OAT: Spread Vs. Bunds & French CDS Remain Below Highs Seen in '24 & '25

French 5-Year CDS remains below the spike highs witnessed earlier in ’25 and back in ’24, pointing to a slightly more sanguine market outlook on French creditworthiness when compared to other recent instances of political stress. Meanwhile, the 10-Year OAT/Bund spread hasn’t challenged late ‘24/early ’25 highs.

- Several factors may have limited OAT spread & CDS widening thus far:

- The incumbent coalition’s fiscal delivery to date.

- The moderation in the far-right RN’s spending preferences in recent months, indicating a less combative fiscal stance if the party does come into legislative power.

- Already well-defined expectations of increased French political risk in the Autumn (albeit with the recent news bringing the timeline forward a little).

- French sovereign credit rating downgrade risks already being embedded in the market for some time.

- Most desks have described the recent moves as roughly “fair”, albeit with further widening risks highlighted, contingent on the outcome of the impending confidence vote on the Bayrou government (8 September) and any subsequent snap election (legislative paralysis is also a key risk here).

Fig. 1: 10-Year OAT/Bund Spread & French 5-Year CDS (bp)

Source: MNI - Market News/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

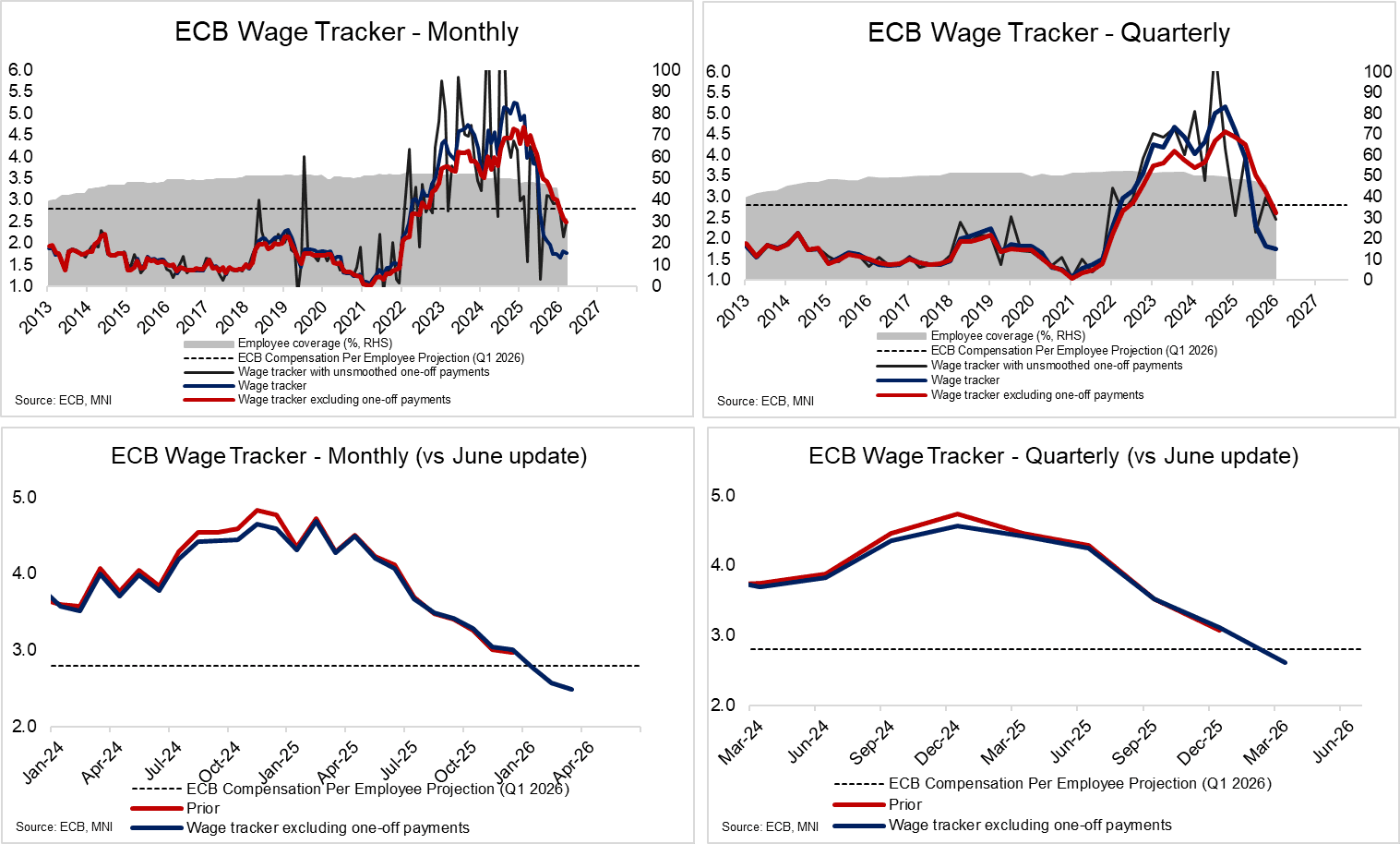

ECB: July Wage Tracker Points To Continued Softening In Q1 2026

The ECB’s forward looking wage tracker points to a continued decline in negotiation wage growth in Q1 2026. Overall, the results are consistent with a further softening in services inflation pressures in the coming years, in line with ECB signalling.

- Wage growth excluding one-off payments is seen at 2.61% Y/Y, down from an estimated 3.11% in Q4 2025. Note that the June iteration only captured negotiations up to Q4 2025. Revisions between the June and July iterations were minimal for 2025, but on net downward for 2024.

- Meanwhile, the Q1 2026 figures will likely be revised in the coming months as employee coverage increases. Current coverage is just 32.5% (vs 45.3% coverage in Q4 2025).

- Still, 2.61% negotiated wage growth is below the ECB’s 2.8% projection for Q1 2026 compensation per employee growth.

SONIA OPTIONS: More Upside Call Spread

SFIQ5 96.15/96.20cs, bought for 0.6 in 5k.

OIL: Russia Supply Concerns Continue To Underpin, Despite U.S. & OPEC Capacity

Crude prices remain underpinned after registering strong gains so far this week, despite the bounce in the USD.

- Our commodities team note that oil prices pushed above the recent range after U.S. President Trump outlined the new early August deadline for a Russia/Ukraine ceasefire.

- Looking forwards, focus is on the risk of supply disruption from further sanctions on Russian oil, but President Trump doesn’t appear concerned about supply matters, suggesting the U.S. will increase its oil output to counter any related disruptions.

- Elsewhere, OPEC is expected to increase its production target for September at its August 3 meeting. Many analysts expected the rise to lead to a market oversupply later this year and into 2026.