UK DMO UPDATE: FQ3 Plans: No real surprises but two 2031 linker auctions

Overall, all broadly as we had expected with two auctions of the 0.125% Aug-31 linker the only minor surprise for us (we had

- Syndication: As expected, confirmed as a new 15-year conventional gilt in October (no maturity date given, we still favour Jan-41) while the November linker syndication wasn't committed to.

- Shorts: 6 auctions with new 3/5-year gilts launched as expected:

- 3-year maturing 22 May 2029: Launching 8 October and reopening on 4 November and 3 December.

- 5-year maturing 7 March 2031: Launching on 23 October and reopening on 20 November and 16 December.

- Medium: 4 auctions including a new long 7-year gilt launched:

- 7-year maturing 7 March 2033: Launching on 29 October

- 10-year: 3 auctions as we expected: 2 October, 12 November, 10 December

- Longs: All as expected: 2 auctions plus the 15-year syndication in October:

- 1.50% Jul-53 green gilt: 21 October

- 30-year 5.375% Jan-56 gilt: 2 December

- Linkers: 4 auctions (plus the one syndication) but all skewed to the shorter end:

- 0.125% Aug-31 Linker: 15 October and 9 December (two auctions of this linker is a little bit of a surprise but not a huge shock).

- 1.125% Sep-35 Linker: 1 October and 28 October (we had expected two auctions)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Firmer To Start, Futures Stick To Recent Range, Long End Tender Due

Gilts firm early on, taking cues from post-7-Year auction price action in U.S. Tsys as opposed to the two-way, non-committal start for Bunds.

- Futures through yesterday’s high, bulls test Monday’s best levels, with the contract topping out at 91.86 for now.

- Note that the contract has pierced the 20-day EMA (91.82). A move higher would target the July 22 high (92.15). Well-defined key support comes in at the July 18 low (91.08).

- Yields 2-3bp lower, parallel shift across the curve.

- 2s10s and 5s30s remain in fairly close proximity to 75bp and 140bp, respectively, trading back from ’25 highs, but consolidating the bulk of the year-to-date steepening.

- Fundamentals (potential for a deeper BoE easing cycle vs. market pricing, fiscal fragility and tepid economic growth) point to further steepening risks, although a more activist approach from policymakers (both the DMO & BoE) when it comes to preventing spikes higher in long end yields presents a risk to that idea. As does pre-existing steepener positioning.

- BoE-dated OIS continues to show ~46bp of cuts through year-end.

- Little of note on the UK data calendar today, which will leave focus on EUR data (Eurozone GDP) ahead of the FOMC decision & U.S. GDP data.

- On the issuance side, the DMO will tender GBP300mln of the 3.75% Jul-52 gilt.

STIR: Euribor Futures Off Session Lows, Upside Risks To Q2 GDP Print

Euribor futures have moved away from session lows since the European cash open, currently flat to -1.5 ticks through the blues. Trendline support in ERH6, drawn from the May 2024 low, remains intact. National data released so far suggests there may be upside risks to analysts’ 0.0% Q/Q Eurozone-wide GDP projection (released 1000BST today). However, we would argue that markets have already incorporated a slightly better-than-expected growth picture following last week’s ECB decision/press conference. A reminder that the ECB projected a 0.2% Q/Q reading in its June macroeconomic projections.

- French Q2 flash GDP was 0.3% Q/Q, above the 0.1% consensus. Although skewed higher by inventories, the French data follows a stronger-than-expected reading in Spain yesterday (0.7% Q/Q vs 0.6% cons) and only a modest 1.0% Q/Q fall in Ireland. Some analysts had pencilled in a more severe reversal of Q1 Irish tariff frontloading.

- Meanwhile, the Eurozone July flash inflation round kicked off with a slightly higher-than-expected reading in Spain (2.7% Y/Y vs 2.6% prior). Other major countries’ prints are due tomorrow. MNI preview here .

- Markets still lean in favour of one more 25bp cut this cycle, with OIS pricing 20bps of easing through March 2026. Some more dovish rhetoric from the likes of Rehn and Villeroy last week, alongside the MNI Policy Team’s latest sources piece, have limited further hawkish repricing in EUR STIRs for now.

- Other regional data shouldn’t be as market moving as GDP (ECB wage tracker, EC July survey). Broader macro focus remains on today’s US refunding announcement and the BOC/Fed decisions.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-25 | 1.891 | -3.2 |

| Oct-25 | 1.856 | -6.7 |

| Dec-25 | 1.772 | -15.1 |

| Feb-26 | 1.754 | -16.9 |

| Mar-26 | 1.724 | -19.9 |

| Apr-26 | 1.727 | -19.6 |

| Jun-26 | 1.733 | -19.1 |

| Jul-26 | 1.736 | -18.7 |

| Source: MNI/Bloomberg Finance L.P. | ||

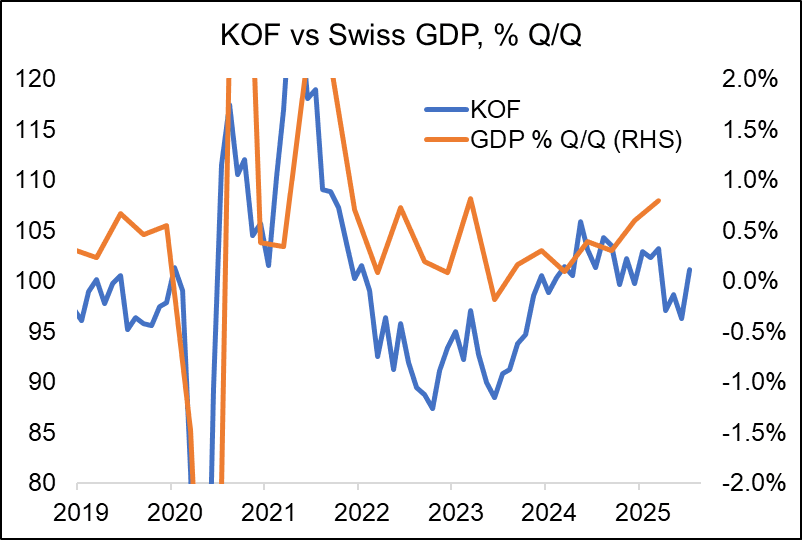

SWITZERLAND DATA: KOF Recovers In July As US-Swiss Deal Remains In Pipeline

The Swiss KOF Economic Barometer recovered in July to 101.1, above consensus of 97.9 and following June's 96.3 (revised from 96.1). The improved sentiment comes amid a US-Swiss trade deal remaining in the pipeline for now.

- “Among the indicator bundles included in the Economic Barometer, the indicators for manufacturing, for hospitality as well as for other services particularly reflect the positive developments. The indicators for foreign demand and for financial and insurance services, however, are under downward pressure”, the KOF institute comments.

- The 15% US-EU trade deal appears to be seen negatively in Switzerland on balance, with fears that the country also will end up with less favourable export conditions going forward. A trade agreement with the US seen as detrimental for Switzerland would have the potential to weigh on sentiment in the country going forward.

- From a monetary policy perspective, today's print will be of limited significance as the SNB's main focus is on inflation amid the continued CPI Y/Y readings around 0% in the country.