MNI EUROPEAN OPEN: Trump Ends US-Canada Trade Talks

EXECUTIVE SUMMARY

- TRUMP-XI TO MEET NEXT THURSDAY ON SIDELINES OF APEC SUMMIT - BBG

- TRUMP SAYS ALL TRADE TALKS WITH CANADA ARE TERMINATED - BBG

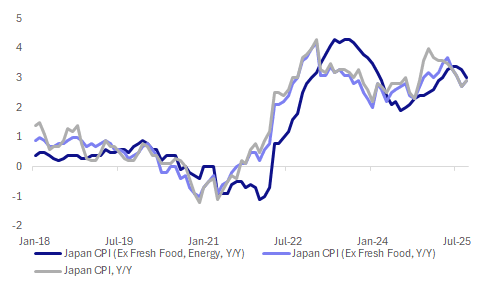

- JAPAN SEPT CORE CPI RISES 2.9% VS. AUG 2.7% - MNI BRIEF

- CHINA- US TRADE RELATIONS NEED DIALOGUE - WANG - MNI BRIEF

- CHINA TO PROMOTE INDUSTRIAL UPGRADE, DOMESTIC MARKETS - MNI BRIEF

Fig 1: Japan CPI Y/Y Trends Converging Near 3% (Services Inflation Slowed)

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

CONSUMER (MNI BRIEF): UK consumer confidence edged higher in October, helped in part by an early round of autumn sales, a leading survey showed.

EU

EU/CHINA (BBG): " French President Emmanuel Macron told European Union leaders to consider using the bloc’s most powerful trade tool against China if they aren’t able to find a resolution to Beijing’s planned export controls on critical raw materials."

UKRAINE (BBG): "The European Union put off until December a decision on whether to tap frozen Russian central bank assets to aid Ukraine, threatening an effort to get Ukraine fresh funding by early 2026."

US

US/CHINA (BBG): “US President Donald Trump and Chinese President Xi Jinping will meet next Thursday on the sidelines of the Asia-Pacific Economic Cooperation summit, the White House announced, as the leaders of the world’s two largest economies look to deescalate a simmering trade war.”

US/CANADA (BBG): "US President Donald Trump said he would immediately halt all trade negotiations with Canada. In a post on Truth Social, Trump criticized an advertisement that he said featured former President Ronald Reagan speaking negatively about tariffs."

HOUSING (MNI): U.S. sales of existing homes increased 1.5% to a seasonally adjusted annual rate of 4.06 million in September, the National Association of Realtors said Thursday, meeting expectations and the fastest annualized pace since February. Sales year-over-year are up 4.1%.

TECH (BBG): "The Trump administration is pushing regulators to dramatically accelerate the process of allowing the booming data-center sector to connect to power grids."

OTHER

JAPAN (MNI BRIEF): Japan’s core consumer inflation accelerated to 2.9% y/y in September from August’s 2.7%, in line with market estimates, as higher energy prices offset a slowdown in food prices excluding perishables, data released Friday by the Ministry of Internal Affairs and Communications showed.

JAPAN (BBG): "Japan’s Finance Minister Satsuki Katayama signaled that it may be necessary to issue additional debt to fund Prime Minister Sanae Takaichi’s upcoming economic package, if existing resources prove insufficient."

ASIA (RTRS): "The International Monetary Fund on Friday urged Asia to lower non-tariff barriers and integrate regional trade to reduce its vulnerability to U.S. tariffs and global financial shocks."

CHINA

US/CHINA (MNI BRIEF): Dialogue and communication remains the correct choice for China and the U.S. to handle trade relations, Minister of Commerce Wang Wentao told reporters on Friday in Beijing.

ECONOMY (MNI BRIEF): China will focus on building a modern industrial system and a strong domestic market over the next five years, aiming to significantly boost residents’ consumption rate and enhance self-reliance in science and technology during its 15th Five-Year Plan period.

ECONOMY (BBG): “ China needs a bolder spending package to mend the finances of households and companies, according to a central bank adviser, as signs of resilience in the economy mask the damage wrought by the trade war with the US.”

YUAN (SHANGHAI SECURITIES NEWS): “The internationalization of China’s currency is gaining significant momentum, suggesting a “new window of opportunity“ has opened for Beijing’s long-term goal of increasing the yuan’s global usage amid a trend toward a more multi-polar international monetary system, the Shanghai Securities News says.”

OIL (BBG): "Chinese state-owned companies including Sinopec canceled some purchases of seaborne Russian crude after the US blacklisted Rosneft PJSC and Lukoil PJSC, adding to signs of disruption in the oil market."

MNI: PBOC Net Injects CNY3.2 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY168 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY3.2 billion after offsetting maturities of CNY164.8 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4019% at 09:40 am local time from the close of 1.4267% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Thursday, compared with the close of 50 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.0928 Fri; -0.09% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0928 on Friday, compared with 7.0918 set on Thursday. The fixing was estimated at 7.1221 by Bloomberg survey today.

MARKET DATA

AUSTRALIA OCT P S&P PMI MFG 49.7; PRIOR 51.4

AUSTRALIA OCT P S&P PMI SERVICES 53.1; PRIOR 52.4

AUSTRALIA OCT P S&P PMI COMPOSITE 52.6; PRIOR 52.4

JAPAN SEP NATL CPI Y/Y 2.9%; MEDIAN 2.9%; PRIOR 2.7%

JAPAN SEP NATL CPI, EX FRESH FOOD Y/Y 2.9%; MEDIAN 2.9%; PRIOR 2.7%

JAPAN SEP NATL CPI, EX FRESH FOOD, ENERGY Y/Y 3.0%; MEDIAN 3.1%; PRIOR 3.3%

JAPAN OCT P S&P PMI MFG 48.3; PRIOR 48.5

JAPAN OCT P S&P PMI SERVICES 52.4; PRIOR 53.2

JAPAN OCT P S&P PMI COMPOSITE 50.9; PRIOR 51.3

MARKETS

US TSYS: USTs Steady in Asia, Await Key CPI Tonight

US Bond futures finished marginally up in a low volume trading day in Asia. The 10-Yr TYZ5 is up 01 at 113-14+, virtually flat on the week. A mid week rally on what appeared growth concerns (given US lockdown) saw a peak in TYZ5 of 113-25+ which was eroded overnight as oil rallied.

Cash has had a mini rally in the afternoon with most maturities lower by -0.5 - 1.0bps.

- The US 2-Yr is down at 3.48%, yet remains higher by +3bps for the week.

- The US 5-Yr is at 3.60% but +1bp for the week, holding to the 3.55% - 3.65% range for now.

- The US 10-Yr closed briefly back above 4.00% but has edged below again in the Asia trading day to be 3.99%, -2bps for the week.

- The 30-Yr is flat today at 4.58% but remains the best performer for the week, down -2bps.

The bond rally in mid-week posed risks for bond traders ahead of tonight's CPI should the release be higher than expected. The move higher in yields overnight given Oil's gains sees those risks moderating, though could suggest the market could be skewed to lower yields and likely to overreact to higher inflation. The forecast for CPI YoY is +3.1% (from +2.9% August) and MoM flat at +0.4%. September release was originally due mid month but was delayed due to the government shut down. The FED meets next week on October 30 with a strong consensus building among investors for another cut. Even a moderately stronger than expected inflation print could see investors views challenged.

JGBS: Flatter Curve Trend Continues, Despite Possible Fresh JGB Issuance

JGB futures have drifted a little higher post the lunchtime break, last 136.12, +.02 versus settlement levels. As has been the case recently, dips under 136.00 have been supported. Further fresh sharp downside in US Tsy futures has been absent, with some support likely coming from lower oil prices. JGB futures have also taken in their stride comments from the new FinMin, who did not rule out further JGB issuance to fund the upcoming economic assistance package.

- There were a host of comments from new FinMin Satsuki Katayama earlier. On extra JGB issuance via BBG: "“We usually draw from higher-than-expected tax revenues and unspent funds from previous budgets to fund extra budgets,” Katayama said in an interview with a group of reporters Friday. “But if that’s not enough, we’ll have to issue more government bonds — it can’t be helped if it comes to that,” she said."

- Still, there were also references to fiscal prudence, with the FinMin stating that the cabinet has not abandoned the government's target of achieving a budget surplus.

- On the BoJ the FinMin said that central bank and the government need to be in unison on basic policy objectives and given that the central bank maintains an accommodative stance she doesn't need to talk further about the matter.

- JGB back end yields are looking through any fresh issuance concerns and continue to track lower, the 20-40yr tenors down a further 2.5bps. The 30yr (last just under 3.07%) is challenging 100-day EMA support in yield terms. The 2/30s curve remains in a flattening trend, last +213bps (-2bps). The 10yr outright yield is down slightly to 1.655%.

- Earlier data showed Sep nationwide CPI close to forecasts, headline and core ex fresh food ticking up to 2.9%y/y, while the measure which excludes fresh food and energy eased to 3.0%y/y from 3.3%. Services y/y inflation eased to 1.4% (from 1.5%) reinforcing a likely wait and see approach from the BOJ next week (decision Thursday the 30th of Oct).

AUSSIE BONDS: 10yr Futures 95.90 High Intact, Q3 CPI/RBA Fireside Chat Next Week

Aussie bond futures hold weaker, but away from session lows. 10yr (XM were last 95.845, -2bps (session lows were at 95.815), while 3yr (YM) are off by 1.5bps to 96.62 (session lows at 96.585). This fits with broader regional/US trends, where further downside in futures has proven limited so far. A softer tone to oil prices (albeit only off 0.60%), along with proximity to the US CPI print later, are likely drivers of market sentiment. Important support for Aussie futures (96.28 for 3yr and 95.51 (Sep 3 low) remain some distance away.

- Any fresh upside in US Tsy futures, could bring resistance at 95.90 into focus for the Aussie 10yr.

- AU-US 10yr government bond yield differentials remain off recent highs, last +15bps.

- Outright ACGB yields are are round 1-2bps firmer, with the back end outperforming in yield terms. The 3yr was last around 3.365%, while the 10yr is just under 4.14%.

- Earlier RBA Governor Bullock spoke on the payments system, with the monetary policy outlook not covered. We had Oct preliminary PMIs out earlier too, with manufacturing slumping to 49.7 from 51.4, although this is not a tier one release.

- Of greater focus will be on next week's Q3 CPI print due Wednesday. Headline is expected to rebound to 3.0% y/y (from 2.1%), but trimmed mean is expected to hold steady at 2.7%y/y.

- Before this, Monday evening 7:15PM AEDT we have Bullock giving a Fireside chat at the ABE dinner. Focus will obviously be on the outlook ahead of the Nov policy meeting, and whether the recent rise in the unemployment rate has shifted the central bank bias/outlook.

BONDS: NZGBS: 10yr Back Offs 4.00% Upside Test, ANZ Surveys In Focus Next Week

NZGB yields are holding higher, but are away from session best levels. The 10yr yield couldn't sustain earlier highs above 4.00% and sits back at 3.985%R in latest dealings. The 2yr has held steady at 2.52% for much of the session. Oil prices have edged lower so far today, while US cash Tsy yields are also down a touch, likely help drag NZGB yields off earlier highs. As we noted earlier NZGB 2 and 10yr yields remain sub all key EMAs, although further upside can't be ruled out in the near term. Focus for today will rest firmly with the US CPI print later. For 10yr the 10yr the 20-day EMA is near 4.08%, for the 2yr around 2.62%.

- The NZ 2/10s curve is slightly steeper, but at +146bps remains sub recent highs around +154bps. The NZ-US 10yr government bond yield differential is around flat, up from the -3-4bps region, but still struggling for meaningful upside. Our fair estimate, last around +6bps, could shift depending on how tonight's US CPI unfolds.

- Looking ahead to next week, we have jobs filled data out on Tuesday, while ANZ business and activity figures print Thursday, then ANZ consumer confidence is out on Friday. The Q3 jobs data though, due Nov 5 is likely the next major focus point from an RBNZ standpoint (next meeting on 26th of Nov).

FOREX: USD/JPY Eyeing Upside 153 Test, USD/CAD Above 1.4000 On Trump Headlines

The USD BBDXY index remains close to this week's highs, last 1213.90, up around 0.1% so far today. The clear focus later will be on the US CPI print. Yen weakness remains a dominant trend, with the edge up in the USD/CNY fix, coupled with muted comments on FX from Japan government officials, driving an earlier run up towards 153.00 (highs were 152.92). The 153.27 level, the Oct 10 high and bull trigger, isn't too far away. Yen is now off this week by 1.5%, the weakest performer in the G10 space. Elsewhere, USD/CAD has pushed up above 1.4000, as US President Trump stated all trade negotiations with Canada would cease. AUD/USD is back to 0.6500, but NZD is outperforming marginally, holding close to 0.5750. Both currencies remain with recent ranges.

- Earlier remarks from Japan's Economic and Fiscal Policy Minister Minoru Kiuchi suggested little concern around weaker FX trends (at least at face value). He stated that FX rates are determined by various factors, but refrained from broader comments on FX, which appears to reflect less concern around FX weakness than previous ministers under the Ishiba regime (previous FinMin Kato recently stated that it was important that the yen moved stably and in line with fundamentals and that they were seeing rapid FX moves in the weak yen direction).

- Earlier data from Japan showed a slight softening in the services CPI for Sep, which should reinforce the BoJ's wait and see approach at next week's policy meeting (Thursday), while the Oct preliminary Oct PMI fell further into contraction, implying downside risks for IP growth.

- USD/CAD spiked from 1.3990 to highs of 1.4028, but we sit back at 1.4010/15 in latest dealings, as Trump headlines crossed. We were close to 1.3990 before the headlines crossed (we remain above all key EMAs, the 20-day EMA is near 1.3980/85, while recent highs rest at 1.4080). US President Trump posted via Truth Social that all trade negotiations with Canada are now terminated. He stated Canada falsely used an ad featuring former President Ronald Reagan speaking negatively about tariffs.

- Out of the US CPI later, we get the preliminary PMIs for Oct for the UK, EU and US.

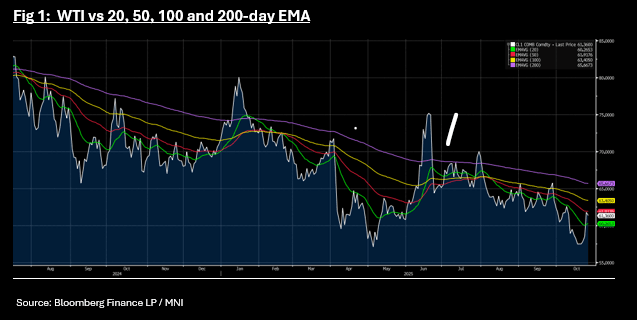

OIL: WTI Bounces on Key Technical, Set for Strongest Week Since June

- Oil gave back some of last night's gains, yet remains set for it's strongest week since June.

- Up over +6.6% for the week, WTI has declined -0.65% to USD$61.39 bbl in the Asia trading day unable to break through the 50-day EMA of $61.91

- Brent is down -0.61% at US$65.59, yet remains up +7% week to date.

- Overnight was oil's biggest one day jump since June, oil gaining on the announcement of US sanctions on Russia's biggest oil companies Rosneft and Lukoil, in efforts to cut off revenue to Russia and limit its ability to continue the war in Ukraine.

- The sanctions come at a time when Ukraine attacks on Russian oil infrastructure has escalated increasing the possibility that global oil supply could be impacted by reduced Russian supply.

- Indian refiners have indicated that the latest sanctions will severely impact their ability to continue to buy Russian oil (as per BBG).

- The EU followed the US with new sanctions including targeting the Russian shadow fleet, a crack down on Russian crypto financing and a ban on LNG imports into Europe from 2027.

- Chinese state-owned companies including Sinopec canceled some purchases of seaborne Russian crude after the US blacklisted Rosneft PJSC and Lukoil PJSC, adding to signs of disruption in the oil market. The Chinese majors have begun to assess the impact of the US curbs, as well as similar moves by the European Union, according to people with knowledge of the situation, asking not to be identified discussing sensitive issues. The companies have paused purchases of some spot cargoes, mostly ESPO, a grade that ships from Russia’s Far East, (as per BBG)

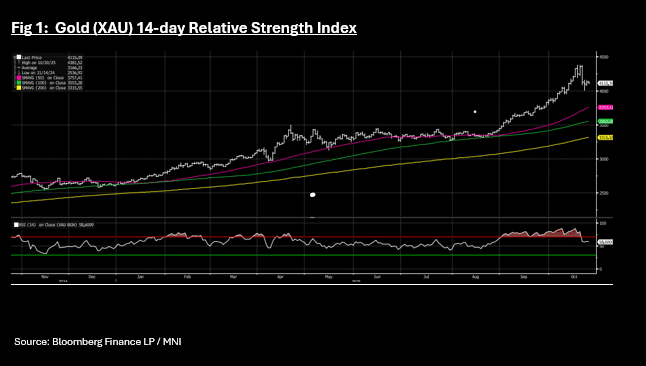

Gold Set for First Weekly Decline Since August

- In a 9-week run of gains, gold has risen almost 25% over that period but falls in recent days could result in its first weekly fall since mid-August.

- The majority of falls this week occurred on Tuesday, with one of the biggest one day falls of the year and bullion has been unable to recover since.

- The catalyst appears profit taking as yet another new record was achieved Monday, closing at US$4,356.30. Year to date gold is up +57%.

- The two days of losses came as ETF outflows reached their highest in several months.

- "The fundamentals supporting gold's rise remain in place, according to the Global Commodities Team at J.P. Morgan. Foreign managers of U.S. assets have diversified from dollars to gold this year, causing demand to rise. If their U.S. exposure drops to 43% from around 45% today, and half a percentage point is redirected to gold, prices could rise to $6,000 per ounce by 2028, the team predicted." as per BBG

- Gold has remained overbought since early September according to the 14-day Relative Strength Index and the move puts bullion back closer to fair value.

- That in itself is likely to see buyers return as the USD diversification story continues and Central Bank buying of gold continues to grow.

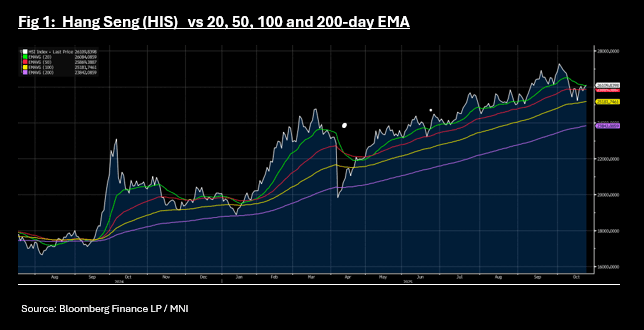

ASIA STOCKS: Strong Week for Region as Tech Leads; HSI Nears Key Technical

China stocks had suffered earlier this week as the Trump administration threatened to curb China's access to key software. As the four day conclave of the Communist Party's Central Committee concluded Thursday, new goals emerged in the next 5-Year plan of China's plan for self-reliance and strength in science and technology. This came as news that a US - China summit has been agreed. Tech stocks in general are strong today with key stocks like Samsung up +2.5% to reach new highs and the Hang Seng Tech Index up over 1%. Major bourses have delivered strong gains this week, with some hitting new all time highs.

- The Jakarta Composite has posted the biggest 5-day gains, up just on 5% in a week where the Central Bank surprised markets by remaining on hold. Since the lows of late March, the JCI is up just on 40% as the Prabowo Government undertakes a pro-growth policy approach.

- The KOSPI's 5-day gains are over 4.5% given the Tech story, and hit yet another new high as the Korea Economic Daily reported that President Lee is considering cutting the top rate on dividends (as per BBG).

- As the political happenings in Japan led to a new leader, the NIKKEI has gained strongly on hopes that inflation fighting packages are to be announced. The NIKKEI closed at new highs Tuesday before profit takers took over. For the week, the NIKKEI remains up over 3% with the Tech sector contributing strongly to gains.

- China's major bourses have all enjoyed solid gains this week as the momentum in the Tech sector globally, drove local prices alongside expectations for the new 5-Year plan. All major bourses are up with the outperformer the Shenzhen Composite, up +3.5%. The HSI in Hong Kong delivered gains of +3.4% for the week and is near the 20-day EMA, attempting to finish above it for the first time in a fortnight.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 24/10/2025 | 0600/0800 | ** | PPI | |

| 24/10/2025 | 0600/0700 | *** | Retail Sales | |

| 24/10/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/10/2025 | 0700/0900 | ** | PPI | |

| 24/10/2025 | 0700/0900 | * | Labour Market Survey | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/10/2025 | 0800/1000 | ECB Cipollone Fireside Chat on International Finance | ||

| 24/10/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/10/2025 | 1200/0800 | ** | Brazil Preliminary CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Services Index (flash) |