STIR: Rally On Jobless Claims and CPI Pared To Differing Degrees

Sep-12 10:34

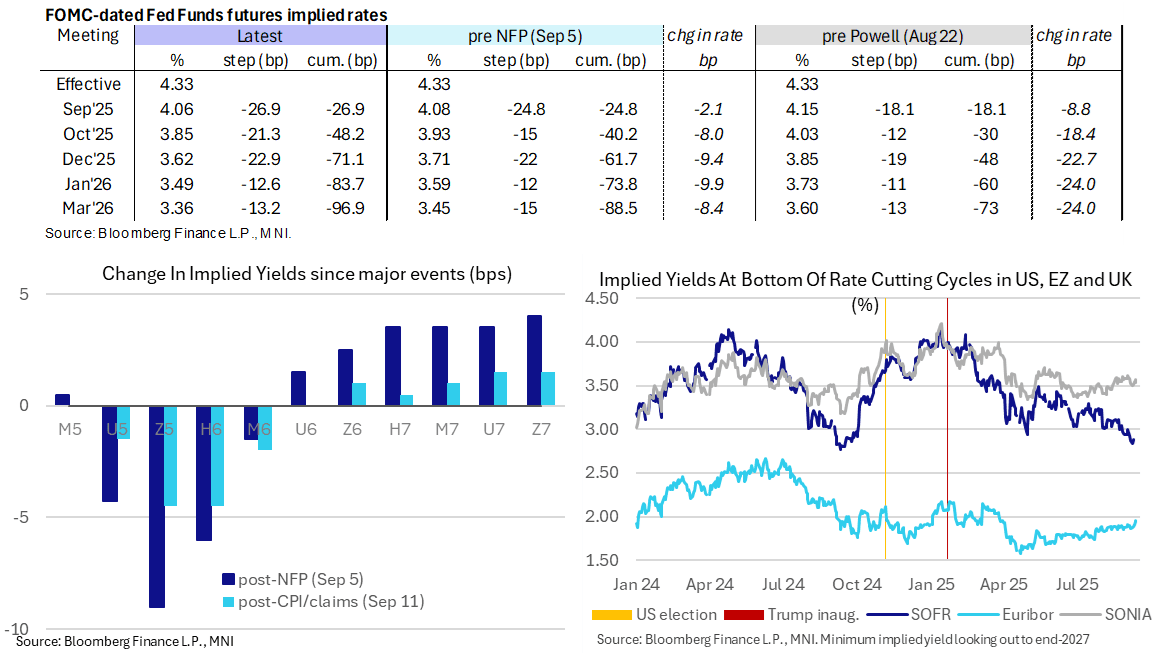

- Fed Funds implied rates are up to 1bp higher on the day for meetings out to early 2026, still holding about half of yesterday’s decline on higher jobless claims (with somewhat of a caveat from a spike in Texas) and the CPI report.

- Cumulative cuts from 4.33% effective: 27bp Sep, 48bp Oct, 71bp Dec, 84bp Jan and 97bp Mar.

- Further out the curve, SOFR futures are up to 3.5 ticks lower in late 2027 contracts to more than fully reverse the rally seen on yesterday’s data - bottom left chart.

- The SOFR implied terminal yield of 2.92% (SFRH7) is 2.5bp higher on the day, at what would be its highest close since payrolls but still pointing to ~140bp of cuts ahead.

There will be uncertainty for the composition of the FOMC at next week's decision right up to the wire:

- The Justice Dept yesterday asked a three-judge panel in Washington to grant a stay order that most likely would allow Trump’s firing of Cook to take effect before the president’s appeal is formally heard. The administration asked for a ruling by Monday."

- Senate Majority Leader Thune filed cloture yesterday on CEA’s Miran to be a member of the Fed Board until Jan 31, 2026. It indicates Miran is on track to be confirmed in time for the Tue-Wed FOMC meeting, with a final vote on the Senate floor likely on Monday evening (having passed 13-11 in the Senate Banking Committee).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY OPTIONS: Commerzbank longer dated Put Options

Aug-13 10:25

- CBK (18/12/26) vs (17/12/27) 32p, trades for the 2027 2.14 in 9.5k.

There are no OI in those strikes, new Positions.

GBP: GBP/USD Set to Test Key Resistance

Aug-13 10:23

Latest stretch higher in GBP is putting GBP/USD on course for a test of the major resistance we've flagged at 1.3589: clearance here puts prices at the highest since mid-July fully reverses the fade into the early August lows.

- GBP has been the primary beneficiary of the USD-led weakness in recent weakness - with the contrast between BoE and Fed policy cemented on the hawkish BoE cut last week, limiting the pricing of UK rate cuts into year-end, and through to the Autumn Budget - the next major macro event in the medium-term (likely late October/early November).

- Growth numbers due tomorrow are expected to show a sharp slowing in quarterly growth to 0.1% from 0.7% in the prior quarter - but an upside surprise here would catalyse a move north of the current range and extend the spell of not-as-bad-as-feared UK economic data.

- The downtick in front-end implied GBP vols coincides with improving net risk reversals - likely implying a cheapening of put vol that covers both the Sept and Nov MPC, priced for a cumulative 11bps of cuts across both meetings.

- On GBP, Rabobank write that they see GBP's recent better tone running out of steam, with the BoE cutting in November - with this week's growth data possibly confirming stagflationary fears.

SOFR OPTIONS: SFRU5 96.00/96.125/96.25 Call Fly Blocked

Aug-13 10:21

Latest block trade lodged at 06:00:30 NY/11:00:30 London

- SFRU5 96.00/96.125/96.25 call fly 4K blocked at 1.0, looks like a buyer vs. 95.955 (10% delta).

Trending Top

Jan-30 21:43

Jan-30 21:11