MNI US MARKETS ANALYSIS: USD Off Lows, Curves Steeper Into PCE

Highlights:

- Core global FI curves bear steepen

- USD recovers from early session lows, GBP weakness noted in FX trade

- U.S. PCE data headlines ahead of the weekend

US TSYS: Bear Steeper With 5s30s Near Recent Highs Ahead Of PCE, Cook Hearing

Treasuries are bear steeper ahead of another important docket, with data focus on the monthly PCE report for July at 0830ET before US District Judge Jia Cobb begins the Fed Gov. Cook hearing at 1000ET.

- Cash yields are 0.2-2.5bp higher, with the long end leading increases.

- Curves give back some of yesterday’s flattening and hold close to recent steeps, including 5s30s at 120.5bp (+1.8bp) vs fresh multi-year highs of 122.8bp late on Wednesday.

- TYZ5 trades at 112-16+ (-02+) having eased off yesterday’s late fresh recent high of 112-20+. Volumes are subdued at a cumulative 215k.

- That 112-20+ marks latest resistance with some attention now on 113-00, whilst support is seen at 111-29 (20-day EMA) in the event of a strong PCE report.

- Data: PCE Jul (0830ET), Advance trade Jul (0830ET), Wholesale/retail inventories Jul/Jul P (0830ET), MNI Chicago PMI Aug (0945ET), U.Mich consumer survey Aug F (1000ET), Kansas City Fed serv Aug (1100ET)

- Fedspeak: None scheduled

- Politics: No public events scheduled for President Trump but presumably high likelihood of Cook-related comments

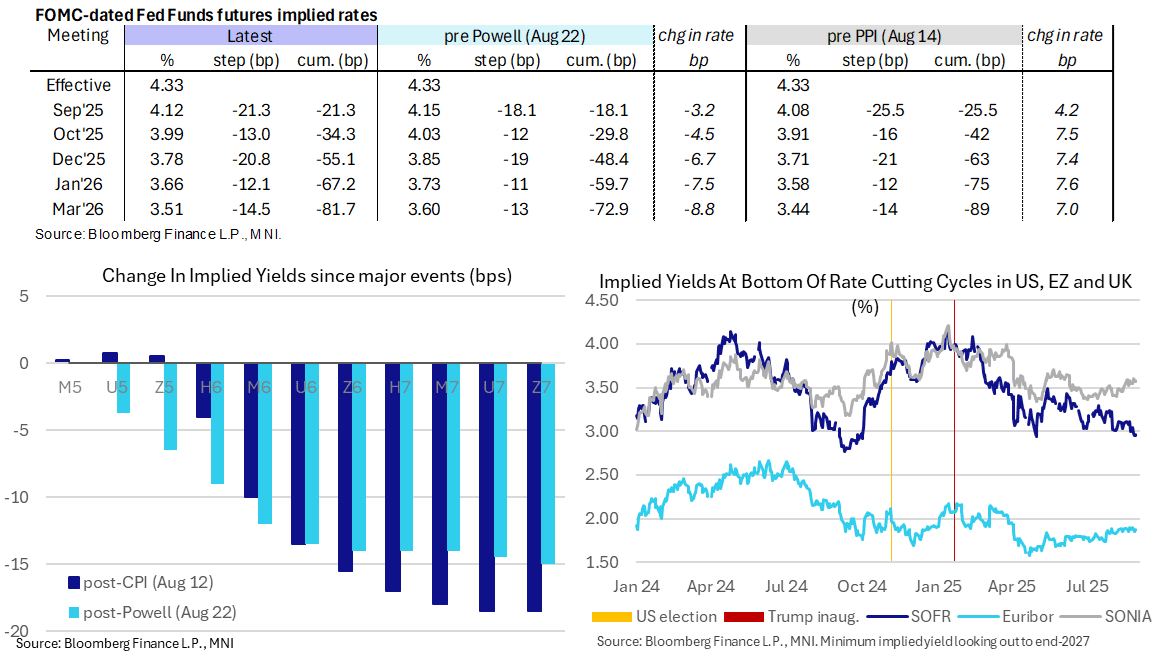

STIR: Fed Rates Await PCE and Cook Hearing, 21.5bp Cuts Seen Next Month

Fed Funds implied rates are little changed ahead of an important docket, with little net change after a dovish but not increasingly so Waller after the close yesterday.

- Cumulative cuts from 4.33% effective: 21.5bp Sep, 34.5bp Oct, 55bp Dec, 67bp Jan and 81.5bp Mar.

- The SOFR implied terminal yield of 2.96% (SFRH7) is near unchanged on the day as it hovers at recent lows with nearly 140bp of cuts from current levels seen.

- Ahead, the July PCE report at 0830ET – we’ve seen unrounded analyst estimates average 0.28% M/M for July, unlikely to have been altered by yesterday’s small downward revision to Q2.

- US District Judge Jia Cobb will begin the Cook hearing at 1000ET today after Cook requested a restraining order as she seeks to remain in her role. FHFA’s Pulte sent a new (third) criminal referral against Cook late yesterday.

- Fed Gov. Waller yesterday in a speech entitled “Let’s Get On With It” (link): "I anticipate additional cuts over the next three to six months, and the pace of rate cuts will be driven by the incoming data.”

- “While I judge that the FOMC should have begun this process in July, based on the data in hand, I don't believe that a cut of larger than 25 basis points is needed in September. That view, of course, could change if the employment report for August, due out a week from tomorrow, points to a substantially weakening economy and inflation remains well contained.”

- “Based on the median of FOMC participants’ estimates of the longer-run value of the federal funds rate, neutral is 125 to 150 basis points lower than the current setting”.

SOFR: Fresh Positions Set In Most Futures On Thursday

OI data points to net short setting dominating through the reds before net long setting came to the fore in the blues and greens, as the SOFR futures strip twist flattened on Thursday. Instances of cover were fairly isolated and limited in comparison.

| 28-Aug-25 | 27-Aug-25 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM5 | 1,162,438 | 1,175,158 | -12,720 | Whites | +59,452 |

| SFRU5 | 1,452,635 | 1,424,817 | +27,818 | Reds | +22,762 |

| SFRZ5 | 1,536,660 | 1,512,042 | +24,618 | Greens | +27,262 |

| SFRH6 | 1,136,897 | 1,117,161 | +19,736 | Blues | +10,809 |

| SFRM6 | 943,065 | 927,483 | +15,582 | ||

| SFRU6 | 922,498 | 924,621 | -2,123 | ||

| SFRZ6 | 953,844 | 959,710 | -5,866 | ||

| SFRH7 | 739,950 | 724,781 | +15,169 | ||

| SFRM7 | 798,171 | 790,688 | +7,483 | ||

| SFRU7 | 638,080 | 637,254 | +826 | ||

| SFRZ7 | 621,728 | 607,192 | +14,536 | ||

| SFRH8 | 394,025 | 389,608 | +4,417 | ||

| SFRM8 | 327,561 | 315,331 | +12,230 | ||

| SFRU8 | 221,752 | 225,798 | -4,046 | ||

| SFRZ8 | 241,676 | 240,213 | +1,463 | ||

| SFRH9 | 162,195 | 161,033 | +1,162 |

EUROPEAN INFLATION: MNI Projects 2.1% Y/Y German National CPI, Core 2.7-2.8%

From state-level data that equates to 89.1% weighting of the national July flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by around 2.1% Y/Y (2.0% prior) and rose around 0.0% M/M. See the tables below for full calculations.

- Analyst consensus stands at 2.0% Y/Y and 0.0% M/M, risks to consensus appear to be skewed to the upside.

- Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies between 2.7-2.8% Y/Y (2.7% prior).

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is generally the same.

| Y/Y | August (Reported) | July (Reported) | Difference |

| North Rhine Westphalia | 2.0 | 1.8 | 0.2 |

| Hesse | 2.4 | 2.4 | 0.0 |

| Bavaria | 2.1 | 1.9 | 0.2 |

| Brandenburg | 2.5 | 2.2 | 0.3 |

| Baden Wuert. | 2.5 | 2.3 | 0.2 |

| Berlin | 2.4 | 2.1 | 0.3 |

| Saxony | 2.2 | 2.1 | 0.1 |

| Rhineland-Palatinate | 1.9 | 1.8 | 0.1 |

| Lower Saxony | 2.2 | 1.9 | 0.3 |

| Saxony-Anhalt | 2.6 | 2.5 | 0.1 |

| Weighted average: | 2.21% | for | 88.0% |

| M/M | August (Reported) | July (Reported) | Difference |

| North Rhine Westphalia | 0.1 | 0.2 | -0.1 |

| Hesse | 0.0 | 0.3 | -0.3 |

| Bavaria | 0.1 | 0.3 | -0.2 |

| Brandenburg | 0.0 | 0.3 | -0.3 |

| Baden Wuert. | -0.1 | 0.4 | -0.5 |

| Berlin | 0.0 | 0.3 | -0.3 |

| Saxony | 0.0 | 0.2 | -0.2 |

| Rhineland-Palatinate | 0.1 | 0.2 | -0.1 |

| Lower Saxony | 0.1 | 0.3 | -0.2 |

| Saxony-Anhalt | -0.1 | 0.2 | -0.3 |

| Weighted average: | 0.03% | for | 88.0% |

OAT: Spread Vs. Bunds & French CDS Remain Below Highs Seen in '24 & '25

French 5-Year CDS remains below the spike highs witnessed earlier in ’25 and back in ’24, pointing to a slightly more sanguine market outlook on French creditworthiness when compared to other recent instances of political stress. Meanwhile, the 10-Year OAT/Bund spread hasn’t challenged late ‘24/early ’25 highs.

- Several factors may have limited OAT spread & CDS widening thus far:

- The incumbent coalition’s fiscal delivery to date.

- The moderation in the far-right RN’s spending preferences in recent months, indicating a less combative fiscal stance if the party does come into legislative power.

- Already well-defined expectations of increased French political risk in the Autumn (albeit with the recent news bringing the timeline forward a little).

- French sovereign credit rating downgrade risks already being embedded in the market for some time.

- Most desks have described the recent moves as roughly “fair”, albeit with further widening risks highlighted, contingent on the outcome of the impending confidence vote on the Bayrou government (8 September) and any subsequent snap election (legislative paralysis is also a key risk here).

Fig. 1: 10-Year OAT/Bund Spread & French 5-Year CDS (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

EUROPEAN/UK ISSUANCE UPDATE:

UK DMO UPDATE: FQ3 Plans: No real surprises but two 2031 linker auctions

Overall, all broadly as we had expected with two auctions of the 0.125% Aug-31 linker the only minor surprise for u.

- Syndication: As expected, confirmed as a new 15-year conventional gilt in October (no maturity date given, we still favour Jan-41) while the November linker syndication wasn't committed to.

- Shorts: 6 auctions with new 3/5-year gilts launched as expected:

- 3-year maturing 22 May 2029: Launching 8 October and reopening on 4 November and 3 December.

- 5-year maturing 7 March 2031: Launching on 23 October and reopening on 20 November and 16 December.

- Medium: 4 auctions including a new long 7-year gilt launched:

- 7-year maturing 7 March 2033: Launching on 29 October

- 10-year: 3 auctions as we expected: 2 October, 12 November, 10 December

- Longs: All as expected: 2 auctions plus the 15-year syndication in October:

- 1.50% Jul-53 green gilt: 21 October

- 30-year 5.375% Jan-56 gilt: 2 December

- Linkers: 4 auctions (plus the one syndication) but all skewed to the shorter end:

- 0.125% Aug-31 Linker: 15 October and 9 December (two auctions of this linker is a little bit of a surprise but not a huge shock).

- 1.125% Sep-35 Linker: 1 October and 28 October (we had expected two auctions)

FOREX: USD Index in Favour as US July PCE Approaches

Despite some moderate two-way swings, the USD index is trading on a firmer footing Friday, currently up around 0.2% as we approach the NY crossover. This keeps a more constructive short-term tone for the greenback present as markets await important July PCE data out of the US, the MNI Chicago PMI and month end.

- Sterling weakness is standing out early Friday, as GBPUSD extends intra-day declines to 0.41%. Despite the dip, spot remains comfortably off Wednesday’s lows at 1.3417 and key short-term support of 1.3391, the Aug 22 low. This dynamic has helped bolster EURGBP to resistance at 0.8674. A break above this level would signal a stronger reversal, placing the cross at its highest levels in three weeks.

- Although moves remain broadly contained, the Kiwi dollar sits atop the G10 leaderboard as NZDUSD modestly extends its bounce from firm pivot support at 0.5800 to around a big figure. Bearish conditions overall for NZDUSD might suggest that good supply is seen into 50-day EMA resistance around 0.5930. The dovish RBNZ has seen the AUDNZD surge higher breaking back above 1.1000 convincingly. There have been some primary signs overnight of momentum stalling above 1.1100, however, look for dips back towards 1.1000/1.1030 to be supported.

- USDJPY has broadly been consolidating back above 147.00, with spot continuing to respect yesterday’s low of 146.66 and last Friday’s post Powell low at 146.58, the most notable short-term supports.

- Elsewhere, USDCHF briefly dipped its toe back below the 0.8000 mark after reaching fresh one-month lows yesterday. Supportive but grinding price action for the swissie has seen EURCHF consolidate back below the 0.94 to current spot levels of 0.9350, very familiar territory for the cross in recent months.

- Aside from PCE and the MNI Chicago PMI, the goods trade balance and personal income data are also schedule, as well as the latest revision of UMich survey data. Canadian GDP data fills out the North American calendar ahead of the weekend.

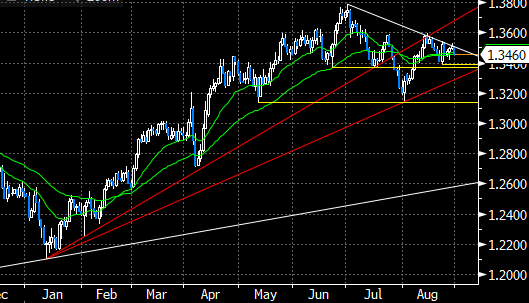

FOREX: Intra-Day GBPUSD Weakness Extends, Key Support Just Below 1.34

In most recent trade, the US dollar is back on the front foot, weighing most notably on sterling which allows GBPUSD to extend intra-day declines to 0.41%. Despite the dip, spot remains comfortably off Wednesday’s lows at 1.3417 and key short-term support of 1.3391, the Aug 22 low.

- A break lower would signal scope for a move towards 1.3315, the 61.8% retracement of the Aug 1 - 14 bull leg. Furthermore, trendline support drawn from the year’s lows would then come back into focus, of which a breach may threaten the broader medium-term uptrend that has been evident this year. This level intersects around 1.3290.

- We previously noted that JP Morgan remains of the view that investors should be using any GBP rallies to set up bearish multi-month exposure covering the UK budget. As part of JPM’s macro trade recommendations, they suggest keeping GBP shorts vs EUR, CHF, NOK & SEK.

- Separately, ING note that an indication that French politics is having a limited FX impact is EURGBP, which has faced only limited downside pressure since the start of the week. ING thinks a test of 0.86 remains possible, even though their longer-term view is less optimistic on GBP given the possibility of a dovish rethink of BoE cuts later in the autumn. For GBPUSD, they still think a structural break above 1.35 is a matter of when rather than if.

Source: MNI - Market News/Bloomberg Finance L.P.

FX OPTIONS: Expiries for Aug29 NY cut 1000ET (Source DTCC)

- EURUSD: 1.1625 (4.15bn), 1.1650 (835mln), 1.1700 (1.04bn), 1.1715 (513mln), 1.1725 (1.06bn)

- USDJPY: 146.50 (1.24bn), 147.00 (391mln), 147.50 (921mln)

- AUDUSD: 0.6500 (944mln), 0.6515 (477mln)

- USDCNY: 7.1400 (450mln)

- USDZAR: 17.6500 (231mln)

EQUITIES: S&P E-Minis Bull Cycle Remains In Play

S&P E-Minis bulls remain in the driver’s seat and the contract traded to a fresh cycle high yesterday. This maintains the bullish price sequence of higher highs and higher lows. Attention is on 6543.75, a 2.00 projection of the Apr 7 - 10 - 21 price swing. Pivot support to watch lies at 6326.74, the 50-day EMA. First support lies at 6436.50, the 20-day EMA.

- The trend set-up in EUROSTOXX 50 futures is bullish and the pullback from the Aug 22 high appears corrective - for now. However, support at 5376.70, the 50-day EMA, has been pierced. A clear break of this average would strengthen a S/T bearish threat and signal scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. Resistance to watch is 5522.00, the Aug 22 high.

COMMODITIES: Bull Cycle In Gold Remains In Play

Gold traded higher Thursday. The medium-term trend condition remains bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. Resistance to watch is $3439.0, the Aug 23 high. A break of this level would expose the key resistance and bull trigger at $3500.1, the Apr 22 low. On the downside, the first key support to watch is $3268.2, the Jul 30 low. Initial support lies at $3311.6, the Aug 20 low.

- Despite recent gains, a bear cycle in WTI futures remains intact and the latest recovery appears corrective. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

| Date | GMT/Local | Impact | Country | Event |

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 29/08/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 29/08/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 29/08/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 29/08/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/08/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 29/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 29/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 29/08/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/08/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/08/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 01/09/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/09/2025 | 0130/1130 | Business Indicators | ||

| 01/09/2025 | 0130/1130 | * | Building Approvals | |

| 01/09/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 01/09/2025 | 0530/0730 | ** | Retail Sales | |

| 01/09/2025 | 0700/0900 | Employment and Unemployment (p) | ||

| 01/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/09/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 01/09/2025 | 0830/0930 | ** | BOE M4 | |

| 01/09/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/09/2025 | 0900/1100 | ** | EZ Unemployment | |

| 01/09/2025 | 1200/1400 | ECB Schnabel Chairs Panel at ECB Legal Conference | ||

| 01/09/2025 | 1400/1600 | ECB Cipollone Chairs Panel at ECB Legal Conference | ||

| 01/09/2025 | 1800/2000 | ECB Lagarde Speech at ECB Legal Conference |