MNI US OPEN - China and US Confirm Further Framework Details

EXECUTIVE SUMMARY

- LUTNICK SAYS US-CHINA TRADE TRUCE SIGNED, 10 DEALS IMMINENT

- IRAN DISMISSES US CLAIM OF NUCLEAR TALKS RESUMING NEXT WEEK

- FRENCH FLASH INFLATION ABOVE CONSENSUS, SERVICES REBOUND

- TOKYO CORE INFLATION SLOWS IN JUNE

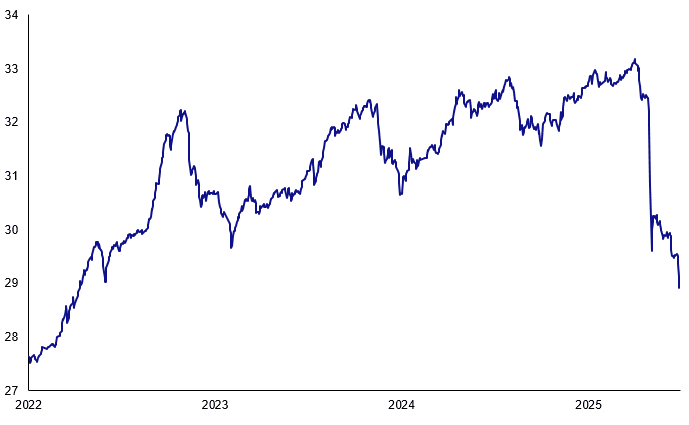

Figure 1: USD/TWD briefly pierces 29.00 for first time since 2022 (chart shows low price)

Source: MNI/Bloomberg Finance L.P.

NEWS

US (BBG): Lutnick Says US-China Trade Truce Signed, 10 Deals Imminent

The US and China finalized a trade understanding reached last month in Geneva, US Commerce Secretary Howard Lutnick said, adding that the White House has imminent plans to reach agreements with a set of 10 major trading partners. The China deal, which Lutnick said had been signed two days ago, codifies the terms laid out in trade talks between Beijing and Washington, including a commitment from China to deliver rare earths used in everything from wind turbines to jet planes.

US/CHINA (MNI): China and U.S. Confirm Further Framework Details

MNI (Beijing) China and the U.S. have further confirmed details of the framework for implementing the consensus reached by the two heads of state on June 5 and consolidating the outcomes of the Geneva economic and trade talks, the Ministry of Commerce said on Friday. China will review and approve qualified export applications for controlled items in accordance with the law, and the U.S. will cancel a series of restrictive measures taken against China accordingly, the spokesperson added.

US/CHINA (BBG): China’s $50 Billion Chip Fund Switches Tack to Fight US Curbs

China’s main chip investment fund is planning to focus on the country’s key shortcomings in sectors like lithography and semiconductor design software, adjusting its approach to better overcome US efforts to stop its technological advances. The third phase of the state-backed National Integrated Circuit Industry Investment Fund, better known as Big Fund III, will focus on backing local companies and projects in areas considered bottlenecks to technological advances, people familiar with the matter said.

US/IRAN (BBG): Iran Dismisses US Claim of Nuclear Talks Resuming Next Week

Iran denied that nuclear talks with the US are scheduled to resume, diminishing prospects for diplomacy after President Donald Trump suggested a deal could come as early as next week. “I say explicitly that no agreement, arrangement or discussion has taken place regarding the initiation of new negotiations,” Foreign Minister Abbas Araghchi said in an interview with state TV late Thursday. “Some of the speculation about the resumption of negotiations should not be taken seriously.”

US (FT): US Treasury Asks Congress to Scrap Foreign Revenge Tax in Trump Bill

The US Treasury department has called on Congress to scrap a provision in Donald Trump’s flagship budget bill that would allow Washington to raise taxes on foreign investments, reversing a plan that had spooked Wall Street. Treasury secretary Scott Bessent said on Thursday that the measure was no longer needed because he had secured concessions for US companies to the new OECD global minimum tax regime.

US (BBG): House Plans Single Vote to Move Genius and Clarity Crypto Bills

House Republicans aim to get the Senate’s landmark stablecoin legislation — known as the Genius Act — to President Donald Trump’s desk for signature as soon as the week of July 7, according to people with direct knowledge of the strategy. Their strategy, subject to change, would also allow the House to bring its crypto market-structure bill — known as the Clarity Act — to a full floor vote. The plan calls for the two separate measures to advance in a single procedural vote, the people said, asking not to be identified discussing behind-the-scenes legislative efforts.

ECB (FT): ECB Beat Inflation Without Heavy Economic Costs, Says Departing Hawk

The European Central Bank’s battle against surging inflation after the pandemic has caused far less damage to the wider Eurozone economy than rate-setters anticipated, a veteran policymaker told the Financial Times. Klaas Knot, whose second term as president of the Dutch central bank DNB ends at the end of June, said he has been “positively surprised” at the limited economic fallout from the ECB’s dramatic tightening of monetary policy from mid-2022. “We would have been prepared to accept more economic pain [to battle inflation] but luckily we didn’t have to,” the longest-serving member of the ECB’s 26-member governing council said.

UK (The Times): Keir Starmer Gives in to Welfare Rebels by Offering to Water Down Cuts

Sir Keir Starmer has offered to protect hundreds of thousands of disabled people currently claiming benefits from the government’s welfare reforms, as part of a package of costly concessions to buy off Labour rebels. In a move that would cost the Treasury £1.5 billion, the prime minister has offered to restrict change to personal independence payments (PIP) to new claimants, protecting 370,000 existing recipients who have been vocal over their concerns. The Institute for Fiscal Studies said the concession would require Rachel Reeves, the chancellor, to “raise taxes or find other savings” to make up the shortfall.

BOE (FT): BoE Urged to Curb Bond Sales Investors Say Could ‘Reignite’ Sell-off

The Bank of England is facing growing calls to scale back its bond-selling programme later this year, as investors warn it risks pushing up borrowing costs further and adding to pressure on a weakening UK economy. The central bank is shrinking its portfolio of bonds accumulated during bursts of quantitative easing over the past decade and a half, as it attempts to bring its balance sheet back to a more normal size.

CHINA/EU (MNI EXCLUSIVE): China Advisors - EU Talks Hinge on Europe Deal With U.S.

Advisors in Beijing, and a senior EU diplomat, assess the likely outcome of an upcoming China-EU summit. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

TAIWAN (BBG): Taiwan Dollar’s Dramatic Reversal Stokes Bets on FX Intervention

The Taiwan dollar saw a sharp move lower in late Friday trading, after earlier climbing past a key level for the first time since 2022, stoking speculation the central bank may have intervened to curb the rally. State banks were seen aggressively buying the US dollar to slow the local currency’s appreciation, according to two traders, who asked not to be identified as they weren’t authorized to speak publicly. Taiwan’s central bank has been seeking to tamp down speculation in foreign exchange markets this year after the currency’s rally.

MEXICO (MNI): Banxico Signals Slower Pace, Drops 'Restrictive'

The Central Bank of Mexico signaled Thursday it may slow the pace of rate cuts at its next meeting, after delivering the seventh consecutive interest rate cut and the fourth straight 50-basis-point reduction to 8.00%. Deputy Governor Jonathan Heath dissented in favor of keeping rates on hold. On the other hand, Banxico removed from the statement the reference to rates needing to be restrictive, indicating that it may be targeting a neutral level by the end of the cycle.

COLOMBIA (BBG): Moody’s, S&P Downgrade Colombia on Fiscal Rule Suspension

Moody’s Ratings and S&P Global Ratings downgraded Colombia’s credit, citing the worsening debt burden and the decision to suspend the fiscal rule that curbed government borrowing. Moody’s cut the nation’s rating one notch from Baa2 to the lowest investment grade, as the government failed to rein in spending after revenues fell short of forecasts. S&P, which already rated foreign-currency bonds as junk, cut the local bonds below investment grade as well to BB+.

DATA

GERMANY DATA (MNI): IFO Employment Barometer Deteriorates in June

The IFO employment barometer decreased to 93.7 points in June, from 95.1 in May and not far away from April's 93.9. "Despite improved sentiment in the economy, the labour market has not yet managed to turn the corner. There is still a lack of orders for new hires," IFO comments. In manufacturing, the indicator declined for the first time after 5 consecutive increases, to a balance of -19.9 (-15.1 prior).

FRANCE DATA (MNI): Services Rebound as French Flash Inflation Above Consensus

- FRANCE JUN CPI +0.3% M/M, +0.9% Y/Y

- FRANCE JUN HICP +0.4% M/M, +0.8% Y/Y

French flash June HICP was a tenth higher than consensus at 0.82% Y/Y (vs 0.7% cons, 0.59% prior). There was a notable rebound in services according to the CPI details - some analysts had expected services to rebound in June, but others had pencilled in a broadly unchanged Y/Y rate. CPI was also a bit higher than expected at 0.93% Y/Y (vs 0.8% cons, 0.66%

prior).

FRANCE MAY CONSUMER SPENDING +0.2% M/M, -0.5% Y/Y (MNI)

FRANCE MAY CONSUMER MANUF SPENDING -0.7% M/M, -0.4% Y/Y (MNI)

FRANCE MAY PPI -0.8% M/M, +0.2% Y/Y (MNI)

SPAIN DATA (MNI): June Inflation Driven Higher by Fuel and Food

- SPAIN JUN FLASH HICP +0.6% M/M, +2.2% Y/Y

- SPAIN JUN FLASH CPI +0.6% M/M, +2.2% Y/Y

- SPAIN JUN FLASH CORE CPI +2.2% Y/Y

Spanish preliminary HICP came in as expected on the yearly rate at 2.2% Y/Y (vs 2.2% cons; 2.0% prior) and the sequential reading at 0.6% M/M (0.6% cons). The national CPI came slightly higher than expectated at +2.2% Y/Y (vs 2.1% cons; 2.0% prior) and 0.6% M/M (vs 0.4% cons of only 7 analysts). Core CPI came in inline with expectations, at +2.2% Y/Y (vs 2.2% cons and prior). The headline rate was driven higher by fuel prices, and, to a lesser extent, to increases in food and non-alcoholic beverages, INE comments.

NORWAY DATA (MNI): Non-seasonally Adjusted Registered Unemployment Unch at 2.0%

NAV has once again not published seasonally adjusted registered unemployment data due to a recent change in IT systems, but the non-seasonally adjusted registered unemployment rate was steady at 2.0%. The number of registered unemployed persons rose to 60,614, from 59,566 in May and 56,953 last June. This was still below the Q1 average of 66,090 though, Despite the inconvenience of no seasonally adjusted data, the report doesn't point to any notable deterioration in labour market conditions.

JAPAN DATA (MNI): June Tokyo Core CPI Rises 3.1% vs. May 3.6%

- JAPAN JUNE TOKYO CORE CPI +3.1% Y/Y; MAY +3.6%

- JAPAN JUNE TOKYO CORE-CORE CPI +3.1% Y/Y; MAY +3.3%

- JAPAN JUNE SERVICES PRICES +2.1% Y/Y; MAY +2.2%

Tokyo’s core inflation slowed to 3.1% y/y in June from 3.6% in May, but remained above the Bank of Japan’s 2% target for the eighth consecutive month, data from the Ministry of Internal Affairs and Communications showed Friday. The deceleration was mainly driven by a smaller rise in crude oil prices (+3.6% vs. +8.7% in May), though this was partially offset by higher prices for non-perishable food (+7.2% vs. +6.9%) and household durable goods (+3.3% vs. +2.7%).

JAPAN DATA (MNI): Household Assets at JPY2,195 Trln End-March

The balance of financial assets held by Japanese households stood at JPY2,195 trillion at the end of March, up 0.3% y/y, but down from the record JPY2,230 trillion seen at the end of December, preliminary fund flow data released by the Bank of Japan on Friday showed. Cash and deposits held by households totaled JPY1,120 trillion, rising 0.1% y/y, and accounted for 51.0% of total household financial assets, underscoring continued reluctance by Japanese households to invest in financial products.

FOREX: USD Index Consolidates at Lower Levels

- Currency markets are more sanguine early Friday, but the lack of any reversal off lows for the USD Index provides another bearish signal as the price holds close to the cycle low of 96.997. This keeps the falling wedge pattern in play, with a firm break of the downtrendline drawn off the late 2024 lows still a possibility ahead of next week's payrolls print.

- This morning's SEK strength has taken a breather in the last 20 minutes, but EURSEK and USDSEK are nonetheless 0.7% below this morning's levels. There wasn't an obvious fundamental driver for the earlier selloff (this morning's Swedish PPI data was actually quite dovish), but yesterday's lows remain intact for both crosses.

- USDCAD has pulled back from its recent highs. The primary downtrend remains intact and short-term gains appear to have been corrective. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low.

- Core PCE data will mark the highlight of the Friday calendar, with final University of Michigan confidence numbers set to follow. The central bank speaker slate is busier: ECB's Rehn & Cipollone speak, as well as Fed's Williams, Hammack & Cook

EGBS: 10-Year Bund Yields Find Support at 2.60%

10-year Bund yields found solid support at 2.60%, a level which has capped topside throughout this month. 10-year yields are now little changed on the session at 2.57%, while the curve exhibits a light twist flattening bias.

- Schatz yields are up 1.5bps, taking cues from EUR STIRs after slightly higher-than-expected French inflation data this morning. Optimism surrounding US trade negotiations has also supported broader risk sentiment.

- Bund futures are -3 ticks at 130.46, up from today’s session low of 130.17 (also the June 16 low). Futures continue to trade below the June 13 high, but this still appears to be a correction from a technical standpoint.

- Italy sold 5/10-year BTPs this morning (and a floating rate bond), with the issuance digested smoothly. The 10-year BTP/Bund spread is 0.5bps wider at 89bps despite this morning’s 1% European equity future rally.

- Eurozone economic confidence was slightly weaker-than-expected at 94.0 (vs 94.8 cons and prior).

- Germany announced a 13.9% rise in the statutory minimum wage by 2027.

- Belgium's gross borrowing requirements have increased by E7.83bln to E52.52bln "on the back of higher net financing requirements (+ 8.0 billion euro) whose increase is, amongst others, due to rising defence spending."

- Broader macro focus turns to this afternoon’s US PCE report, while ECB’s Villeroy, Rehn and Cipollone are scheduled to speak.

GILTS: Light Pressure This Morning, Tight Ranges on the Day

Gilts came under light selling pressure in early European trade, but have stabilised alongside similar moves in global peers, with ranges remaining tight.

- Firmer-than-expected European inflation data and increased optimism surrounding a Sino-U.S. trade agreement provided the early weight.

- Futures last -13 at 93.12, narrow 93.06-36 range on the day.

- The bullish technical outlook remains intact, but momentum is stalling a little.

- Initial support located at the 20-day EMA (92.64), while the June 25 high (93.57) presents initial resistance.

- Yields flat to 1bp higher across the curve, 10s under the most pressure.

- Fundamentals continue to point to further curve steepening after the pullback from ’25 highs in spreads.

- Spread to Bunds last 191bp, unable to force a close below 190bp despite this week’s tightening (spread move largely driven by the German issuance outlook). A break below 190bp would expose the April closing low (184.8bp).

- Local focus remains on PM Starmer’s decision to pare back welfare cuts, owing to pressure from his own party. Negative fiscal readthrough for the UK, odds of tax hikes/spending cuts elsewhere rise.

- Post-settlement/early Friday modest dovish moves in GBP STIRs fade given cues from the long end.

- BoE-dated OIS showing ~53.5bp of cuts through year-end after respecting the 55bp zone over the past couple of sessions.

- ~80% odds of a 25bp cut priced for August and 26.5bp showing through September.

- Little of note on the UK calendar ahead of the weekend, which will leave macro and geopolitical cues at the fore.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.015 | -20.2 |

Sep-25 | 3.951 | -26.6 |

Nov-25 | 3.780 | -43.8 |

Dec-25 | 3.682 | -53.5 |

Feb-26 | 3.547 | -67.0 |

Mar-26 | 3.507 | -71.0 |

EQUITIES: E-Mini S&P Remains Above Bull Trigger, Trading at Cycle Highs

The trend condition in Eurostoxx 50 futures remains bearish, however, the recovery from Monday’s low appears to be a potential reversal. The contract has traded through the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme and signal scope for a stronger recovery. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of Monday’s 5194.00 low would reinstate a bearish theme. The trend condition in S&P E-Minis is unchanged, it remains bullish and this week’s fresh cycle highs reinforces current conditions. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared, this opens 6249.00, the Feb 21 high. Key support is at the 50-day EMA - at 5952.18. A clear break of it would signal a reversal.

- Japan's NIKKEI closed higher by 566.21 pts or +1.43% at 40150.79 and the TOPIX ended 35.85 pts higher or +1.28% at 2840.54.

- Elsewhere, in China the SHANGHAI closed lower by 24.226 pts or -0.7% at 3424.227 and the HANG SENG ended 41.25 pts lower or -0.17% at 24284.15.

- Across Europe, Germany's DAX trades higher by 193.54 pts or +0.82% at 23842.14, FTSE 100 higher by 45.19 pts or +0.52% at 8780.84, CAC 40 up 93.31 pts or +1.23% at 7650.62 and Euro Stoxx 50 up 50.79 pts or +0.97% at 5294.82.

- Dow Jones mini up 103 pts or +0.24% at 43821, S&P 500 mini up 14.5 pts or +0.23% at 6209.5, NASDAQ mini up 70.5 pts or +0.31% at 22739.75.

Time: 10:00 BST

COMMODITIES: Gold Below Two Important Short-Term Support Points

WTI futures maintain a softer tone following the reversal from Monday’s high. Support to watch is at the 50-day EMA, at $64.55. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high. The trend condition in Gold remains bullish and the latest pullback is considered corrective - for now. Note that today’s move down has resulted in a test of two important short-term support points; $3290.9, the 50-day EMA, and 3294.8, a trendline drawn from the Dec 30 ‘24 low. A clear break of both support points would signal scope for a deeper correction - this would expose $3245.5. A reversal higher would refocus attention $3451.3, the Jun 16 high.

- WTI Crude up $0.53 or +0.81% at $65.75

- Natural Gas up $0.1 or +2.69% at $3.619

- Gold spot down $38.83 or -1.17% at $3289.72

- Copper down $1.45 or -0.28% at $510.6

- Silver down $0.61 or -1.68% at $36.0649

- Platinum down $58.78 or -4.13% at $1363.5

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 27/06/2025 | 1000/1200 | ** | PPI | |

| 27/06/2025 | 1130/0730 | New York Fed's John Williams | ||

| 27/06/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 27/06/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 27/06/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 27/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 27/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 27/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 27/06/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 27/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 27/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 28/06/2025 | 1530/1730 | ECB Schnabel On Panel At Petersberger Sommerdialog 2025 |