EUROZONE DATA: Lending Growth Accelerates Again, Impulse Maintained

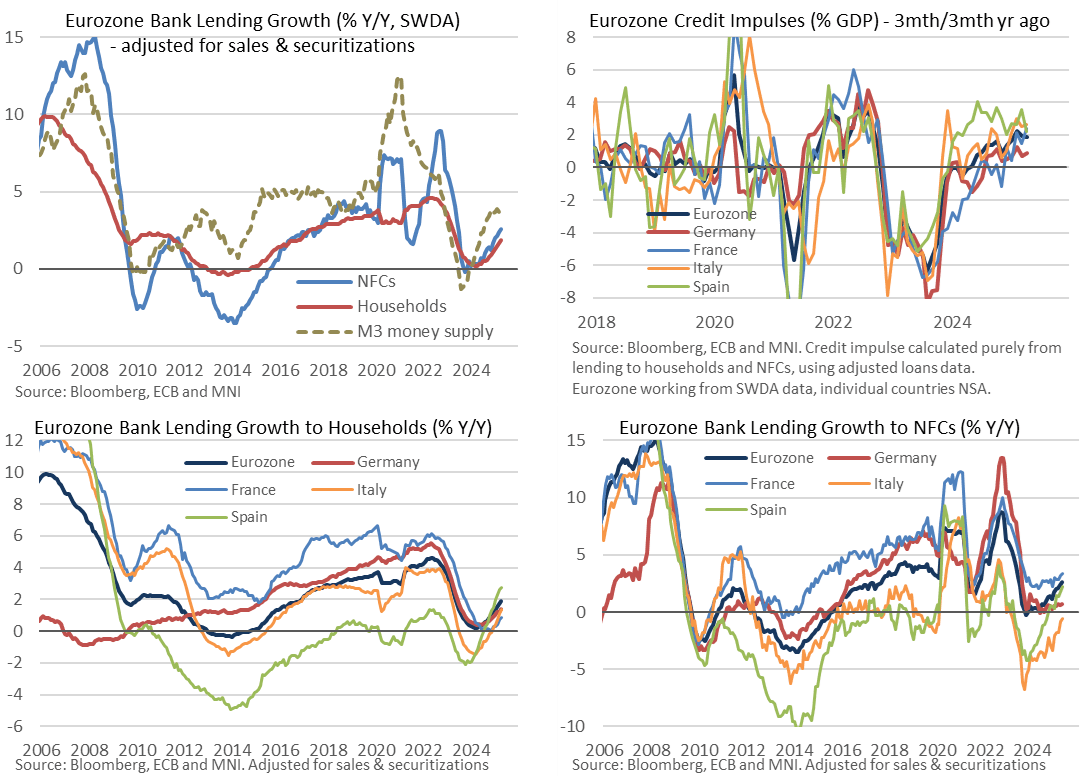

Eurozone lending growth to the private sector accelerated a touch further in April, setting fresh highs since mid-2023 at 2.7% Y/Y or 2.2% Y/Y when adjusting for sales & securitization. Germany continues to lag in credit impulse metrics, not helping by a continuation of what has been a particularly tepid trend in lending to non-financial corporates.

- Sticking to a sales & securitization adjusted basis, lending to non-financial corporates (NFCs) increased 2.6% Y/Y in April after an upward revised 2.4% (initial 2.3) for a fresh high since Jun 2023.

- Lending to households meanwhile increased 1.9% Y/Y in April after 1.7% for its fastest since May 2023. It’s an eight consecutive monthly acceleration for the Y/Y.

- France continues to see the fastest rate of lending to NFCs (3.4% Y/Y, +0.2pp) although Spain and Italy have extended their recovery, with Spain still accelerating strongly (2.3% Y/Y, +0.5pp) and Italy almost out of contraction territory (-0.6% Y/Y, +0.3pp). Germany, however, extends a lacklustre trend, at 0.7% Y/Y (+0.1pp) having averaged 0.6% since late 2023.

- Spain continues to lead the increase in lending to households in what has been an impressive turnaround (2.7% Y/Y, +0.1pp). Germany (1.4% Y/Y, +0.2pp) and Italy (1.4% Y/Y, +0.3pp) follow with France (0.8% Y/Y, +0.1pp) lagging in contrast to its more robust rate of lending to corporates.

- Despite the modest acceleration in credit growth, the Eurozone credit impulse metric of 3mth flows vs 3mths a year ago continued a broad plateauing so far in 2025. It sits around 2% GDP after a large swing from the -5 to -6% GDP seen in mid-2023 when credit growth started to slow abruptly - see top right chart.

- On this relative impulse basis, Italy leads (2.6% GDP), followed by France (2.4% GDP), Spain (2.2% GDP) and Germany lagging (0.9% GDP).

- Separately, Eurozone M3 money supply surprisingly re-accelerated back to 3.9% Y/Y (cons 3.7) in April after an upward revised 3.7% (initial 3.6%) in March and 3.9% in Feb. It averaged 5.0% Y/Y through 2019.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Estoxx Risk Reversal

SX5E (19th June) 4500/5600RR, sold the put at 23.5 in 3k.

SONIA: Large downside Put Spread

Large Downside Sonia put spread multiple clips:

- SFIZ5 95.75/95.65ps, bought for 1 in 22k total.

EGBS: Goldman Look For EGB Outperformance Vs. Peers

Goldman Sachs think the EGBs can outperform wider core rates, based on “the resilience of the asset class in the face of recent volatility, the likely dovish ECB response to the growth damage from U.S. tariffs and the possibility of global risk relief in the event of trade de-escalation”.

- They suggest that “this cyclical environment does not preclude a renewed focus on fiscal or political risk, especially in core countries. But we think those risks are likely to become more meaningful only later in the year, when French budget negotiations are in full swing, and we move closer to the inflection in German issuance”.

- Goldman note that “given the significant market focus on diversification away from U.S. assets, the prospect for global portfolio flows into EGBs is worth considering. We argue that the larger economies of Southern Europe (Italy & Spain) are best placed to benefit from inflows, as foreign ownership in those markets still lags the improvements in macro fundamentals or that in the hedge value of government bonds”.

- They continue “to forecast 10y BTP-Bund, OAT-Bund, and Bonos-Bund at 120bp, 70bp, and 60bp respectively at year-end”. However, they see “risks tilted towards tighter spreads into the summer”.