FOREX: USD Index in Favour as US July PCE Approaches

- Despite some moderate two-way swings, the USD index is trading on a firmer footing Friday, currently up around 0.2% as we approach the NY crossover. This keeps a more constructive short-term tone for the greenback present as markets await important July PCE data out of the US, the MNI Chicago PMI and month end.

- Sterling weakness is standing out early Friday, as GBPUSD extends intra-day declines to 0.41%. Despite the dip, spot remains comfortably off Wednesday’s lows at 1.3417 and key short-term support of 1.3391, the Aug 22 low. This dynamic has helped bolster EURGBP to resistance at 0.8674. A break above this level would signal a stronger reversal, placing the cross at its highest levels in three weeks.

- Although moves remain broadly contained, the Kiwi dollar sits atop the G10 leaderboard as NZDUSD modestly extends its bounce from firm pivot support at 0.5800 to around a big figure. Bearish conditions overall for NZDUSD might suggest that good supply is seen into 50-day EMA resistance around 0.5930. The dovish RBNZ has seen the AUDNZD surge higher breaking back above 1.1000 convincingly. There have been some primary signs overnight of momentum stalling above 1.1100, however, look for dips back towards 1.1000/1.1030 to be supported.

- USDJPY has broadly been consolidating back above 147.00, with spot continuing to respect yesterday’s low of 146.66 and last Friday’s post Powell low at 146.58, the most notable short-term supports.

- Elsewhere, USDCHF briefly dipped its toe back below the 0.8000 mark after reaching fresh one-month lows yesterday. Supportive but grinding price action for the swissie has seen EURCHF consolidate back below the 0.94 to current spot levels of 0.9350, very familiar territory for the cross in recent months.

- Aside from PCE and the MNI Chicago PMI, the goods trade balance and personal income data are also schedule, as well as the latest revision of UMich survey data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (U5) Holding On To Its Gains

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-28 High Jul 3

- RES 1: 111-14+ High Jul 22

- PRICE: 111-12 @ 11:30 BST Jul 30

- SUP 1: 110-19+/08+ Low Jul 24 / Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures traded higher on Tuesday. Recent gains resulted in a break of the 20-day EMA, strengthening the recovery that began mid-July. Note too that resistance at 111-13+, the Jul 10 high, has been pierced. A clear break of it would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low.

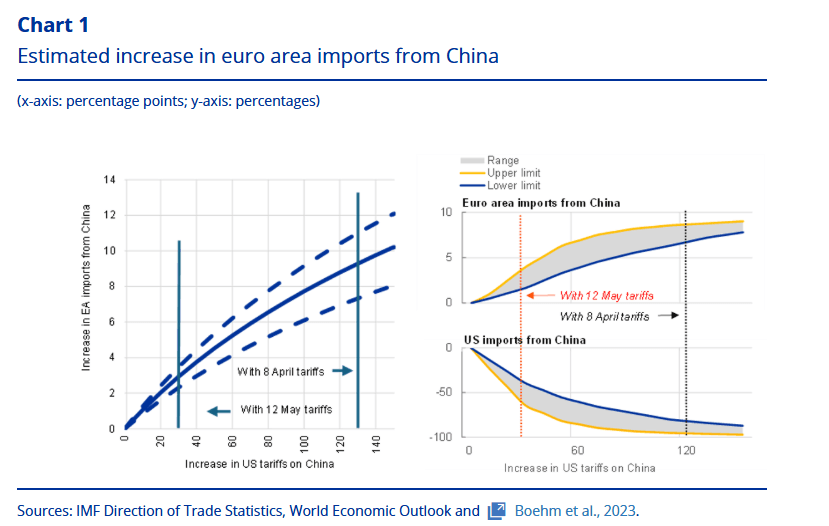

ECB: Worst Case Scenario Of Chinese Trade Diversion Would Reduce HICP By 0.15pp

An ECB staff blog, published today, suggests a 10% increase in Euro area imports from China under a severe trade scenario could reduce non-energy industrial goods inflation by 0.5pp in 2026, impliyng a negative peak impact on headline HICP inflation of 0.15pp. The estimates are based on the same severe trade scenario outlined in the June macroeconomic projections, where the US effective tariff rate on Chinese goods is 135%. Of course, the current effective tariff rate is closer to ~30% following the May 12 trade agreement, which looks to have been extended for another 90 days after talks between the US and China in Stockholm this week. As such, the estimates should be considered a worst case scenario, not a forecast based on current conditions.

- Staff note that the Euro area could be more impacted by Chinese trade diversion at present compared to 2018 due to:

- A similar composition of Chinese exports to the US and the EU

- "Established supply chain links, which have expanded since the last China-US trade war, and ongoing industrial upgrades in China facilitate the redirection of trade flows"

- "Chinese businesses have laid the groundwork to facilitate faster market entry."

- "The depreciation of the Chinese renminbi makes Chinese goods cheaper and more attractive for European importers."

- "Many [Chinese] firms, especially those in final goods production, still have room to absorb reduced profit margins".

- Following a 10% rise in Chinese imports, "assuming that domestic demand remains the same in the short term, this increase in imports would result in an excess supply of goods equivalent to 1.3% of overall goods consumption. For consumers to absorb this additional volume of imported goods – either by replacing other imports or substituting domestic production – the prices of Chinese imports would need to decrease. Specifically, our calculations indicate that lower Chinese import prices would reduce overall import prices by 1.6%."

- "But it will take some time for consumer prices to drop. While stronger supply from China may trigger a swift decline in import prices, consumer prices for non-energy industrial goods (NEIG) tend to respond more gradually, with the strongest impact materialising one to one-and-a-half years after the initial shock".

EU: Commission-18 Countries Apply For EUR127bln In Defence Loans Under SAFE

The European Commission has confirmed that an initial 18 member states have applied for a combined EUR127bln in loans to fund military procurement as part of the Security Action for Europe (SAFE) Defence Instrument. Belgium, Bulgaria, Czechia, Estonia, Greece, Spain, France, Croatia, Italy, Cyprus, Latvia, Lithuania, Hungary, Poland, Portugal, Romania, Slovakia and Finland have all applied under the scheme, with applications running to 30 November.

- Euractiv outlines the process of application, assessment, and disbursal of funds: "Member states now have six months from the entry into force of the Regulation [29 May] to submit their initial national plans, which the Commission will then assess. Following a Commission proposal, the Council is expected to adopt implementing decisions, which will include the size of the loan and any pre-financing. Pre-financing, which can be up to 15% of the loan, will ensure that support can be paid swiftly to cover the most urgent needs, potentially starting in 2025. Member states will need to report on the progress of implementation when they submit their payment requests, which can be done twice a year. The last approval for disbursements can take place until 31 December 2030."

- The SAFE loans are seen as a major component of the 'Readiness 2030' plans (formerly known as 'ReArm Europe', but changed due to political sensitivities in Italy and Spain), alongside allowing the 'national escape clause' of the Stability and Growth Pact to allow for increased defence spending up to an additional 1% of GDP.