US TSYS: USTs Steady in Asia, Await Key CPI Tonight

US Bond futures finished marginally up in a low volume trading day in Asia. The 10-Yr TYZ5 is up 01 at 113-14+, virtually flat on the week. A mid week rally on what appeared growth concerns (given US lockdown) saw a peak in TYZ5 of 113-25+ which was eroded overnight as oil rallied.

Cash has had a mini rally in the afternoon with most maturities lower by -0.5 - 1.0bps.

- The US 2-Yr is down at 3.48%, yet remains higher by +3bps for the week.

- The US 5-Yr is at 3.60% but +1bp for the week, holding to the 3.55% - 3.65% range for now.

- The US 10-Yr closed briefly back above 4.00% but has edged below again in the Asia trading day to be 3.99%, -2bps for the week.

- The 30-Yr is flat today at 4.58% but remains the best performer for the week, down -2bps.

The bond rally in mid-week posed risks for bond traders ahead of tonight's CPI should the release be higher than expected. The move higher in yields overnight given Oil's gains sees those risks moderating, though could suggest the market could be skewed to lower yields and likely to overreact to higher inflation. The forecast for CPI YoY is +3.1% (from +2.9% August) and MoM flat at +0.4%. September release was originally due mid month but was delayed due to the government shut down. The FED meets next week on October 30 with a strong consensus building among investors for another cut. Even a moderately stronger than expected inflation print could see investors views challenged.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Yields End Mixed, 2-Year Edges Lower

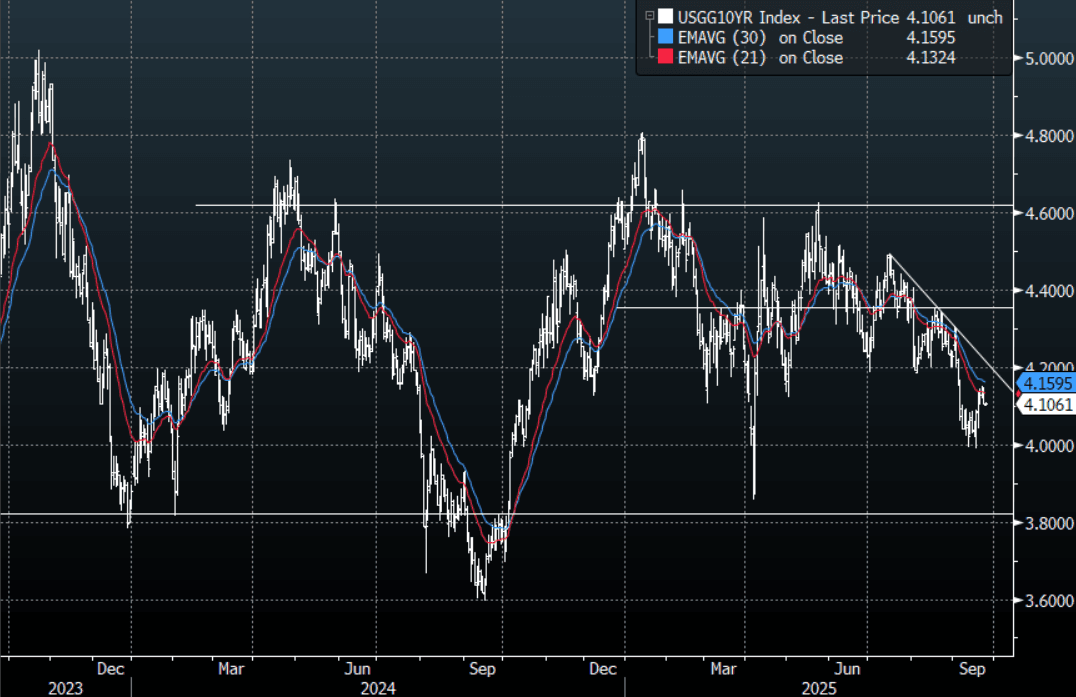

The TYZ5 range has been 112-28 to 112-31 during the Asia-Pacific session. It last changed hands at 112-29+, up 0-01+ from the previous close.

- The US 2-year yield has edged lower trading 3.633%, down 0.02 from its close.

- The US 10-year yield is trading around 4.106%.

- This saw the 2s10s yield curve move higher, +1.68 at 53.481.

- 10-Year’s found some buyers back towards 4.15%. Is that the top, I suspect we test the 4.20% area at some point where demand should again return. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Bloomberg - “The OECD warned that the global economy has yet to feel the full impact of Trump’s tariffs, despite recent resilience. It raised its forecast for growth to 3.2% this year, but expects momentum to moderate to 2.9% in 2026 amid higher import duties.”

- Samantha LaDuc on X: “Apollo’s Torsten Slok on US inflation: “72% of the CPI components are growing faster than the Fed’s 2% inflation target.”

- Robin Brooks on X: “Last week's Fed meeting was a hawkish catalyst for markets. In the run-up to that meeting, markets priced a lot more Fed easing, which pulled down longer-term US and French yields. But now there's no more Fed meeting to anchor long-term yields and they're up again.”

- Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cash Bonds Mostly Slightly Richer At Lunch

At the Tokyo lunch break, JGB futures are stronger, +8 compared to settlement levels, after yesterday's holiday.

- Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August.

- The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although it remains at much higher outright levels (52.0).

- On the services side for Japan, we remain at elevated levels. There remains a decent wedge between the manufacturing and services PMIs.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 1.3bp lower (20-year) to 0.3bp higher (40-year). The benchmark 10-year yield is 0.9bp lower at 1.645% versus the cycle high of 1.670%.

- Swap rates are flat to 2bps lower.

MNI EXCLUSIVE: MNI Discusses BOJ's Must Haves For Further Hikes