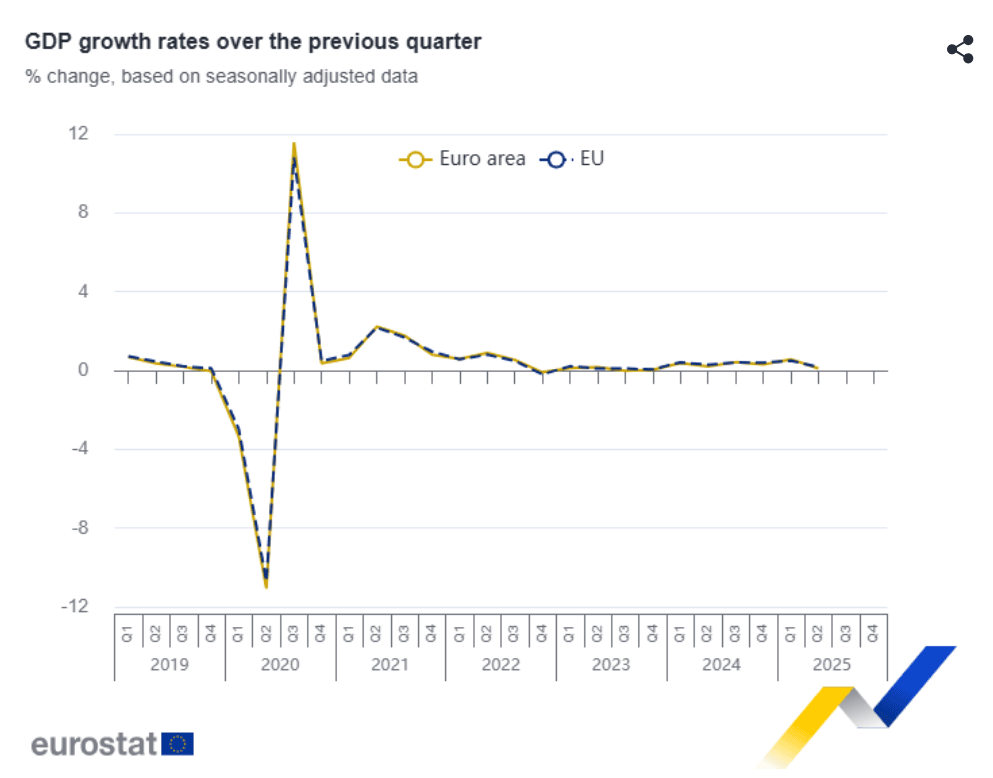

EUROZONE DATA: Upside Risks To Q2 Eurozone GDP Materialize

Eurozone GDP printed 0.1% Q/Q in Q2, slightly stronger than consensus of 0.0% and slightly softer than the ECB's 0.2% staff projection. It was below Q1's outsized 0.6%.

- Ireland, which had a strong upward contribution in Q1, dragged the print lower this time at -1.0% Q/Q.

- Across the four major economies, detailed information on the Q1 data is lacking. Drivers across countries are mixed, with Germany mentioning stronger private and government consumption but weak investment, France seeing a material inventory contribution but weak domestic demand, while Italy and Spain both see positive domestic demand.

- Summarising the main quarterly GDP prints released yesterday/this morning:

- Eurozone: 0.1% Q/Q vs 0.0% cons, 0.6% prior.

- Germany: -0.1% Q/Q vs -0.1% cons, 0.3% prior.

- France: 0.3% Q/Q vs 0.1% cons, 0.1% prior.

- Italy: -0.1% Q/Q vs 0.1% cons, 0.3% prior.

- Spain: 0.7% Q/Q vs 0.6% cons, 0.6% prior.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: MNI Projects 2.0-2.1% Y/Y German National CPI, Core 2.6%

From state-level data that equates to 89.1% weighting of the national June flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by around 2.0-2.1% Y/Y (2.1% prior) and rose 0.0-0.1% M/M. See the tables below for full calculations.

- Analyst consensus stands at 2.2% Y/Y and 0.2% M/M, so there should be some downside risks to headline inflation.

- Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies around 2.6% Y/Y (2.8% prior). This would be the joint lowest rate since June 2021 for the measure.

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is normally the same.

| Y/Y | June (Reported) | May (Reported) | Difference |

| North Rhine Westphalia | 1.8 | 2.0 | -0.2 |

| Hesse | 2.3 | 2.3 | 0.0 |

| Bavaria | 1.8 | 2.1 | -0.3 |

| Brandenburg | 2.2 | 2.2 | 0.0 |

| Baden Wuert. | 2.3 | 2.2 | 0.1 |

| Berlin | 2.0 | 1.8 | 0.2 |

| Saxony | 2.4 | 2.3 | 0.1 |

| Rhineland-Palatinate | 1.8 | 1.7 | 0.1 |

| Lower Saxony | 2.2 | 2.3 | -0.1 |

| Saarland | 1.9 | 1.8 | 0.1 |

| Saxony-Anhalt | 2.5 | 2.8 | -0.3 |

| Weighted average: | 2.06% | for | 89.1% |

| M/M | June (Reported) | May (Reported) | Difference |

| North Rhine Westphalia | -0.1 | 0.2 | -0.3 |

| Hesse | 0.1 | 0.0 | 0.1 |

| Bavaria | -0.1 | 0.1 | -0.2 |

| Brandenburg | 0.2 | 0.0 | 0.2 |

| Baden Wuert. | 0.2 | -0.1 | 0.3 |

| Berlin | 0.2 | -0.1 | 0.3 |

| Saxony | 0.2 | 0.0 | 0.2 |

| Rhineland-Palatinate | 0.2 | -0.1 | 0.3 |

| Lower Saxony | 0.2 | 0.1 | 0.1 |

| Saarland | 0.1 | -0.1 | 0.2 |

| Saxony-Anhalt | 0.1 | 0.0 | 0.1 |

| Weighted average: | 0.05% | for | 89.1% |

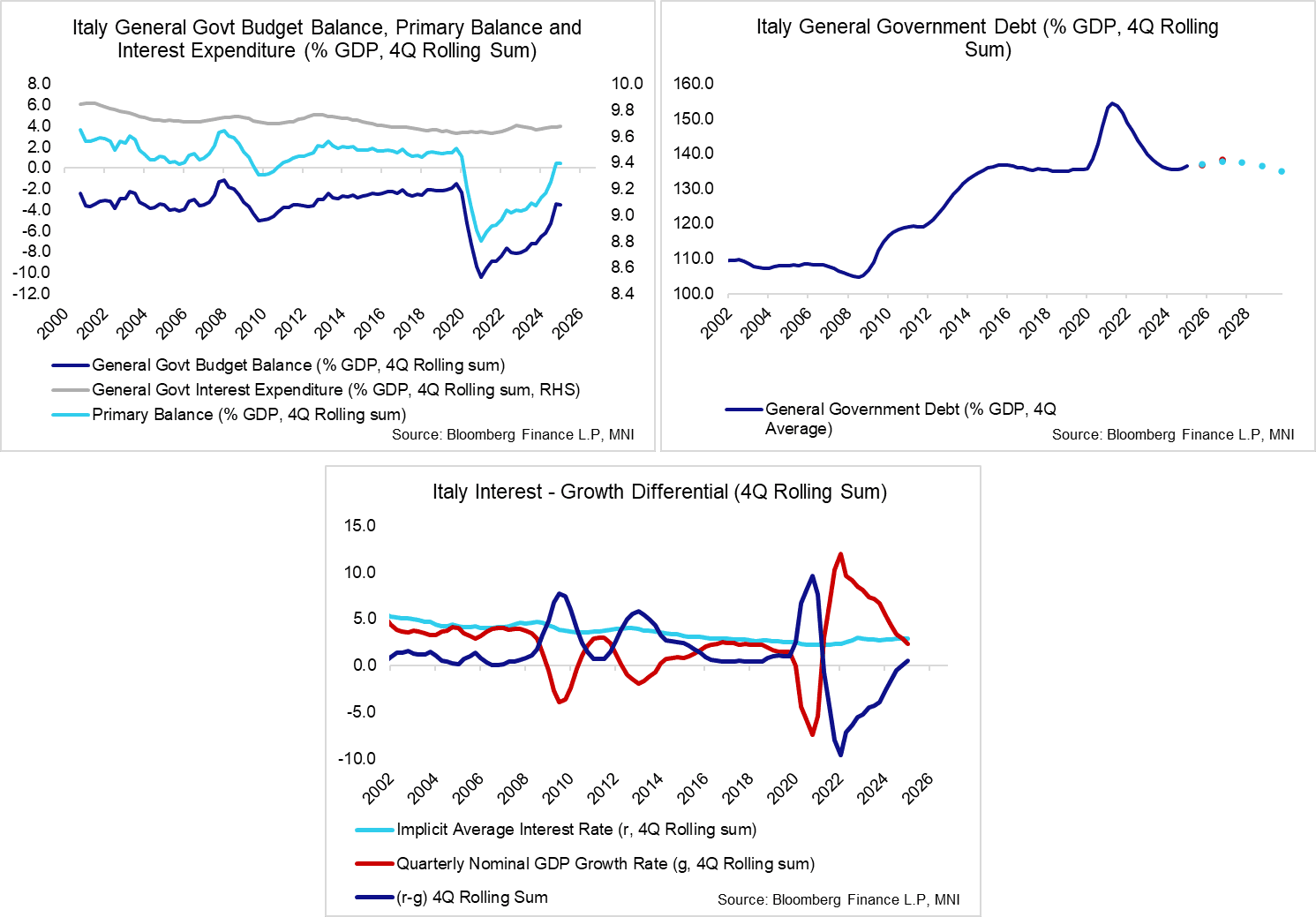

EUROPEAN FISCAL: Italy Runs Primary Surplus In Q1, But Interest Expenses Rising

On a 4Q rolling sum basis, the Italian budget deficit ticked up a tenth to 3.5% of nominal GDP in Q1 – far less dramatic than the 8.5% single-quarter figure reported by newswires. Interest expenditures (also on a 4Q rolling basis) ticked up to 4.0% GDP (vs 3.9% prior), meaning the government still ran a primary surplus of 0.4% for the second consecutive quarter.

- In its May forecast round, the EC projected the Italian deficit at 3.3% in 2025 and 2.9% in 2026. This was similar to the Government’s medium-term fiscal plan projections presented last year (3.3% in 2025, 2.8% in 2026). Bloomberg consensus on the other hand is slightly less optimistic on 2026 fiscal consolidation, with the median analyst projecting the budget deficit at 3.4% in 2025 and 3.2% in 2026.

- Expenditures rose to 50.8% of GDP in Q1 (4Q rolling, vs 50.6% prior), with revenues ticking up to 47.3% (vs 47.1% prior).

- The debt/GDP ratio (4Q average) rose to 136.5% (vs 135.8% in Q4). The EC expects debt/GDP at 136.7% in 2025 and 138.2% in 2026 (Italian Government: 136.9% in 2025 and 137.8% in 2026). Medium-term fallout from the post-covid Superbonus scheme continues to push debt/GDP higher in the coming years, but the Government expects the ratio to begin falling from 2028.

- While Italian fiscal consolidation still appears intact, one less positive development in Q1 was the interest – nominal growth differential (“r-g”) turning positive (0.5pp minus 0.0pp in Q4). This means that interest expenses are growing faster than the economy. If the Government stops running primary surpluses with this dynamic in place, it would put total debt on an unstable and increasing path once again.

FED: Bostic Sees Firms' Tariff Uncertainty lnto 2026, MNI Livestream Later Today

Atlanta Fed’s Bostic (non-voter) on CNBC’s Squawk Box Europe: “I’m hearing more [businesses] say that they may not expect this whole thing [response to tariffs and other economic factors] to play out, to where they’re at their final strategy, till even 2026, so this could be a much more extended period than I think many expect,”

Bostic spoke to Reuters last week, reiterating his view for just one 25bp cut late this year.

A reminder that MNI has a livestream with Bostic later today at 1000ET/1500BST. You can register for an in-depth discussion on the economic outlook here: https://mni.marketnews.com/RaphaelBostic