MNI US MARKETS ANALYSIS - Treasuries Erase IJC Rally

Highlights:

- Treasuries erase jobs-led rally, curve flatter on yesterday's 30y auction

- Equities fade off alltime highs, but no major backtrack yet

- Takaichi takes top spot in LDP polling, hindering JPY

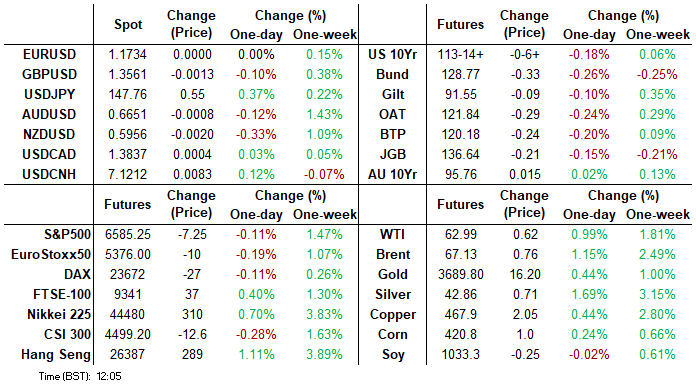

US TSYS: 5s30s Flattening Extends, More Than 20bps Off Last Week’s Cycle Highs

- Treasuries are for the most part mildly lower on the day albeit with some outperformance for 30s after yesterday’s auction (on the screws but with higher bid-to-cover (2.38 vs 2.27) and indirect take-up (62.0% vs 59.5%).

- USTs outperform EGBs but latter in the weakness could be some catch-up following yesterday’s UST sell-off that continues late in the session.

- The US front-end to belly has now broadly reversed yesterday’s rally on high initial jobless claims and the broader CPI report although the longer end still has further to go.

- Today see focus on a Trump interview at 0800ET before the U.Mich consumer survey is the sole release of the day at 1000ET.

- Cash yields are 1.3bp higher (7s) to 0.1bp lower (30s).

- 30s outperformance extend the week’s flattening in 5s30s, currently at 104.7bps (-1.3bp on the day) having started the week at 118bp and briefly peaked at ~127bps for fresh multi-year highs after last Friday’s payrolls report.

- TYZ5 trades at 113-15 (-07) on another overnight session with thin cumulative volumes currently at 220k.

- An earlier low of 113-11+ saw it fully reverse yesterday’s data-driven rally although it’s back a little higher. Yesterday’s spike leaves a fresh resistance level at 113-29 with bulls still in the driver’s seat, whilst support is seen at 113-05+ (Sep 10 low).

- Data: U.Mich consumer survey Sep prelim (1000ET)

- Politics: Trump in live TV interview with Fox and Friends (0800ET)

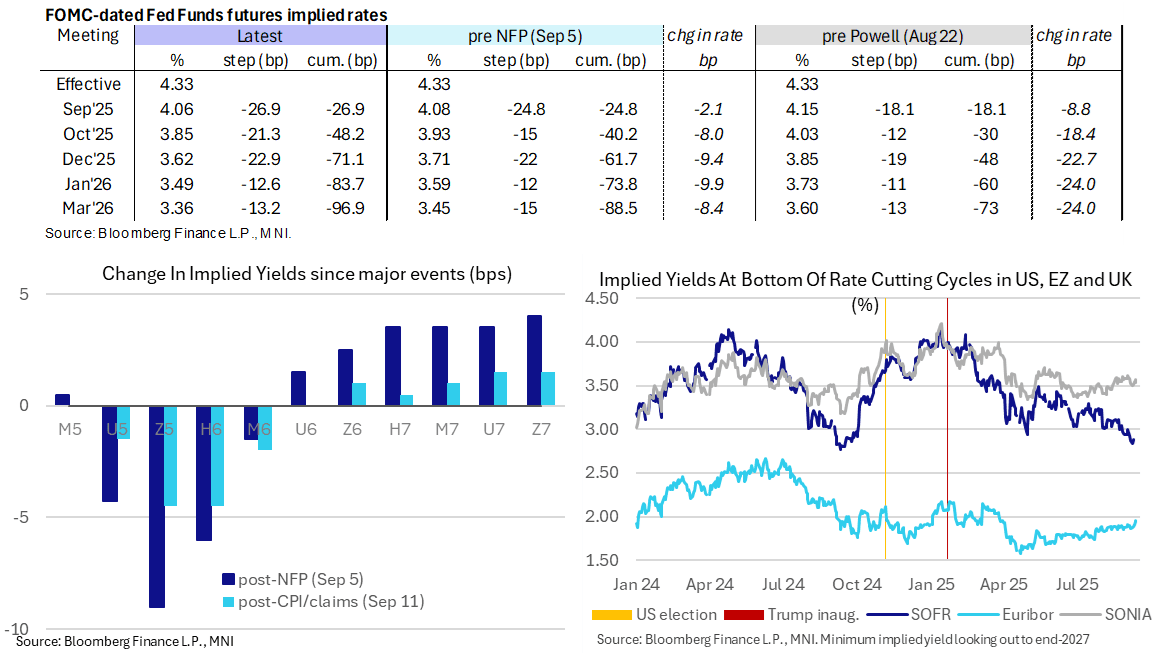

STIR: Rally On Jobless Claims and CPI Pared To Differing Degrees

- Fed Funds implied rates are up to 1bp higher on the day for meetings out to early 2026, still holding about half of yesterday’s decline on higher jobless claims (with somewhat of a caveat from a spike in Texas) and the CPI report.

- Cumulative cuts from 4.33% effective: 27bp Sep, 48bp Oct, 71bp Dec, 84bp Jan and 97bp Mar.

- Further out the curve, SOFR futures are up to 3.5 ticks lower in late 2027 contracts to more than fully reverse the rally seen on yesterday’s data - bottom left chart.

- The SOFR implied terminal yield of 2.92% (SFRH7) is 2.5bp higher on the day, at what would be its highest close since payrolls but still pointing to ~140bp of cuts ahead.

There will be uncertainty for the composition of the FOMC at next week's decision right up to the wire:

- The Justice Dept yesterday asked a three-judge panel in Washington to grant a stay order that most likely would allow Trump’s firing of Cook to take effect before the president’s appeal is formally heard. The administration asked for a ruling by Monday."

- Senate Majority Leader Thune filed cloture yesterday on CEA’s Miran to be a member of the Fed Board until Jan 31, 2026. It indicates Miran is on track to be confirmed in time for the Tue-Wed FOMC meeting, with a final vote on the Senate floor likely on Monday evening (having passed 13-11 in the Senate Banking Committee).

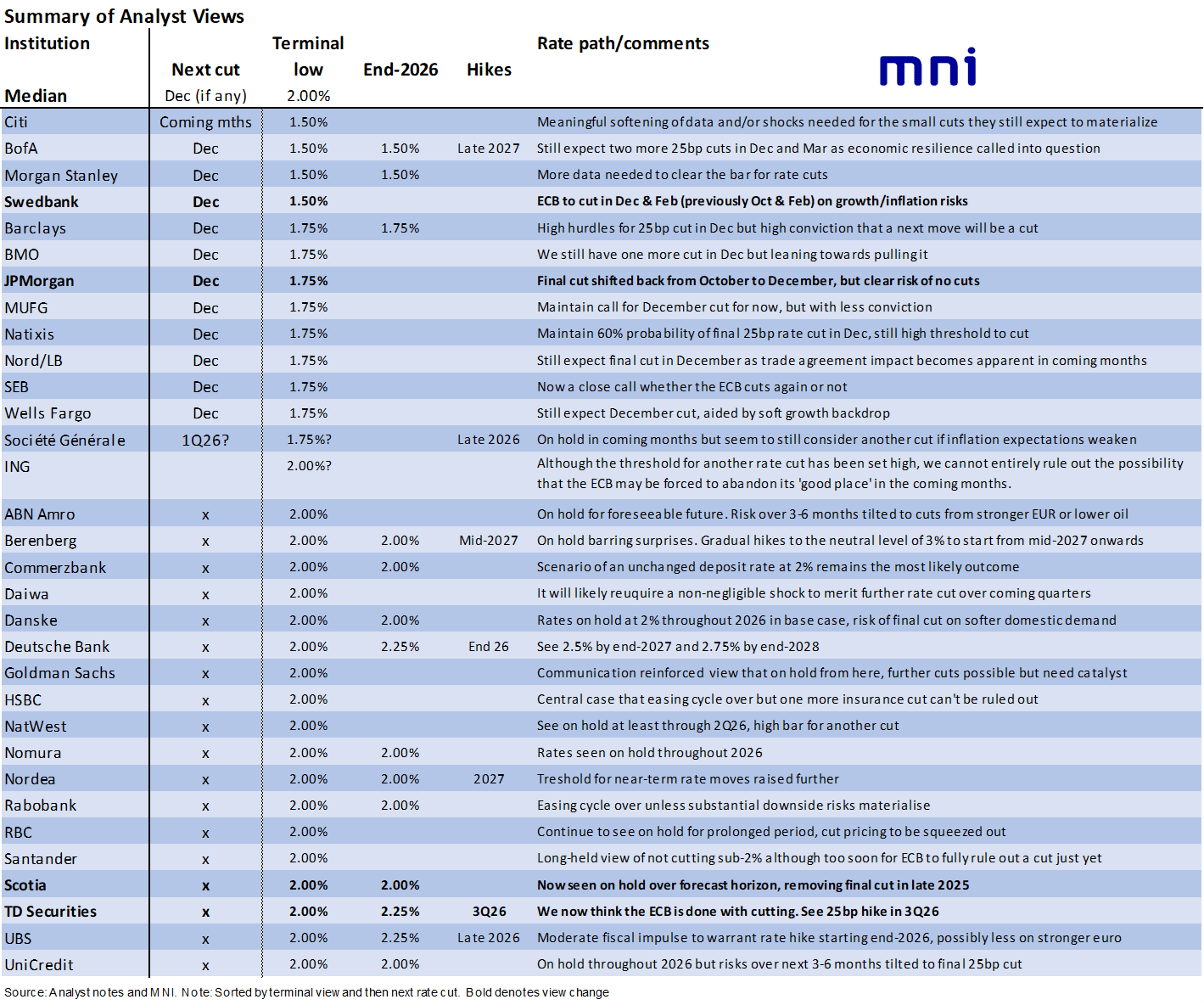

ECB: Analyst Post-ECB Rate View Summary: Hawkish Tilt

Of the 32 analysts reviewed since yesterday's ECB decision, we still see a median terminal deposit rate of 2%. It comes with 19 looking for no further rate cuts, 9 looking for one cut and 4 looking for two cuts. ECB-dated OIS currently only has ~10bp of cuts priced to mid-2026.

We have seen four view changes, all in a hawkish direction but from analysts at either end of the hawk-dove spectrum.

- Scotia and TD Securities have removed their view for a final cut, with Scotia seeing the ECB on hold for the forecast horizon whilst TD envisages the start of hikes in 3Q26.

- That leaves TD with the earliest starting point we’ve seen for hikes where explicitly stated by analysts.

- Swedbank meanwhile still see two cuts ahead but have pushed back the next cut from October to December.

- JPMorgan have also pushed back the next cut from October to December, still seen as the final cut for the cycle.

- A few analysts looking for rates on hold for the foreseeable future specifically note a 3-6 month window where downside risks to policy rates are more pronounced.

US TSY FUTURES: Net Long Setting In TY Futures Dominated On Thursda

OI data points to a mix of net long setting (TU, TY & US), long cover (FV) and short cover (UXY & WN) on Thursday

- Although the curve-wide net DV01 swing was tiled towards net long setting, that was solely down to TY futures, which saw over $5mln of fresh DV01 risk added.

| 11-Sep-25 | 10-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,491,488 | 4,483,696 | +7,792 | +316,292 |

FV | 6,839,914 | 6,841,762 | -1,848 | -82,259 |

TY | 5,368,865 | 5,288,243 | +80,622 | +5,531,899 |

UXY | 2,370,477 | 2,373,674 | -3,197 | -292,791 |

US | 1,819,081 | 1,815,828 | +3,253 | +467,224 |

WN | 2,016,635 | 2,026,485 | -9,850 | -1,866,488 |

|

| Total | +76,772 | +4,073,878 |

SOFR: Fresh Positions Set In Most Futures On Thursday

OI data points to a mix of net long setting (SFRU5-M6) and short setting dominating across much of the SOFR futures strip on Thursday, with only limited rounds of net long cover (SFRH8, M8 & Z8) interrupting.

| 11-Sep-25 | 10-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,225,497 | 1,204,565 | +20,932 | Whites | +90,895 |

SFRU5 | 1,481,267 | 1,429,563 | +51,704 | Reds | +75,221 |

SFRZ5 | 1,674,810 | 1,659,998 | +14,812 | Greens | +33,131 |

SFRH6 | 1,204,080 | 1,200,633 | +3,447 | Blues | +14,951 |

SFRM6 | 1,023,413 | 996,018 | +27,395 |

|

|

SFRU6 | 889,548 | 877,762 | +11,786 |

|

|

SFRZ6 | 1,032,430 | 1,008,063 | +24,367 |

|

|

SFRH7 | 716,009 | 704,336 | +11,673 |

|

|

SFRM7 | 849,672 | 840,020 | +9,652 |

|

|

SFRU7 | 690,095 | 682,414 | +7,681 |

|

|

SFRZ7 | 686,073 | 669,270 | +16,803 |

|

|

SFRH8 | 446,239 | 447,244 | -1,005 |

|

|

SFRM8 | 357,384 | 359,017 | -1,633 |

|

|

SFRU8 | 273,387 | 257,747 | +15,640 |

|

|

SFRZ8 | 260,820 | 261,554 | -734 |

|

|

SFRH9 | 186,335 | 184,657 | +1,678 |

|

|

SECURITY: Kremlin Says Negotiations With Ukraine Have Been 'Paused'

Kremlin spokesperson Dmitri Peskov told reporters, “There's a pause in Russia-Ukraine negotiations.” Peskov added Russia “remains open to talks,” but European countries are “holding back efforts to find peace in Ukraine,” per Reuters.

- The comments come amid European efforts to fortify NATO's Eastern flank in response to a Russian drone incursion into Poland that resulted in NATO engaging Russian aircraft in NATO airspace for the first time.

- Peskov dismissed European concerns over the joint Russian-Belarusian ‘Zapad’ military exercises, which got underway today, as “emotions based on hostility towards Russia.” This week's Zapad - wargaming conflict with NATO - is the first major military exercise on NATO’s border since the invasion of Ukraine.

- ECFR writes Europe should treat Zapad as political theatre, "a staged escalation to ratchet up the security climate ... and influence talks between Moscow, Minsk and Washington.”

- European capitals await President Trump’s decision on Russian sanctions. Yesterday, Trump reiterated he is “not happy” but a comment suggesting Russia’s drone incursion “could have been a mistake,” raised European concerns over Trump's commitment to NATO security and prompted a drop in the implied probability of new sanctions on Russia.

- Politico notes the Trump administration "has its eye elsewhere", citing a new National Defense Strategy that "places domestic and regional missions above countering adversaries."

- NATO Secretary General Mark Rutte and NATO's Supreme Allied Commander Alexus Grynkewich will deliver a joint press conference at 11:00 ET 16:00 BST 17:00 CET.

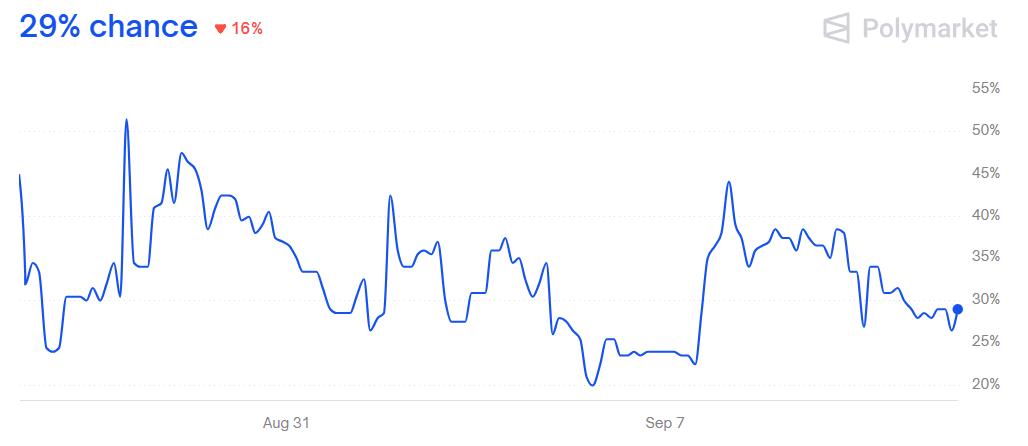

Figure 1: New US Sanctions On Russia by Sept. 30

Source: Polymarket

FOREX: JPY Softer as Takaichi Takes Top Spot in Polling

- JPY weakness stands out early Friday, with USD/JPY rallying through Y147.50 on the back of a Kyodo News report flagging that Thatcherite MP Takaichi is leading opinion polling to replace Ishiba as leader of the LDP and Japanese Prime Minister. Her pro-fiscal spending stance as well as her criticism of BoJ tightening plans have worked against the currency and any rally through yesterday's highs opens resistance into 148.58/149.14, the Sep 8/3 highs.

- The USD trades firmer against all others in G10, benefiting from a phase of equity sales alongside the European open. Weakness in stocks came on no headline or news trigger, although losses are just off yesterday's alltime highs - so may mimic profit-taking rather than any fundamental driver. The USD Index daily chart shows this rally is still contained below 97.944, the 50% retracement for the downleg posted off the early September highs.

- FX volumes are healthy: Z5 EUR futures have posted close to 30k contracts, while JPY futures are seeing notable interest: and already aren't far off meeting the cumulative total volume from Thursday.

- The single currency continues to trade well: the EUR holds yesterday's rally as markets see the first post-decision comments from governing council members. The trend theme in EURUSD remains bullish and the pair is trading closer to its recent highs. Resistance at 1.1743, the Aug 22 high, has recently been cleared reinforcing a bull cycle. This signals scope for 1.1829, the Jul 01 high and bull trigger.

- Focus for the duration of Friday trade shifts to prelim University of Michigan sentiment numbers, at which markets expect 1-year and 5-10-year inflation expectations to moderate to 4.8% and 3.4% respectively. The Fed remain inside their pre-meeting media blackout period, which should keep central bank speak quiet.

OPTIONS: Expiries for Sep12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.7bln), $1.1600(E1.1bln), $1.1650(E1.6bln), $1.1670-75(E1.8bln), $1.1700(E2.8bln), $1.1724-35(E1.9bln) $1.1800(E1.5bln), $1.1850(E1.4bln)

- USD/JPY: Y146.00($1.1bln), Y147.25($616mln), Y147.40-50($2.9bln), Y150.00($698mln), Y151.00($1.1bln)

- EUR/GBP: Gbp0.8725(E604mln)

- AUD/USD: $0.6570-90(A$1.6bln)

EQUITIES: Post-CPI Gains Reinforce Bullish Theme for E-Mini S&P

- A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5369.48, the 50-day EMA. A clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, the contract has recovered above the 20-day EMA - a bullish development for now. A stronger reversal would open 5445.00, Aug 26 high.

- A bull cycle in S&P E-Minis remains intact and Thursday’s gains reinforce current conditions. The contract has once again traded to a fresh cycle high. This confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6600.00 handle where a break would strengthen the bull theme and open 6673.37, a Fibonacci projection. Initial support to watch is 6481.60, the 20-day EMA.

COMMODITIES: Gold Remains in a Clear Bull Cycle, Close to Fresh Record Highs

- The trend condition in WTI futures is unchanged - a bear cycle remains intact and recent short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would open $57.71, the May 30 low.

- Gold remains in a clear bull cycle and continues to trade at its recent highs. The yellow metal has traded to a fresh all-time high again this week. The break higher confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3504.1, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 12/09/2025 | 1230/0830 | * | Building Permits | |

| 12/09/2025 | 1400/1000 | * | Services Revenues | |

| 12/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 12/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 12/09/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 12/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |