OIL: WTI Bounces on Key Technical, Set for Strongest Week Since June

Oct-24 03:50

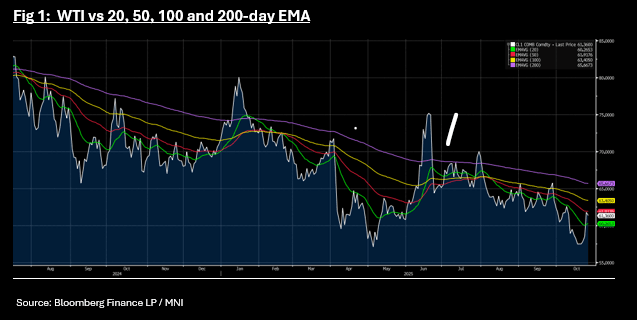

- Oil gave back some of last night's gains, yet remains set for it's strongest week since June.

- Up over +6.6% for the week, WTI has declined -0.65% to USD$61.39 bbl in the Asia trading day unable to break through the 50-day EMA of $61.91

- Brent is down -0.61% at US$65.59, yet remains up +7% week to date.

- Overnight was oil's biggest one day jump since June, oil gaining on the announcement of US sanctions on Russia's biggest oil companies Rosneft and Lukoil, in efforts to cut off revenue to Russia and limit its ability to continue the war in Ukraine.

- The sanctions come at a time when Ukraine attacks on Russian oil infrastructure has escalated increasing the possibility that global oil supply could be impacted by reduced Russian supply.

- Indian refiners have indicated that the latest sanctions will severely impact their ability to continue to buy Russian oil (as per BBG).

- The EU followed the US with new sanctions including targeting the Russian shadow fleet, a crack down on Russian crypto financing and a ban on LNG imports into Europe from 2027.

- Chinese state-owned companies including Sinopec canceled some purchases of seaborne Russian crude after the US blacklisted Rosneft PJSC and Lukoil PJSC, adding to signs of disruption in the oil market. The Chinese majors have begun to assess the impact of the US curbs, as well as similar moves by the European Union, according to people with knowledge of the situation, asking not to be identified discussing sensitive issues. The companies have paused purchases of some spot cargoes, mostly ESPO, a grade that ships from Russia’s Far East, (as per BBG)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Mostly Slightly Richer At Lunch

Sep-24 03:30

At the Tokyo lunch break, JGB futures are stronger, +8 compared to settlement levels, after yesterday's holiday.

- Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August.

- The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although it remains at much higher outright levels (52.0).

- On the services side for Japan, we remain at elevated levels. There remains a decent wedge between the manufacturing and services PMIs.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 1.3bp lower (20-year) to 0.3bp higher (40-year). The benchmark 10-year yield is 0.9bp lower at 1.645% versus the cycle high of 1.670%.

- Swap rates are flat to 2bps lower.

MNI EXCLUSIVE: MNI Discusses BOJ's Must Haves For Further Hikes

Sep-24 03:29

MNI discusses the BOJ's must-haves for further rate hikes. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA: Bond Futures Mixed in Morning Trade

Sep-24 03:24

- China's major bond futures are moving in mixed trade this morning as the 10-Yr bond yield is stationary at 1.80%.

- The 10-Yr is lower by -0.03 at 107.72 and moves further below all major moving averages.

- The 2-Yr is flat at 102.35 and consolidates below all major moving averages. Above is the 20-day EMA of 102.38.