2.3% Y/Y

- SPAIN JUL FLASH HICP -0.4% M/M, +2.7% Y/Y

Spanish flash July HICP was a tenth above consensus on a rounded basis at 2.7% Y/Y (vs 2.6% cons, 2.3% prior). Core HICP (excluding energy and unprocessed foods) was estimated at 2.3% Y/Y (vs 2.2% prior). Flash CPI was also 2.7% Y/Y (vs 2.4% cons, 2.3% prior), with core CPI at 2.3% Y/Y (vs 2.2% cons and prior). The slighty higher-than-expected core CPI reading suggests services, non-energy industrial goods or processed foods components were behind the surprise in July, even if most of the annual acceleration came from energy.

ITALY DATA (MNI): Net Exports Drag on Q2 GDP

Italian Q2 flash GDP was weaker-than-expected at -0.1% Q/Q (vs 0.1% cons, 0.3% prior). With Germany in line at -0.1% Q/Q and Spain/France/Ireland a little stronger-than-expected, there may still be upside risks to the Eurozone-wide consensus of 0.0% Q/Q. Few details are provided in the Italian flash print. The press release notes that "there is a positive contribution by the domestic component (gross of change in inventories) and a negative contribution by the net export component".

SWITZERLAND DATA (MNI): KOF Recovers in July as US-Swiss Deal Remains in Pipeline

- SWISS KOF JUL ECONOMIC BAROMETER 101.1

The Swiss KOF Economic Barometer recovered in July to 101.1, above consensus of 97.9 and following June's 96.3 (revised from 96.1). The improved sentiment comes amid a US-Swiss trade deal remaining in the pipeline for now. "Among the indicator bundles included in the Economic Barometer, the indicators for manufacturing, for hospitality as well as for other services particularly reflect the positive developments. The indicators for foreign demand and for financial and insurance services, however, are under downward pressure", the KOF institute comments.

SWEDEN DATA (MNI): Only a Partial Recovery in June Retail Sales

May's historic fall in Swedish retail sales was only revised up two tenths to -4.6% M/M. As such, it still would have had a large downward impact on yesterday's weaker-than-expected Q2 flash GDP reading. Retail sales (ex-fuel) partly recovered in June, rising 2.5% M/M, but 3m/3m growth was still -0.6% (vs -0.5% in May, +0.9% in April). On an NSA monthly basis, it's worth noting that the seasonally weak May has been followed up by a seasonally strong June.

AUSTRALIA DATA (MNI): Aussie Trimmed CPI at 2.7%, 0.6% Q/Q

- AUSTRALIA Q2 CPI +0.6% Q/Q

- AUSTRALIA Q2 TRIMMED CPI +0.6% Q/Q

- AUSTRALIA MONTHLY JUN CPI 0.2% MM, 1.8% YY

Australia’s trimmed mean inflation slowed to 2.7% year-on-year in the June quarter, down 20 basis points from the previous period, with a quarterly increase of 0.6%, according to data released Wednesday by the Australian Bureau of Statistics, which also showed headline CPI easing 20bp to 2.1% y/y. The Reserve Bank of Australia had expected in May trimmed mean inflation, its preferred measure, to print at 2.6% in Q2, assuming a 4.0% cash rate. The actual cash rate remains at 3.85% following a 25bp reduction in May. The monthly CPI indicator for June showed trimmed mean inflation at 2.1% year-on-year, though the RBA places limited emphasis on the monthly reading and prefers the full-quarter data when assessing inflation.

FOREX: Awaiting the FOMC

- The Dollar saw its first negative start in over 5 days going into the European session, but most major FX pairs/crosses are now fairly steady as we await the FOMC later today.

- The Yen is still the best performer within G10, up 0.33% on the day, although looking at the price action, market participants have seen the USDJPY exchanging hands inside a 147.81/148.17 range for the past 8 hours.

- Some of the early overnight focus was on the Australian inflation data, which came below expectations.

- The AUD was still flat going into the European Govie open, but is now the worst small performer at the time of typing, down 0.12% and testing the 0.6500 figure, so far printed a 0.6497 low.

- Desks will now start to speculate that the RBA could be set to cut its rate as early as the next meeting on the 12th August.

- Looking ahead, there's plenty of data to take down before the expected unchanged Fed decision, including: US ADP, GDP, and Core PCE QoQ.

EGBS: Bund Futures Look Through Heavy Morning of Econ Data

Despite an extremely heavy morning of regional economic data, Bund futures have traded in a contained 33 tick range, currently unchanged at 129.66. Early rallies were limited by this morning’s heavy Italian supply, which has now passed. Broader macro focus remains on today’s US refunding announcement at 1330BST and the FOMC decision this evening.

- Initial resistance in Bunds is the 20-day EMA at 129.92, while key support and the bear trigger is not seen till 128.84. In the short-term, risks to Bunds may be tilted to the upside due to growth concerns stemming from the EU-US trade agreement, alongside potential front-running of supportive month-end extensions.

- German yields are up to 2bps lower, with the 10-year tenor outperforming. 10-year EGB spreads to Bunds are little changed.

- Eurozone GDP printed 0.1% Q/Q in Q2, slightly stronger than consensus of 0.0% and slightly softer than the ECB's 0.2% staff projection. It was below Q1's outsized 0.6%. July EC economic confidence was also stronger-than-expected at 95.8 (vs 94.5 cons, 94.2 prior).

- Meanwhile, Spanish flash July inflation was a tenth above consensus at 2.7% Y/Y (vs 2.6% cons, 2.3% prior).

GILTS: Tender Demand & Eyes on Month-End Underpin Rally

Gilts remain underpinned.

- Late Tuesday cues from Tsys provided support at the open, with solid demand at the GBP300mn tender of the 3.75% Jul-52 gilt then helping underpin after a pullback into the bidding deadline.

- A reminder that month-end index extension projections for gilts are sizeable, which could also be factoring into today’s rally.

- Futures have pierced resistance at the 20-day EMA (91.82). Bulls now eye the July 22 high (92.15). highs of 91.97 seen thus far. To the downside, well-defined key support comes in at the July 18 low (91.08).

- Benchmark yields 3-4bp lower, curve marginally flatter

- 2s10s and 5s30s remain in fairly close proximity to 75bp and 140bp, respectively, trading back from ’25 highs, but consolidating the bulk of the year-to-date steepening.

- GBP STIR pricing takes cues from the rally in the long end. SONIA futures flat to +1.5, BoE-dated OIS little changed, showing 46bp of easing through year-end, with ~90% odds of an August cut priced.

- Little of note on the UK calendar for the remainder of today, which will leave focus on broader headline flow, as well as the U.S. quarterly refunding announcement and GDP data ahead of the FOMC decision.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 3.994 | -22.3 |

Sep-25 | 3.960 | -25.7 |

Nov-25 | 3.808 | -40.9 |

Dec-25 | 3.754 | -46.3 |

Feb-26 | 3.647 | -57.0 |

Mar-26 | 3.611 | -60.6 |

EQUITIES: E-Mini S&P Remains in a Bullish Price Sequence

The trend condition in Eurostoxx 50 futures is unchanged, it remains bullish and short-term weakness appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a resumption of gains would refocus attention on the bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00. The trend set-up in S&P E-Minis remains bullish. Recent cycle highs once again confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6173.21. Support at the 20-day EMA is at 6322.32.

- Japan's NIKKEI closed lower by 19.85 pts or -0.05% at 40654.7 and the TOPIX ended 11.54 pts higher or +0.4% at 2920.18.

- Elsewhere, in China the SHANGHAI closed higher by 6.006 pts or +0.17% at 3615.717 and the HANG SENG ended 347.52 pts lower or -1.36% at 25176.93.

- Across Europe, Germany's DAX trades lower by 1.54 pts or -0.01% at 24215.53, FTSE 100 lower by 20.18 pts or -0.22% at 9116.13, CAC 40 up 25.11 pts or +0.32% at 7882.47 and Euro Stoxx 50 up 2.66 pts or +0.05% at 5381.86.

- Dow Jones mini down 6 pts or -0.01% at 44810, S&P 500 mini up 4.5 pts or +0.07% at 6410.5, NASDAQ mini up 34.25 pts or +0.15% at 23486.25.

Time: 10:00 BST

COMMODITIES: Gold Continues to Trade Close to Support at 50-Day EMA

WTI futures traded higher yesterday highlighting an extension of the current corrective cycle. $69.41, the 50.0% retracement of the Jun 23-24 downleg, has been pierced. A continuation higher would open $70.96 next, the 61.8% retracement point. On the downside, support to watch is the 50-day EMA, at $65.02. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3323.0, the 50-day EMA. A clear break of this level would signal scope for a deeper retracement and expose the next key support at $3282.8, the Jul 9 low. Key near-term resistance is $3439.0, the Jul 23 high. A break of this hurdle would be bullish.

- WTI Crude down $0.28 or -0.4% at $68.89

- Natural Gas up $0.02 or +0.67% at $3.163

- Gold spot up $6.41 or +0.19% at $3332.89

- Copper down $0.95 or -0.17% at $561.5

- Silver down $0.1 or -0.26% at $38.108

- Platinum down $4.85 or -0.35% at $1387.48

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 30/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/07/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/07/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/07/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 30/07/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/07/2025 | 1430/1030 | BOC press conference | ||

| 30/07/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 30/07/2025 | 1800/1400 | *** | FOMC Statement | |

| 31/07/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/07/2025 | 2350/0850 | ** | Industrial Production | |

| 31/07/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/07/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/07/2025 | 0130/1130 | * | Building Approvals | |

| 31/07/2025 | 0130/1130 | ** | Retail Trade | |

| 31/07/2025 | 0130/1130 | *** | Retail trade quarterly | |

| 31/07/2025 | 0130/1130 | ** | Trade price indexes | |

| 31/07/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 31/07/2025 | 0600/0800 | ** | Import/Export Prices | |

| 31/07/2025 | 0630/0830 | ** | Retail Sales | |

| 31/07/2025 | 0645/0845 | *** | HICP (p) | |

| 31/07/2025 | 0645/0845 | ** | PPI | |

| 31/07/2025 | 0755/0955 | ** | Unemployment | |

| 31/07/2025 | 0800/1000 | *** | Bavaria CPI | |

| 31/07/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 31/07/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 31/07/2025 | 0900/1100 | ** | Unemployment | |

| 31/07/2025 | 0900/1100 | *** | HICP (p) | |

| 31/07/2025 | 1000/1200 | ** | PPI | |

| 31/07/2025 | 1200/1400 | *** | HICP (p) | |

| 31/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 31/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 31/07/2025 | 1230/0830 | * | Payroll employment | |

| 31/07/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/07/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/07/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/07/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 31/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 31/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result |