JGBS: Flatter Curve Trend Continues, Despite Possible Fresh JGB Issuance

JGB futures have drifted a little higher post the lunchtime break, last 136.12, +.02 versus settlement levels. As has been the case recently, dips under 136.00 have been supported. Further fresh sharp downside in US Tsy futures has been absent, with some support likely coming from lower oil prices. JGB futures have also taken in their stride comments from the new FinMin, who did not rule out further JGB issuance to fund the upcoming economic assistance package.

- There were a host of comments from new FinMin Satsuki Katayama earlier. On extra JGB issuance via BBG: "“We usually draw from higher-than-expected tax revenues and unspent funds from previous budgets to fund extra budgets,” Katayama said in an interview with a group of reporters Friday. “But if that’s not enough, we’ll have to issue more government bonds — it can’t be helped if it comes to that,” she said."

- Still, there were also references to fiscal prudence, with the FinMin stating that the cabinet has not abandoned the government's target of achieving a budget surplus.

- On the BoJ the FinMin said that central bank and the government need to be in unison on basic policy objectives and given that the central bank maintains an accommodative stance she doesn't need to talk further about the matter.

- JGB back end yields are looking through any fresh issuance concerns and continue to track lower, the 20-40yr tenors down a further 2.5bps. The 30yr (last just under 3.07%) is challenging 100-day EMA support in yield terms. The 2/30s curve remains in a flattening trend, last +213bps (-2bps). The 10yr outright yield is down slightly to 1.655%.

- Earlier data showed Sep nationwide CPI close to forecasts, headline and core ex fresh food ticking up to 2.9%y/y, while the measure which excludes fresh food and energy eased to 3.0%y/y from 3.3%. Services y/y inflation eased to 1.4% (from 1.5%) reinforcing a likely wait and see approach from the BOJ next week (decision Thursday the 30th of Oct).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

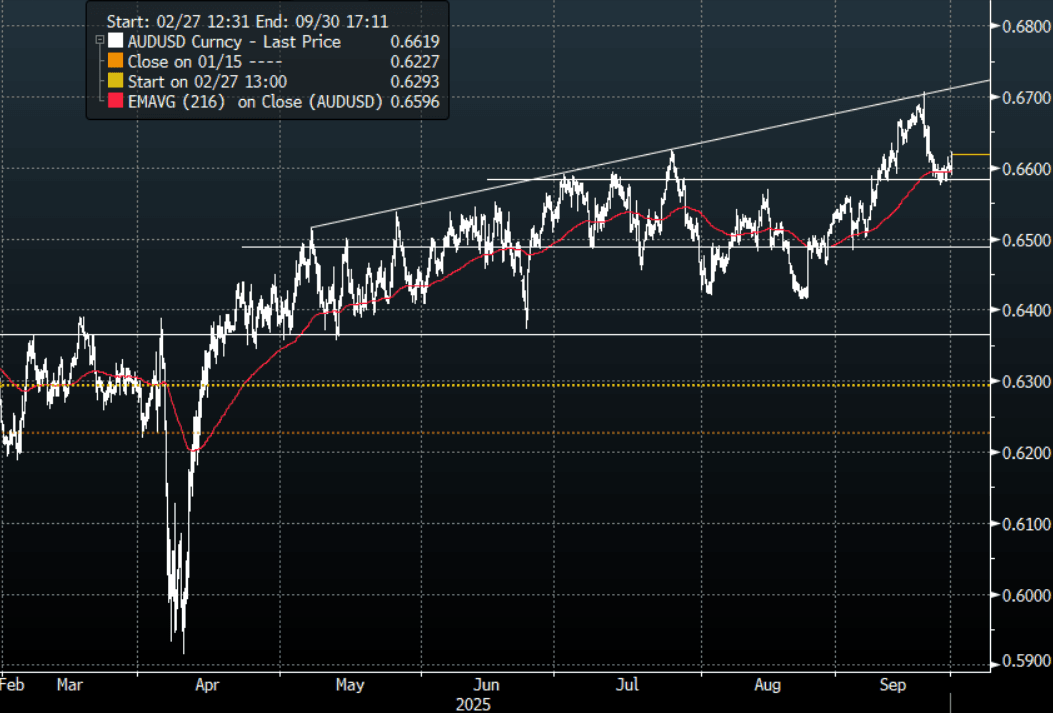

AUD: Asia Wrap - Hotter CPI Print Helps AUD/USD Probe Back Above 0.6600

The AUD/USD has had a range of 0.6589 - 0.6623 in the Asia- Pac session, it is currently trading around 0.6620, +0.32%. The AUD moved higher across the board in reaction to a hotter CPI print. The AUD/USD’s ability to build on this move higher will depend largely on the USD’s fortunes. I suspect the AUD continues to consolidate just above 0.6600 while the USD works out what it wants to do.

- MNI AU - August CPI Headline Up To 3%Y/Y, Trimmed Mean Eases To 2.6%: The headline August CPI print was 3.0%y/y, against a 2.9% market consensus and 2.8% July outcome. The trimmed mean was 2.6% y/y, after printing 2.7% in July (there is no consensus estimate for this outcome).

- Whilst the RBA will continue to place more weight on the quarterly CPI (we get the new comprehensive monthly series towards the end of Nov, for the Oct reference period), today's data will reinforce some caution for the central bank around further easing. It is likely to firm the no change stance next week (although market pricing has priced in very little chance of a move).

- "AUSTRALIA'S CHALMERS: AUSTRALIA LOOKING AT NEW WAYS TO CUT RED TAPE IN TAX SYSTEM" : BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD904m), 0.6625(AUD575m), 0.6720(AUD791m). Upcoming Close Strikes : 0.6625(AUD1.29b Sept 29), 0.6725(AUD1.19bm Sept 29), 0.6730(AUD466m Sept 25) - BBG

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- AUD/JPY - Asia-Pac range 97.28 - 97.95, Asia is trading around 97.95.The pair has found solid demand back towards 97.00 and has bounced with the help of today's CPI print. While above 97.00 focus will turn to September's highs toward 98.50.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

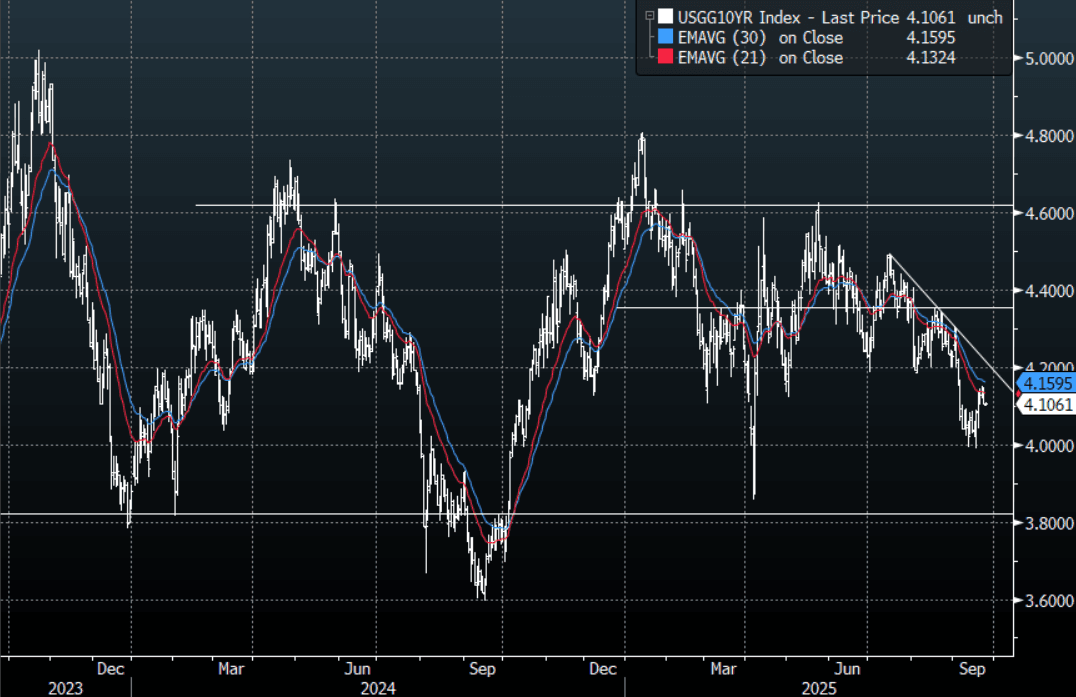

US TSYS: Asia Wrap - Yields End Mixed, 2-Year Edges Lower

The TYZ5 range has been 112-28 to 112-31 during the Asia-Pacific session. It last changed hands at 112-29+, up 0-01+ from the previous close.

- The US 2-year yield has edged lower trading 3.633%, down 0.02 from its close.

- The US 10-year yield is trading around 4.106%.

- This saw the 2s10s yield curve move higher, +1.68 at 53.481.

- 10-Year’s found some buyers back towards 4.15%. Is that the top, I suspect we test the 4.20% area at some point where demand should again return. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Bloomberg - “The OECD warned that the global economy has yet to feel the full impact of Trump’s tariffs, despite recent resilience. It raised its forecast for growth to 3.2% this year, but expects momentum to moderate to 2.9% in 2026 amid higher import duties.”

- Samantha LaDuc on X: “Apollo’s Torsten Slok on US inflation: “72% of the CPI components are growing faster than the Fed’s 2% inflation target.”

- Robin Brooks on X: “Last week's Fed meeting was a hawkish catalyst for markets. In the run-up to that meeting, markets priced a lot more Fed easing, which pulled down longer-term US and French yields. But now there's no more Fed meeting to anchor long-term yields and they're up again.”

- Data/Events: MBA Mortgage Applications, Building Permits, New Home Sales

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cash Bonds Mostly Slightly Richer At Lunch

At the Tokyo lunch break, JGB futures are stronger, +8 compared to settlement levels, after yesterday's holiday.

- Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August.

- The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although it remains at much higher outright levels (52.0).

- On the services side for Japan, we remain at elevated levels. There remains a decent wedge between the manufacturing and services PMIs.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 1.3bp lower (20-year) to 0.3bp higher (40-year). The benchmark 10-year yield is 0.9bp lower at 1.645% versus the cycle high of 1.670%.

- Swap rates are flat to 2bps lower.