ECB: Analyst Post-ECB Rate View Summary: Hawkish Tilt

Sep-12 10:09

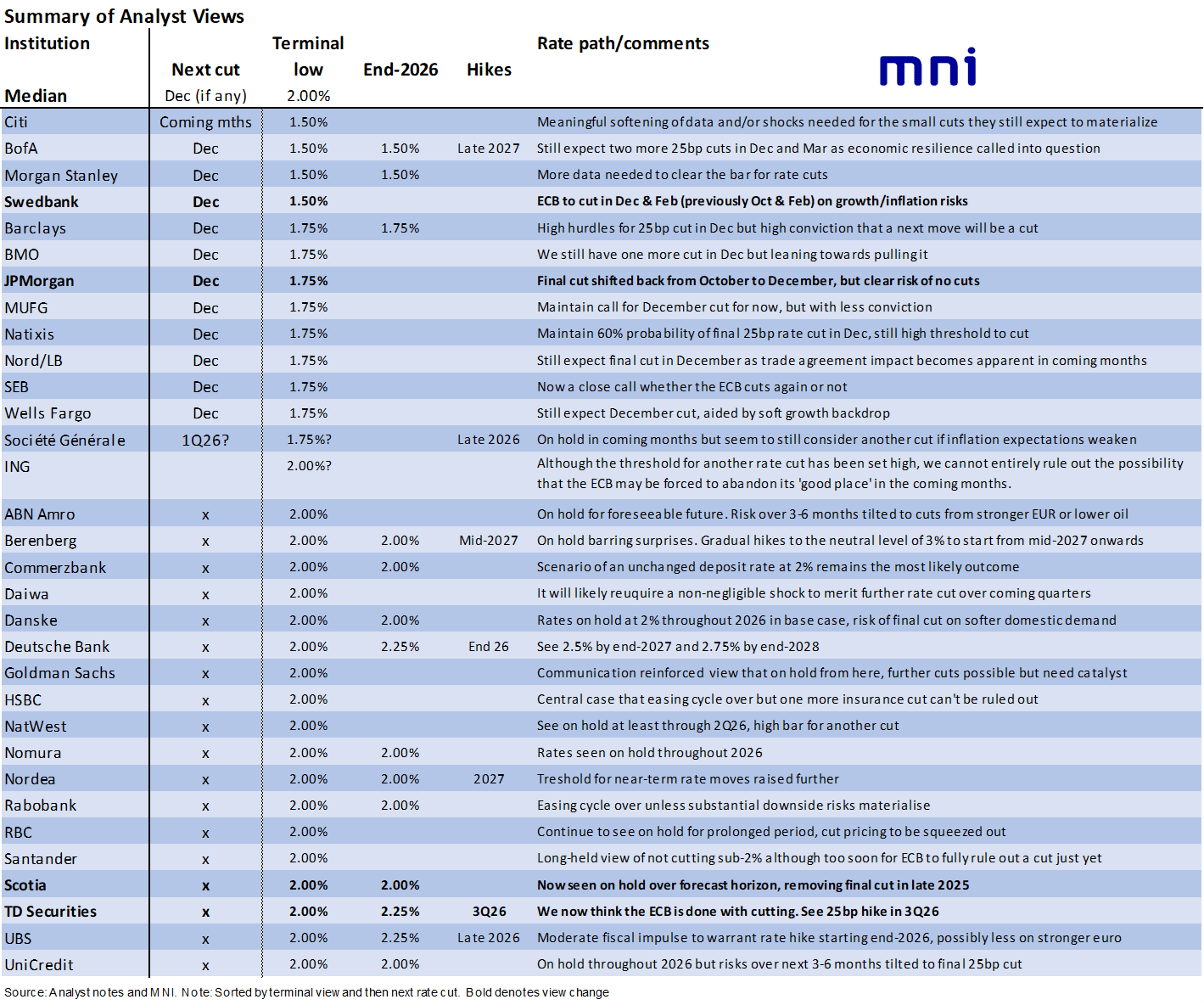

Of the 32 analysts reviewed since yesterday's ECB decision, we still see a median terminal deposit rate of 2%. It comes with 19 looking for no further rate cuts, 9 looking for one cut and 4 looking for two cuts. ECB-dated OIS currently only has ~10bp of cuts priced to mid-2026.

We have seen four view changes, all in a hawkish direction but from analysts at either end of the hawk-dove spectrum.

- Scotia and TD Securities have removed their view for a final cut, with Scotia seeing the ECB on hold for the forecast horizon whilst TD envisages the start of hikes in 3Q26.

- That leaves TD with the earliest starting point we’ve seen for hikes where explicitly stated by analysts.

- Swedbank meanwhile still see two cuts ahead but have pushed back the next cut from October to December.

- JPMorgan have also pushed back the next cut from October to December, still seen as the final cut for the cycle.

- A few analysts looking for rates on hold for the foreseeable future specifically note a 3-6 month window where downside risks to policy rates are more pronounced.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED FUNDS FUTURES: FFV5/X5 Spread Sold

Aug-13 10:00

FFV5/X5 ~2.9K given at -15.5.

US OUTLOOK/OPINION: Core PCE Estimates Ease To 0.25% M/M For July

Aug-13 09:56

- Yesterday’s CPI report has seen core PCE estimates for July center on 0.25% M/M (across eight analysts) vs a tentative 0.31% M/M prior to CPI (across five analysts).

- It implies a very similar pace to the 0.26% M/M in latest data for June and would see the Y/Y firm to 2.87% for its fastest since February.

- There’s a relatively narrow range of 0.22-0.28% considering PPI is still to come tomorrow.

- Wells Fargo: 0.22%

- JPM: 0.24%

- Nomura: 0.24% (vs 0.33 pre-CPI)

- NWM: 0.24%

- TDS: 0.25%

- UBS: 0.25% (vs 0.33 pre-CPI)

- GS: 0.26% (vs 0.31 pre-CPI)

- BofA: 0.28%

RIKSBANK: VIEW: Handelsbanken No Longer Expect August Cut

Aug-13 09:54

- “Our call for a Riksbank August rate cut has been challenged by high summer inflation prints. We believe this outweighs concerns over weak economic activity, leading us to expect the Riksbank to hold rates in August”.

- “Although some economic indicators have come in weaker than expected, this is unlikely to prompt immediate policy action in the current inflation environment. At its August meeting, the board also lacks updated staff forecasts, which may be needed to assess the outlook with enough confidence to look past the current inflation overshoot”.

- “A full report also offers additional scope to explain the rationale for a rate cut even as inflation remains elevated. Lastly, with the markets pricing a low probability – less than 10 percent – of an August rate cut, a pause could be in line with monetary policy and contribute to stability in turbulent times”.

- “We forecast that the Riksbank will deliver another rate cut in September to support economic activity and guard against inflation falling too far going forward”.

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank

Schatz

Bobl