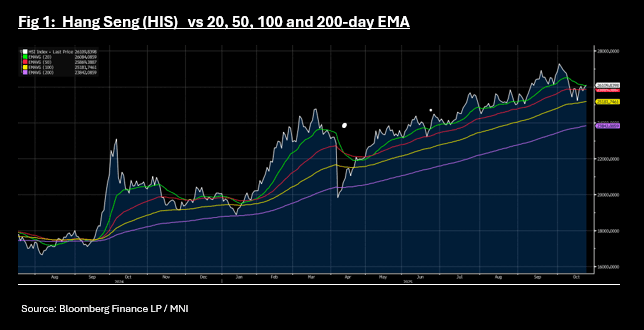

ASIA STOCKS: Strong Week for Region as Tech Leads; HSI Nears Key Technical

China stocks had suffered earlier this week as the Trump administration threatened to curb China's access to key software. As the four day conclave of the Communist Party's Central Committee concluded Thursday, new goals emerged in the next 5-Year plan of China's plan for self-reliance and strength in science and technology. This came as news that a US - China summit has been agreed. Tech stocks in general are strong today with key stocks like Samsung up +2.5% to reach new highs and the Hang Seng Tech Index up over 1%. Major bourses have delivered strong gains this week, with some hitting new all time highs.

- The Jakarta Composite has posted the biggest 5-day gains, up just on 5% in a week where the Central Bank surprised markets by remaining on hold. Since the lows of late March, the JCI is up just on 40% as the Prabowo Government undertakes a pro-growth policy approach.

- The KOSPI's 5-day gains are over 4.5% given the Tech story, and hit yet another new high as the Korea Economic Daily reported that President Lee is considering cutting the top rate on dividends (as per BBG).

- As the political happenings in Japan led to a new leader, the NIKKEI has gained strongly on hopes that inflation fighting packages are to be announced. The NIKKEI closed at new highs Tuesday before profit takers took over. For the week, the NIKKEI remains up over 3% with the Tech sector contributing strongly to gains.

- China's major bourses have all enjoyed solid gains this week as the momentum in the Tech sector globally, drove local prices alongside expectations for the new 5-Year plan. All major bourses are up with the outperformer the Shenzhen Composite, up +3.5%. The HSI in Hong Kong delivered gains of +3.4% for the week and is near the 20-day EMA, attempting to finish above it for the first time in a fortnight.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Mostly Slightly Richer At Lunch

At the Tokyo lunch break, JGB futures are stronger, +8 compared to settlement levels, after yesterday's holiday.

- Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August.

- The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although it remains at much higher outright levels (52.0).

- On the services side for Japan, we remain at elevated levels. There remains a decent wedge between the manufacturing and services PMIs.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 1.3bp lower (20-year) to 0.3bp higher (40-year). The benchmark 10-year yield is 0.9bp lower at 1.645% versus the cycle high of 1.670%.

- Swap rates are flat to 2bps lower.

MNI EXCLUSIVE: MNI Discusses BOJ's Must Haves For Further Hikes

CHINA: Bond Futures Mixed in Morning Trade

- China's major bond futures are moving in mixed trade this morning as the 10-Yr bond yield is stationary at 1.80%.

- The 10-Yr is lower by -0.03 at 107.72 and moves further below all major moving averages.

- The 2-Yr is flat at 102.35 and consolidates below all major moving averages. Above is the 20-day EMA of 102.38.