MNI US MARKETS ANALYSIS - USD Off Lows as Tariffs Reinstated

Highlights:

- Greenback bounces off lows, but USD Index still well off the week's highs

- German national CPI seen slowing ahead of next week's EZ print, ECB decision

- HKD forward discount trimmed sharply as USD/HKD approaches weak-side of trading band

US TSYS: Thursday Rally Consolidated In Tight Ranges

- Treasuries are mildly lower on the day in what have been tight ranges, with the largest moves at the very long end but not troubling recent steeps for 5s30s.

- A federal appeals court yesterday temporarily reinstated the most sweeping tariffs whilst the WSJ reports that the Trump administration is looking at finding a new legal authority to impose tariffs.

- Today sees a press conference between President Trump and Musk at 0830ET. Trump yesterday: “I am having a Press Conference tomorrow at 1:30 P.M. EST, with Elon Musk, at the Oval Office. This will be his last day, but not really, because he will, always, be with us, helping all the way. Elon is terrific!”

- There are also notable data releases including April PCE, MNI Chicago PMI for May and the final U.Mich consumer survey for May, the latter after a tentative improvement was indicated in the preliminary survey that closed shortly after the US-China trade de-escalation on May 12.

- With month-end at play, we can't rule out a late bid in Tsys, they should more broadly have a limited impact. Bloomberg Bonds for Tsys +0.11yr (decent), MS Bonds to Tsys +0.08yr (average).

- Cash yields are 0-1.5bp higher, led by 30s.

- TYU5 sits at 110-22 (unch) in narrow ranges (110-18 to 110-25) on modest cumulative volumes of 290k.

- Whilst a broad consolidation of yesterday’s intraday risk-off and dovish data-driven rally, the earlier high has seen a probe of a key resistance at 110-23 (May 16 high). A clear break would undermine the broader bearish theme and could open 111-05+ (May 9 high).

- Data: PCE Apr (0830ET), Advance goods trade Apr (0830ET), Wholesale/retail inventories Apr/Apr prelim (0830ET), MNI Chicago PMI (0945ET), U.Mich May final (1000ET)

- Fedspeak: Daly panel (1645ET), Goolsbee on radio podcast (time unknown)

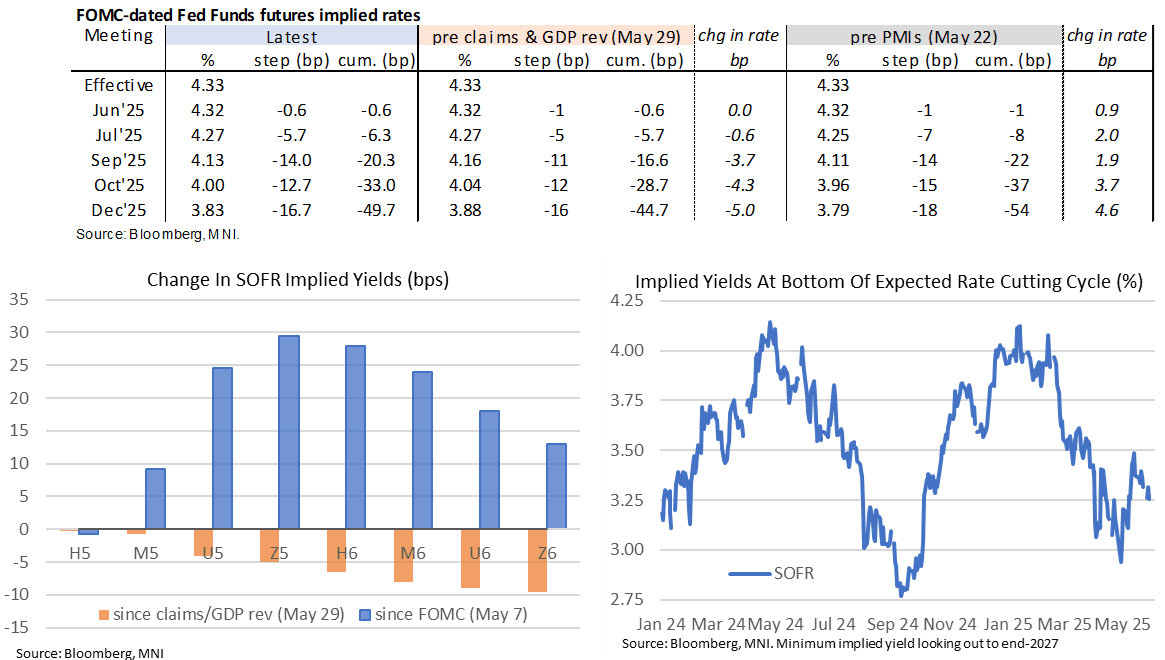

STIR: Fed Rates A Little Off Yesterday’s Most Dovish Levels

- Fed Funds implied rates hold much of yesterday’s dovish shift, seen on a rolling over in equity futures plus a collection of dovish US data, ahead of the April PCE report and finalized U.Mich survey plus further Trump comments.

- The path is slightly off yesterday’s most dovish levels though, with a federal appeals court temporarily reinstating tariffs and the Trump administration looking at alternative strategies.

- Most dovish levels had been seen after White House Press Sec Leavitt said President Trump told Fed Chair Powell he believes the Fed is making a “mistake” by not lowering rates in a Trump-requested meeting. “The president's been very vocal about that, both publicly and now I can reveal privately as well."

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 20.5bp Sep, 33bp Oct and 49.5bp Dec.

- Essentially no change in terminal pricing, with a SOFR implied yields expected to bottom at 3.255% (SFRZ6, -0.5bp). That sits a little below the 100bp +/-5bp of cuts range mostly held in the past two plus weeks.

- SF Fed's Daly (non-voter) speaks late on at 1645ET in a panel (Q&A only). She said yesterday that she's seeing the balance in the labor market that we need for 2% inflation. The economy is in a good place and she sees a general sense of cautious optimism.

STIR: Mix Of Net Long Setting & Short Cover In SOFR Futures On Thursday

OI data suggests that net long setting dominated in the whites and reds as SOFR futures rallied on Thursday.

- Positioning swings then seemed to be a little more split between net long setting and short cover further out the strip.

| 29-May-25 | 28-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,066,123 | 1,064,876 | +1,247 | Whites | +16,187 |

SFRM5 | 1,479,489 | 1,472,677 | +6,812 | Reds | +39,805 |

SFRU5 | 1,124,355 | 1,109,932 | +14,423 | Greens | -5,541 |

SFRZ5 | 1,069,080 | 1,075,375 | -6,295 | Blues | +2,278 |

SFRH6 | 772,877 | 764,540 | +8,337 |

|

|

SFRM6 | 755,303 | 730,600 | +24,703 |

|

|

SFRU6 | 706,891 | 705,185 | +1,706 |

|

|

SFRZ6 | 842,545 | 837,486 | +5,059 |

|

|

SFRH7 | 662,925 | 671,538 | -8,613 |

|

|

SFRM7 | 591,868 | 592,371 | -503 |

|

|

SFRU7 | 419,137 | 425,967 | -6,830 |

|

|

SFRZ7 | 418,199 | 407,794 | +10,405 |

|

|

SFRH8 | 286,665 | 284,618 | +2,047 |

|

|

SFRM8 | 212,592 | 203,772 | +8,820 |

|

|

SFRU8 | 162,800 | 162,276 | +524 |

|

|

SFRZ8 | 178,651 | 187,764 | -9,113 |

|

|

SOUTH KOREA: MNI Publishes Election Briefing

Download Full Report Here

South Korea holds a snap presidential election on Tuesday, 3 June, two years ahead of schedule. The election takes place at a time of heightened political, security, and economic tensions for South Korea, with two strongly opposing views of the country’s future offered by the main candidates. Under the presidency of Yoon Suk-yeol, South Korea moved to significantly bolster relations with the US and Japan as a bulwark against China in the region. The outcome of this election could see a moderation in this stance should the defeated 2022 candidate Lee Jae-myung win, or an acceleration under foreign policy hawk Kim Moon-soo.

In this briefing, we offer scenario analysis of the most likely election outcomes, with assigned probabilities. The briefing also contains a short explanation on how South Korean presidential elections work and how the course of the election should progress on election night, information on the main candidates contesting the vote, and an opinion polling and betting market chartpack.

HONG KONG: Forward Discount Trimmed Sharply as HKD Approaches Weak-Side of Band

Noting a decent intraday move across HKD forward points, with the 12m fwd discount trimmed to 1050 points in a ~200 point move across the European morning, although the move is evident across the curve so far.

- No specific headlines or newsflow to trigger the move, but the rally in curve comes as USD/HKD spot approaches the weak-side of the trading band (7.85) for the first time since the sharp liquidity injection and intervention from HKMA earlier this month after the test on the strong-side.

- The moves may be the first signal that the liquidity injection is starting to be well-absorbed by the market, and keeps focus on HIBOR developments as well as cash demand and corporate activity in Hong Kong.

- We noted earlier this week the switch of venue for the Shein IPO from London to Hong Kong. A successful float could double the the already-strong YTD fundraising on the exchange (running at just under $10bln). With a placement seen as likely later this year (although subject to regulatory approval), focus may shift to potential distortions in HKD cash demand: Sizeable demand for securities can help narrow the HKD forward discount, which has proved sensitive in recent years to a pick-up in capital markets activity, as the uptick in cash demand in turns adds upward pressure to HIBOR.

- Morgan Stanley wrote on HIBOR this week that a test of 7.85, local dividend payments, an increase in issuance or additional IPOs could trigger a rebound in local rates.

EUROPE ISSUANCE UPDATE

BTP Italia

- The institutional takeup of the new 7-year 1.85% Jun-32 BTP Italia was E8.79bln (E9.92bln at the previous offering) according to Reuters.

- In total between institutional and retail E15.31bln was raised.

- The annual real coupon was set this morning at 1.85% with retail investors who hold to maturity to also receive a bonus of 1.0%.

- The retail phase of the placement took place Tue-Thu (ISIN IT0005648248) and saw a takeup of E6.52bln (E8.56bln at the previous offering).

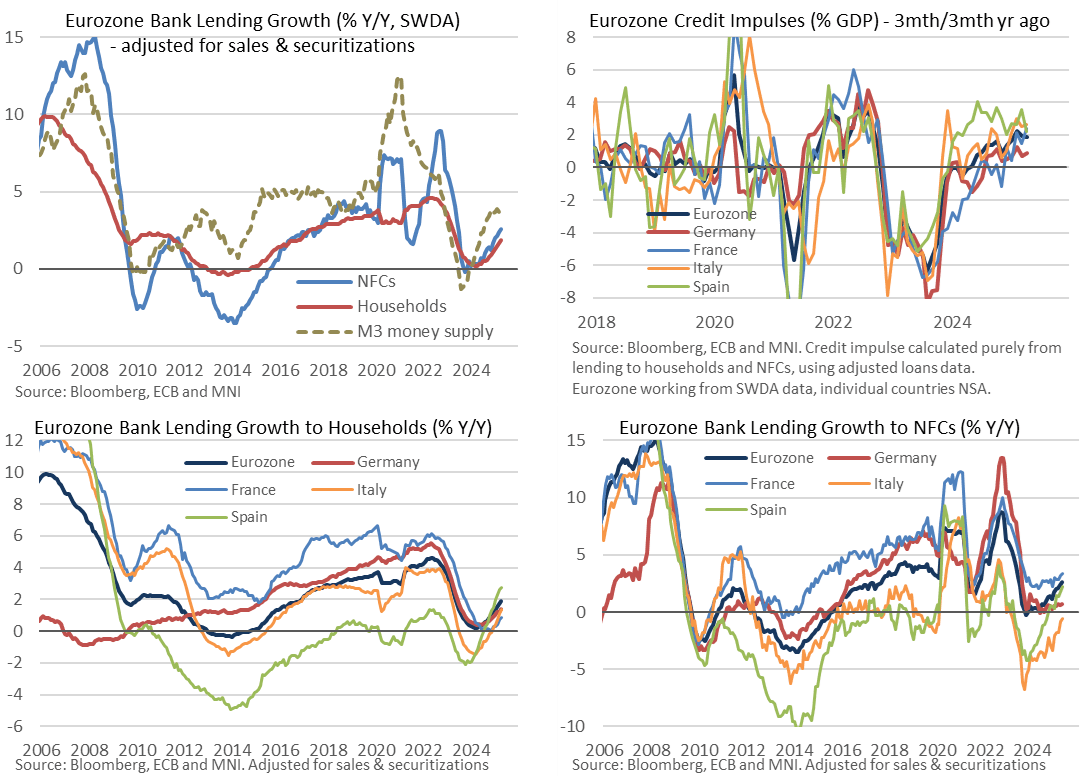

EUROZONE DATA: Lending Growth Accelerates Again, Impulse Maintained

Eurozone lending growth to the private sector accelerated a touch further in April, setting fresh highs since mid-2023 at 2.7% Y/Y or 2.2% Y/Y when adjusting for sales & securitization. Germany continues to lag in credit impulse metrics, not helping by a continuation of what has been a particularly tepid trend in lending to non-financial corporates.

- Sticking to a sales & securitization adjusted basis, lending to non-financial corporates (NFCs) increased 2.6% Y/Y in April after an upward revised 2.4% (initial 2.3) for a fresh high since Jun 2023.

- Lending to households meanwhile increased 1.9% Y/Y in April after 1.7% for its fastest since May 2023. It’s an eight consecutive monthly acceleration for the Y/Y.

- France continues to see the fastest rate of lending to NFCs (3.4% Y/Y, +0.2pp) although Spain and Italy have extended their recovery, with Spain still accelerating strongly (2.3% Y/Y, +0.5pp) and Italy almost out of contraction territory (-0.6% Y/Y, +0.3pp). Germany, however, extends a lacklustre trend, at 0.7% Y/Y (+0.1pp) having averaged 0.6% since late 2023.

- Spain continues to lead the increase in lending to households in what has been an impressive turnaround (2.7% Y/Y, +0.1pp). Germany (1.4% Y/Y, +0.2pp) and Italy (1.4% Y/Y, +0.3pp) follow with France (0.8% Y/Y, +0.1pp) lagging in contrast to its more robust rate of lending to corporates.

- Despite the modest acceleration in credit growth, the Eurozone credit impulse metric of 3mth flows vs 3mths a year ago continued a broad plateauing so far in 2025. It sits around 2% GDP after a large swing from the -5 to -6% GDP seen in mid-2023 when credit growth started to slow abruptly - see top right chart.

- On this relative impulse basis, Italy leads (2.6% GDP), followed by France (2.4% GDP), Spain (2.2% GDP) and Germany lagging (0.9% GDP).

- Separately, Eurozone M3 money supply surprisingly re-accelerated back to 3.9% Y/Y (cons 3.7) in April after an upward revised 3.7% (initial 3.6%) in March and 3.9% in Feb. It averaged 5.0% Y/Y through 2019.

EUROPEAN INFLATION: MNI Projects 2.0-2.1% Y/Y German National CPI, Core 2.8%

From state-level data that equates to 89.1% weighting of the national May flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) printed around 0.0-0.1% M/M and rose 2.0-2.1% Y/Y (April 2.1%). See the tables below for full calculations.

- Analyst consensus stands at 2.1% Y/Y and 0.1% M/M, so there might be some slight downside risks to headline inflation. We had initially seen some marginal upside risks, but since then Rhineland-Palatinate, Berlin and Saarland data all came in softer than the 2.1% Y/Y consensus figure. Either way, the magnitude of risks vs consensus appears contained this month.

- Current tracking of Core CPI (ex-energy and food, based on 50% of the national index) implies around 2.8% (2.9% in April) and 0.1-0.2% M/M.

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is normally the same.

| Y/Y | May (Reported) | April (Reported) | Difference |

| North Rhine Westphalia | 2.0 | 1.8 | 0.2 |

| Hesse | 2.3 | 2.3 | 0.0 |

| Bavaria | 2.1 | 2.1 | 0.0 |

| Brandenburg | 2.2 | 2.2 | 0.0 |

| Baden Wuert. | 2.2 | 2.4 | -0.2 |

| Berlin | 1.8 | 1.9 | -0.1 |

| Saxony | 2.3 | 2.4 | -0.1 |

| Rhineland-Palatinate | 1.7 | 1.9 | -0.2 |

| Lower Saxony | 2.3 | 2.2 | 0.1 |

| Saarland | 1.8 | 1.9 | -0.1 |

| Saxony-Anhalt | 2.8 | 2.9 | -0.1 |

| Weighted average: | 2.05% | for | 89.1% |

| M/M | May (Reported) | April (Reported) | Difference |

| North Rhine Westphalia | 0.2 | 0.4 | -0.2 |

| Hesse | 0.0 | 0.5 | -0.5 |

| Bavaria | 0.1 | 0.4 | -0.3 |

| Brandenburg | 0.0 | 0.4 | -0.4 |

| Baden Wuert. | -0.1 | 0.5 | -0.6 |

| Berlin | -0.1 | 0.3 | -0.4 |

| Saxony | 0.0 | 0.5 | -0.5 |

| Rhineland-Palatinate | -0.1 | 0.4 | -0.5 |

| Lower Saxony | 0.1 | 0.3 | -0.2 |

| Saarland | -0.1 | 0.4 | -0.5 |

| Saxony-Anhalt | 0.0 | 0.5 | -0.5 |

| Weighted average: | 0.04% | for | 89.1% |

BOE: Taylor delivers dovish FT interview but nothing surprising given May vote

- External MPC member Professor Alan Taylor has given an interview with the FT (published around 2 hours ago) in which he notes his dissent in May (voting for a 50bp cut against the 25bp delivered) and that he is seeing increasing risks of the BOE's downside scenario. This shouldn't be too market moving as nothing he has said he is a surprise for him, but it reinforces his position as the second most dovish MPC member (after Dhingra). He also noted that the increase in inflation recently was "driven by one-off factors" and noted that the BOE had forecast inflation to peak later this year, but he was looking further ahead than that. He said that higher inflation is "coming out of one-time tax and administered price changes" and in contrast to Pill's concern on the labour market that pay settlement indicators were “within touching distance of sustainable wage growth.”

- When asked if he would vote for a June cut: “I’m not going to pre-emptively announce my vote, but I think I indicated in my dissent that I thought we needed to be on a lower [monetary] policy path... I’m seeing more risk piling up on the downside scenario because of global developments” with the FT citing that he then pointed to US tariff impacts "be building up over the rest of this year in terms of trade diversion and drag on growth."

- He also said that “We got a massive change in trade policy, we have a lot of uncertainty: I would focus on that as the big story” to first order.

- The full interview is available here (behind paywall).

FOREX: Greenback Retraces Small Part of Thurs Weakness

- The greenback is retracing a small part of the acute weakness posted on Thursday, dragging EUR/USD off the overnight high of 1.1390. Newsflow and headlines have been few and far between, with the temporary reinstatement of Trump's tariff regime containing uncertainty through the appeals process and putting markets on a steadier footing into the final session of the week.

- JPY is firmer against all others. USD/JPY has traded either side of the Y144.00 handle, with markets conscious of the printing of a shooting star candle on the daily chart Thursday. This could signal a bearish short-term reversal for the pair, highlighting the Y142.12 level as key on the downside. A break below here would resume the bear trend posted off the May high, and the March/January highs further out.

- The EUR is more mixed. Having outperformed on tariff uncertainty yesterday (most notably against GBP), the single currency has faded slightly, but the case for EUR as a haven currency through trade volatility remains in place. Equity futures in the US are modestly lower, but well within range of the Thursday close, leaving today's run of data as the key input.

- The German national CPI print is up next, with MNI projecting 2.0-2.1% for the Y/Y rate after this morning's mixed regional inflation prints. Canadian Q1 GDP is also due, seen slowing to 1.7% from 2.6% prior, while US PCE price index data, the final University of Michigan print and the MNI Chicago PMI are set for release.

EQUITIES: Recent Pullback for Eurostoxx 50 Futures Appears Corrective

- The trend cycle in Eurostoxx 50 futures is unchanged, it remains bullish and the recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. A break of this level would strengthen a bull theme. Key support to watch lies at 5249.44, the 50-day EMA. Clearance of this average would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact. Thursday’s initial gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5742.22, the 50-day EMA. A clear break of this average is required to highlight a reversal.

COMMODITIES: Medium-Term Trend Signals for Gold Remain Bullish

- WTI futures traded to a fresh short-term cycle high on May 21 before finding resistance. A bear threat remains intact and the recovery since Apr 9, appears corrective. Key resistance to watch is $62.54, the 50-day EMA. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger.

- A bullish theme in Gold remains intact and recent gains signal the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 30/05/2025 | 1200/1400 | *** | HICP (p) | |

| 30/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/05/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 30/05/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 30/05/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 30/05/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/05/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 30/05/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 30/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 30/05/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 2045/1645 | San Francisco Fed's Mary Daly | ||

| 30/05/2025 | 2330/1930 | Chicago Fed's Austan Goolsbee | ||

| 31/05/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/05/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI |