OPTIONS: Expiries for Sep12 NY cut 1000ET (Source DTCC)

Sep-12 10:38

- EUR/USD: $1.1550(E1.7bln), $1.1600(E1.1bln), $1.1650(E1.6bln), $1.1670-75(E1.8bln), $1.1700(E2.8bln), $1.1724-35(E1.9bln) $1.1800(E1.5bln), $1.1850(E1.4bln)

- USD/JPY: Y146.00($1.1bln), Y147.25($616mln), Y147.40-50($2.9bln), Y150.00($698mln), Y151.00($1.1bln)

- EUR/GBP: Gbp0.8725(E604mln)

- AUD/USD: $0.6570-90(A$1.6bln)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

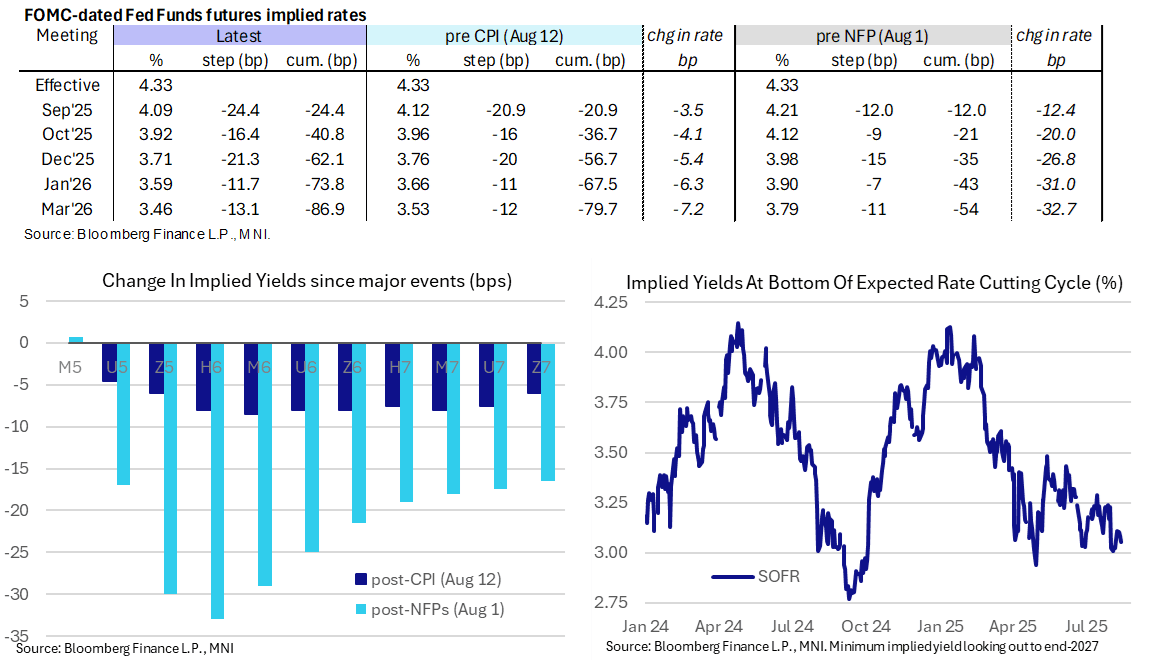

STIR: Fed Rate Path Split Between Two and Three Cuts For 2025

Aug-13 10:37

- Fed Funds implied rates are unchanged on the day for the September meeting after yesterday’s CPI report (25bp cut essentially fully priced) but are up to 2.5bp lower out to 1Q26 amidst a broader FI rally.

- Cumulative cuts from 4.33% effective: 24.5bp Sep, 41bp Oct, 62bp Dec, 74bp Jan and 87bp Mar.

- The 62bp for the year compares with 56.5bp pre-CPI and 35 pre-NFP. The now outdated June SEP median had 50bp of cuts with seven members looking for no cuts at all.

- The SOFR implied yield of 3.055% (SFRH7) is 3bp lower on the day, back to fully pricing five cuts for the cycle.

- Bessent late yesterday suggested the Fed ought to be open to a 50bp rate cut next month. The Fed “could have been cutting in June, July” had it had the revised [payrolls] figures in hand at the time. He said the CPI report showcased that economists had misread the likely effect of tariffs.

- Analysts continue to shift towards market pricing for the September FOMC, with Nomura and TD Securities yesterday joining a sizeable list of those now looking for a 25bp cut next month.

- Today's scheduled Fedspeak sees Goolsbee and Bostic in focus:

- 0800ET - Barkin (non-voter) repeats a speech on the economy. Subsequent Q&A might be watched but unlikely to say anything new - he said yesterday the "balance" between dual mandate variables is "still unclear".

- 1300ET - Goolsbee ('25 voter, dove) speaks at a monetary policy luncheon. It's been an unusually long time since Goolsbee last spoke, on Jul 11 saying that he has seen "surprisingly little" impact from tariffs but that new tariff threats (at the time) could delay rate cuts.

- 1330ET - Bostic (non-voter) speaks on the economic outlook (Q&A only). This should be a useful update from Bostic, who said after the July nonfarm payrolls report that he still saw only one rate cut this year. He wants to see how things evolve over the coming months and warned that it might take twelve months for businesses to adjust their prices.

EQUITY OPTIONS: Commerzbank longer dated Put Options

Aug-13 10:25

- CBK (18/12/26) vs (17/12/27) 32p, trades for the 2027 2.14 in 9.5k.

There are no OI in those strikes, new Positions.

GBP: GBP/USD Set to Test Key Resistance

Aug-13 10:23

Latest stretch higher in GBP is putting GBP/USD on course for a test of the major resistance we've flagged at 1.3589: clearance here puts prices at the highest since mid-July fully reverses the fade into the early August lows.

- GBP has been the primary beneficiary of the USD-led weakness in recent weakness - with the contrast between BoE and Fed policy cemented on the hawkish BoE cut last week, limiting the pricing of UK rate cuts into year-end, and through to the Autumn Budget - the next major macro event in the medium-term (likely late October/early November).

- Growth numbers due tomorrow are expected to show a sharp slowing in quarterly growth to 0.1% from 0.7% in the prior quarter - but an upside surprise here would catalyse a move north of the current range and extend the spell of not-as-bad-as-feared UK economic data.

- The downtick in front-end implied GBP vols coincides with improving net risk reversals - likely implying a cheapening of put vol that covers both the Sept and Nov MPC, priced for a cumulative 11bps of cuts across both meetings.

- On GBP, Rabobank write that they see GBP's recent better tone running out of steam, with the BoE cutting in November - with this week's growth data possibly confirming stagflationary fears.