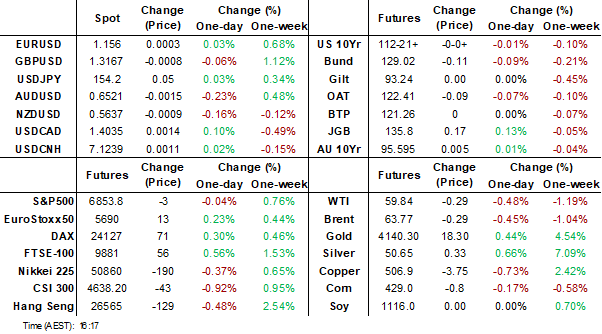

MNI EUROPEAN MARKETS ANALYSIS: JGB Back End Yields Higher

- As expected the US Senate passed a bill to re-open the US government, sending it the House. The USD has mostly been supported today, although USD/JPY stopped short of a 154.50 upside test.

- The JGB yield curve is steeper, with fiscal concerns weighing, while the 30yr auction delivered weak results.

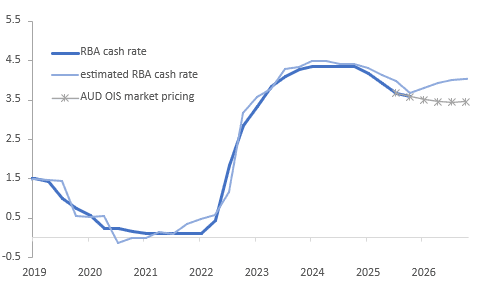

- When updated for Q3 CPI, Q2 GDP and the RBA’s November projections, our simple policy reaction function based on the core inflation and output gaps is signalling no further easing. See below for more details.

- The US bond market is shut for Veterans Day, which could impact oil trading volumes, but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

MARKETS

US TSYS: Futures Edge Lower Ahead of Veterans Day

In quiet day ahead of veterans' day, bond futures finished lower across most maturities. The US 10-Yr (TYZ5) is down -01 at 112-21 to remain below the 50-day EMA of 112-25+ and above the 100-day EMA of 112-13+.

Bonds finished the US trading session with marks as follows:

- The US 2-Yr is at 3.59%

- The US 5-Yr is at 3.715%

- The US 10-Yr is at 4.118%

- The US 30-Yr is at 4.706%

Equity markets across the region are strong with the KOSPI and NIKKEI leading the rally

The next focus for bond markets will be the US$42bn 10-Yr auction on the 13th, followed by the US$25bn 30-Yr auction on the 14th.

JGBS: Fiscal Stimulus Talk Weighs On 30Y Auction

JGB futures are stronger and at session highs, +18 compared to settlement levels, despite today’s lacklustre 30-year auction. The market is showing increasing unease about fiscal stimulus talk and its impact on longer-dated supply.

- The 30-year JGB auction delivered weak results. The low price fell short of dealer expectations of 100.45, per the Bloomberg survey. Moreover, the cover ratio decreased to 3.1248x from 3.4110x and the auction tail lengthened significantly to 0.27 from 0.17, indicating a deterioration in bidding strength.

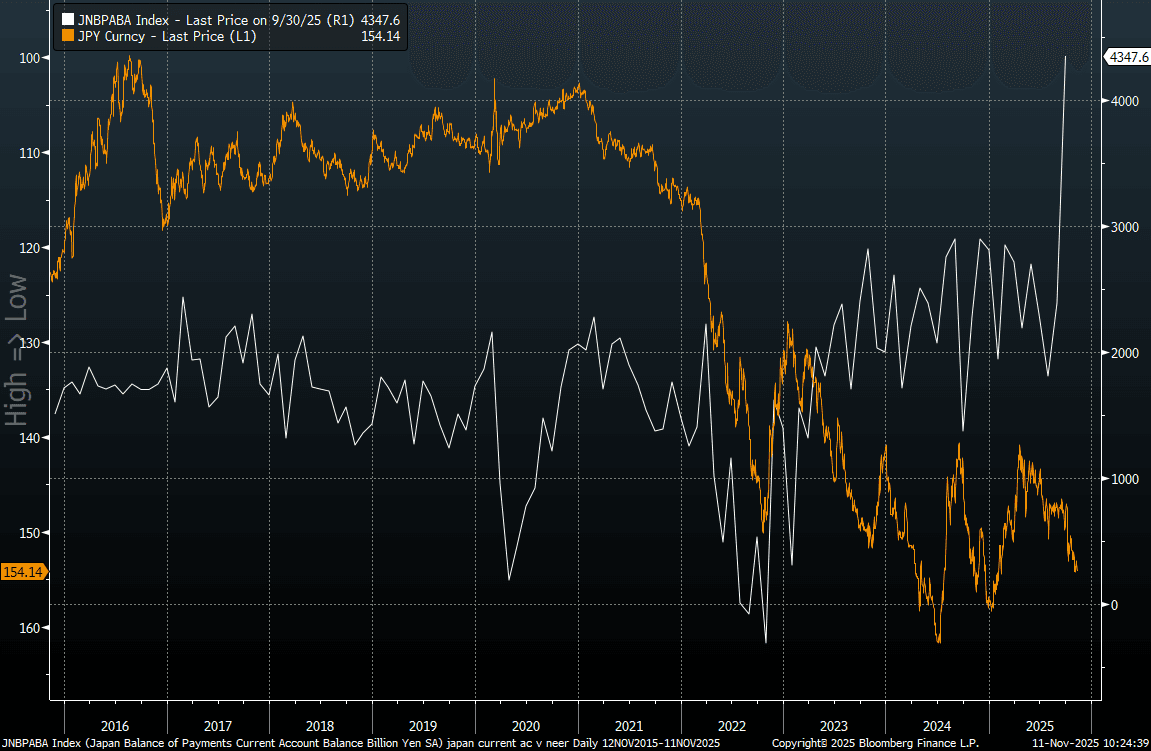

- MNI - Japan Sep trade and current account balance data were stronger than forecast, particularly on the current account side. In unadjusted terms we printed 4483.3bn, versus 2456.6bn projected and 3701.4bn prior. In seasonally adjust terms we were at 4347.6bn for the current account, close to double the consensus projection and prior outcome. This is the best outcome for at least a few decades.

- Cash JGBs have twist-steepened, with yields 2bps lower to 3bps higher across benchmarks. The benchmark 30-year yield is at 3.171% versus the cycle high of 3.351%. (see chart)

- Swap rates are 1bp lower to 2bps higher.

- Tomorrow, the local calendar will see Money Supply and Machine Tool Orders.

JAPAN DATA: Current A/C Surplus Surges On Income Inflows, But May Not Aid Yen

Japan Sep trade and current account balance data were stronger than forecast, particularly on the current account side. In unadjusted terms we printed ¥4483.3bn, versus ¥2456.6bn projected and ¥3701.4bn prior. In seasonally adjust terms we were at ¥4347.6bn for the current account, close to double the consensus projection and prior outcome. This is the best outcome for at least a few decades. This isn't necessarily a yen positive though, at least based off recent correlations. Current account shifts haven't coincided with yen shifts in recent years.

- The trade balance on a BoP basis aided the current account improvement. We were up to a surplus of ¥236bn, versus a projected deficit of -¥100.1bn. The trade balance remains within recent ranges. The Citi terms of trade proxy for Japan is pointing to positive trade balance outcomes continuing in the near term.

- The bigger driver for the current account improvement though was the surge in the primary income balance, ¥4728.1bn, versus ¥2968.4bn in Aug. These outcomes are usually fairly steady, but point to a pick in net income earned from Japan's offshore investments.

- The chart below plots USD/JPY, which is inverted on the chart (the orange line) against the current account position (the white line). It shows the lack of relationship between the two series, with much of the surplus in Japan potentially re-exported offshore via capital outflows.

- This may benefit the yen at some point, particularly if we see the US authorities (especially Tsy Secretary Bessent) making noises about yen being undervalued relative to Japan's external balances.

- However, this is likely to play out over the medium term rather than in the near term. Short term dynamics around the BoJ/Fed outlooks, which will drive US-JP yield differentials, along with broader risk trends, are likely to remain more important USD/JPY drivers.

Fig 1: Japan Current Account & USD/JPY (Inverted) Trends

Source: Bloomberg Finance L.P./MNI

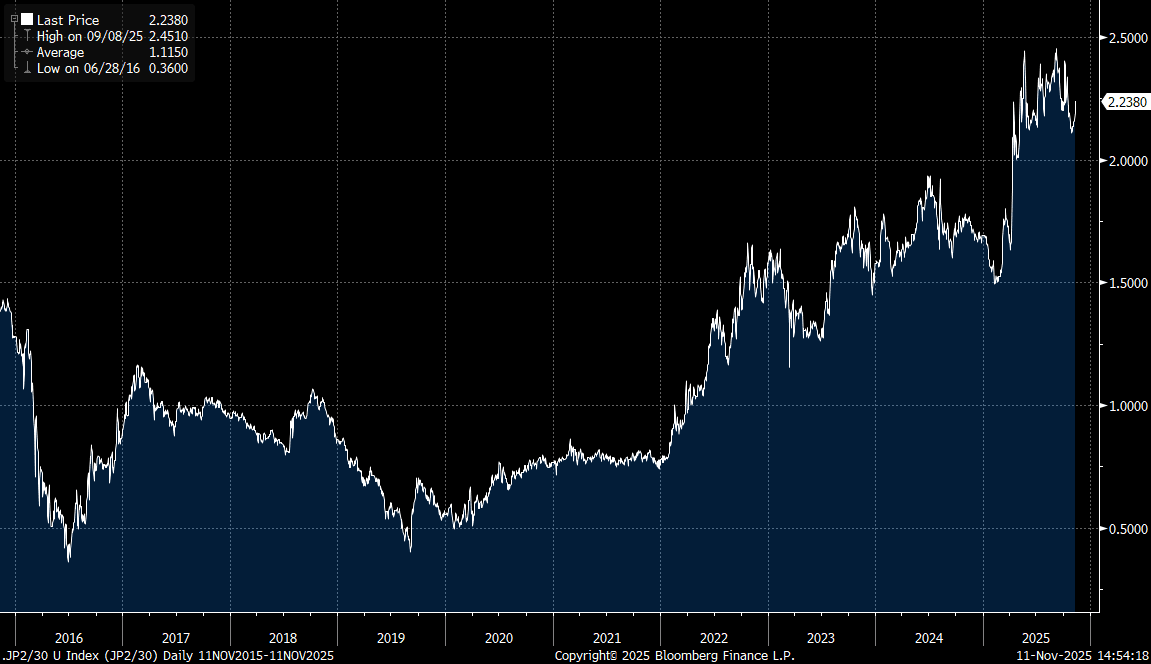

JAPAN: Risks Building For JGB Curve To Re-Visit Recent Cycle Highs

Japan PM Takaichi has again pushed back on Japan's inflation goals being met, noting that it can't be said that Japan has exited deflation yet (via BBG). She added that she would be communicating closely with the BoJ. It also follows earlier remarks in Nov, where Takaichi stated that Japan is around halfway to achieving its goal of stable inflation backed by wages growth. Push back on BoJ's tightening bias, coupled with concerns around fiscal slippage, could see the JGB yield curve return to recent highs and potentially extend higher. The 2/30s curve was last +224bps, with recent highs marked just above +245bps, see the chart below.

- BoJ hike odds for Dec are down a touch from recent highs, with around a 45% chance of a 25bps hike priced in at this stage.

- Takaichi also noted in her remarks that the bulk of the extra budget will go to families (presumably for cost of living relief). Boosting investment is also a key focus point, with 17 key industries identified (including AI, shipbuilding and defence, along with rare earths). Takaichi has noted Abenomics didn't boost economic growth enough.

- Details on the extra budget are expected in coming weeks, with sell-side viewpoints mixed on its potential size and how much pressure this may create in terms of the JGB outlook.

- Via BBG: " Yusuke Ikawa (of BNP Japan) expects fresh spending in the range of ¥15 trillion ($98 billion) to ¥20 trillion with the issuance of more bonds to finance it likely. Last year an extra budget provided ¥13.9 trillion in additional outlays for Ishiba’s economic measures."

- While AXA from late last week (also via BBG): "Currently, reports suggest the total size of the supplemental budget could reach around ¥10 trillion,” says Ryutaro Kimura, a senior fixed-income strategist at AXA Investment Managers. “However, by reallocating funds from existing budgets and utilizing proceeds from bonds issued in advance for next fiscal year’s budget, I expect that large-scale additional issuance can be avoided”.

- Beyond the extra budget, the new government is already looking at more expansive fiscal policy. The aim of achieving a primary balance surplus in the fiscal accounts is no longer a goal for a single year, but will be viewed from a longer-term perspective.

- Recent bond auction results point to unease, with today's 30-year JGB auction delivering weak results. Today’s result was also consistent with this month’s 10-year auction, which also demonstrated weak demand metrics.

Fig 1: JGBs 2/30 Curve Back On A Steepening Trend

Source: Bloomberg Finance L.P./MNI

AUSTRALIA: Easing Cycle May Be Done

When updated for Q3 CPI, Q2 GDP and the RBA’s November projections, our simple policy reaction function based on the core inflation and output gaps is signalling no further easing. As trimmed mean inflation doesn’t return to the 2.5% band mid-point by the end of 2027 on current assumptions, there is a risk of monetary tightening.

- The AUD OIS market has 17bp of easing priced in by September 2026 with almost nothing by the end of 2025.

- The reaction function implies around 75bp of easing in the year to Q3 2025 but that by Q2 2026 25bp of this has been reversed. The rate estimates then settle around 4% over H2 2026 and stay there in H1 2027.

- The equation uses a one quarter lead of trimmed mean inflation which the RBA revised up to 3.2% in Q4 2025 and Q2 2026 in its November projections. It then moderates towards 2.6%.

- Using the RBA’s GDP growth expectations of around 2%, the output gap is likely to be slightly negative over the forecast period.

- It is worth noting that econometric calculations are just estimates and not predictions.

Australia policy reaction function with trimmed mean CPI %

Source: MNI - Market News/LSEG

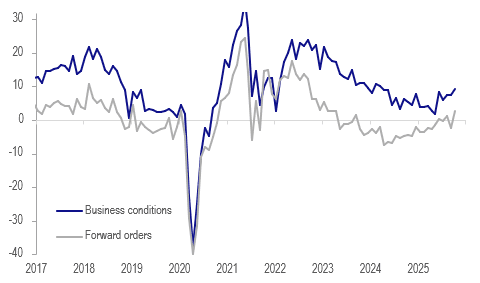

AUSTRALIA DATA: NAB Survey Signals Ongoing Recovery & Lower Inflation

NAB business confidence and conditions were little changed in October with the former down 1 point to +6 and the latter up 1 point to +9. The survey details were generally positive though with forward orders positive and their highest in two and a half years, investment up, labour demand steady and cost/price increases moderating. It is consistent with an ongoing economic recovery and contained inflation and therefore the RBA on hold.

Australia NAB business survey outlook

Source: MNI - Market News/LSEG

- Business conditions rose to their highest since March 2024 with profitability up 3 points, trading +5 and employment steady but one point below the 2025 average. Capital expenditure rose 4 points to +11. While exports remained positive, they are struggling as they weakened in October.

- The labour demand component is currently signalling a stabilisation in employment growth, which has trended lower since mid-year.

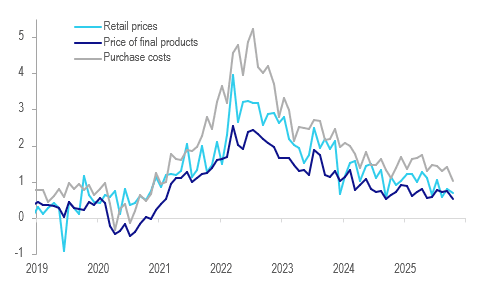

- The 3-month change in purchase costs moderated to 1.0%, the lowest since February 2021 and below Q3’s 1.4% average. Labour costs rose 1.5% 3m/3m down from 1.6% in September.

- Final product prices increased only 0.5% 3m/3m after 0.75% in Q3 and the slowest since February 2021. Retail prices increased 0.7% 3m/3m after Q3’s 0.8%.

Australia NAB business survey price/cost components % 3m/3m

Source: MNI - Market News/LSEG

AUSTRALIA DATA: Westpac Consumer Details Mixed, Spending Rise Not A Given

The details of the November Westpac consumer confidence survey are mixed signalling that there could be payback in December. It rose despite lower sentiment amongst mortgage holders as a group and less optimism regarding the labour market outlook but stronger domestic growth and less risk from US tariffs seemed to have driven the rebound into net optimism territory.

- Westpac asked about Christmas spending intentions and 15% said they would spend more than last year up from 11.6% in November 2024 with around 35% planning to spend less, similar to 2024. Westpac describes the responses as “less restrained” than 2024. It shows that the jump in confidence translating into strong spending is not assured.

- Family finances improved with expectations for a year ahead +12.3% to 109.1, significantly stronger than compared to a year ago, which Westpac believes was helped by the RBA not discussing a hike on 4 November despite the surprisingly high Q3 CPI. But 76% of respondents after the RBA decision to keep rates on hold expect rates to be on hold or higher in a year up from 60% in October.

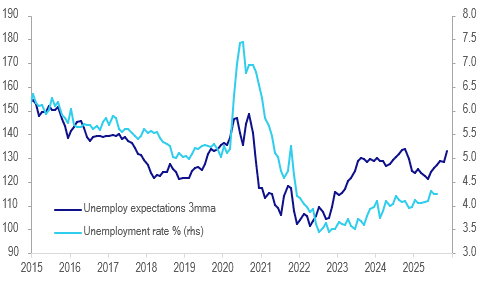

- The economic outlook for the next year and 5 years rose 16.6% and 15.3% respectively and are above their historical averages. But unemployment expectations jumped 9.3% to 139.5 driven by 18-24 year olds and the unemployed. The RBA sees the youth unemployment rate as a lead indicator of the labour market (October prints 13 November).

- The “time to buy a major item” rose 14.9% m/m to 111.6, highest in four years.

Australia Westpac unemployment expectations

Source: MNI - Market News/LSEG/ABS

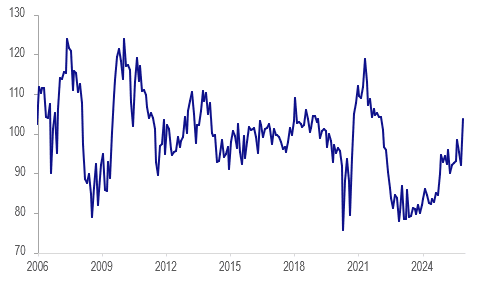

AUSTRALIA DATA: Sentiment Jumps, Higher Inflation & On Hold Rates Ignored

Despite lower rate cut and higher inflation expectations, Westpac consumer confidence surprisingly jumped 12.8% m/m to 103.8 in November, the highest since January 2022 and the largest monthly rise since Covid-impacted September 2020. Finally optimists exceeded pessimists, reflected in the “time to buy a major item” rising almost 15%. If sustained, then it is likely to reflect further recovery in the domestic economy and possibly a wealth effect from rising house prices.

- On Monday, RBA Deputy Governor Hauser noted that growth is already close to potential and thus the economy to capacity. While these concepts are difficult to estimate, any pickup in growth could potentially add to inflation. This large jump in confidence adds to the risk of that and the chance that rates won’t be cut further.

- Consumers don’t always behave in line with their survey responses and so monthly household spending data will be monitored closely to see if there is an increase in expenditure consistent with the pickup in confidence. October prints on 4 December with November 12 January.

- House prices are expected to rise with expectations +0.3% m/m to 172.4, a new record high. However, time to buy a home remains soft at 96.4.

Australia Westpac consumer confidence

Source: MNI - Market News/LSEG

AUSSIE BONDS: Grinding Cheaper After Mixed Confidence Data

ACGBs (YM -3.0 & XM -1.0) are modestly weaker.

- Cash ACGBs are 1-3bps cheaper, with a flattening bias, in today’s Asia-Pac session after today’s confidence data.

- The details of the November Westpac consumer confidence survey are mixed, signalling that there could be payback in December. It rose despite lower sentiment amongst mortgage holders as a group and less optimism regarding the labour market outlook.

- NAB business confidence and conditions were little changed in October, with the former down 1 point to +6 and the latter up 1 point to +9.

- The bills strip has bear-steepened, with pricing -2 to -4.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 8% probability, with a cumulative 14bps of easing priced by mid-2026.

- Tomorrow, the local calendar will see Home Loan data alongside RBA's Jones-Fireside Chat.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond tomorrow and A$800mn of the 1.75% 21 November 2032 bond on Friday.

BONDS: Subdued Session With Market Little Changed

NZGBs closed little changed, with benchmark yields flat to 1bp cheaper.

- The RBNZ’s Q4 survey of expectations posted unchanged inflation expectations. The central bank is likely to be relieved that not only are they within its 1-3% target band but they didn’t increase in the latest reading following the rise in Q3 CPI to 3.0% y/y from 2.7%, although the RBNZ’s measure of core held steady at 2.7%.

- The RBNZ has maintained for some time that the Q3 increase would be temporary and its August projections showed inflation moderating from Q4 and approaching the band midpoint in 2026 given the degree of spare capacity in the economy.

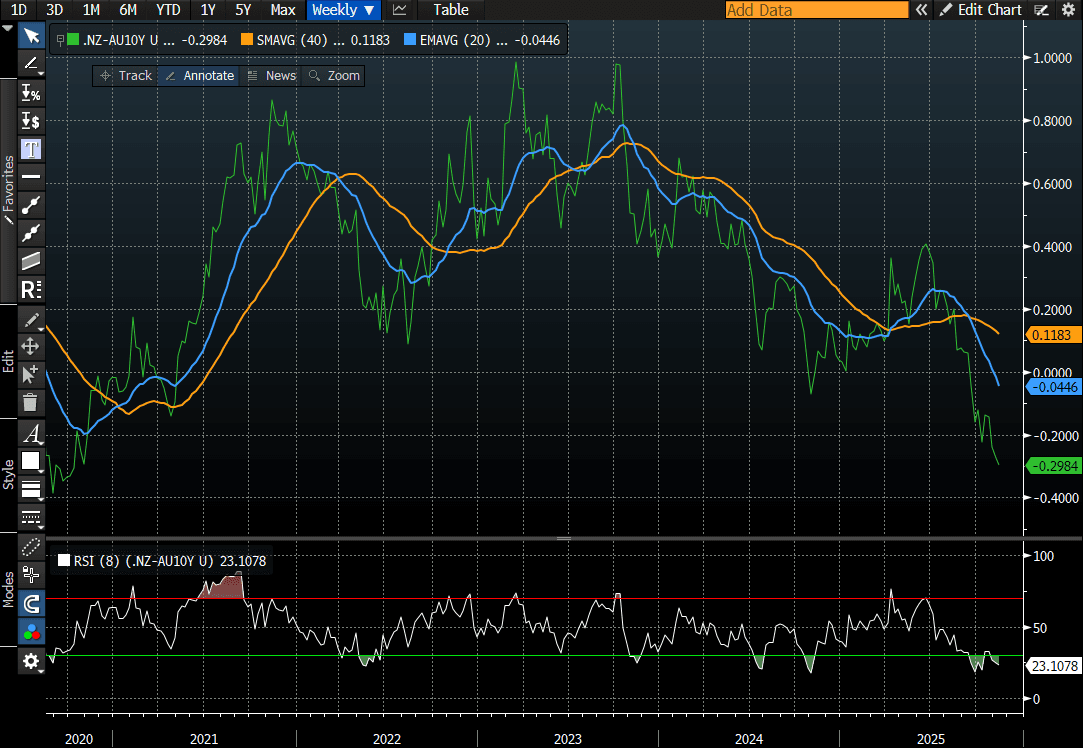

- NZ-AU 10-year differential is unchanged at -30bps, its lowest since 2020. (see chart)

- Swap rates closed are unchanged.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

Tomorrow, the local calendar will be empty ahead of Card Spending data on Thursday.

Bloomberg Finance LP

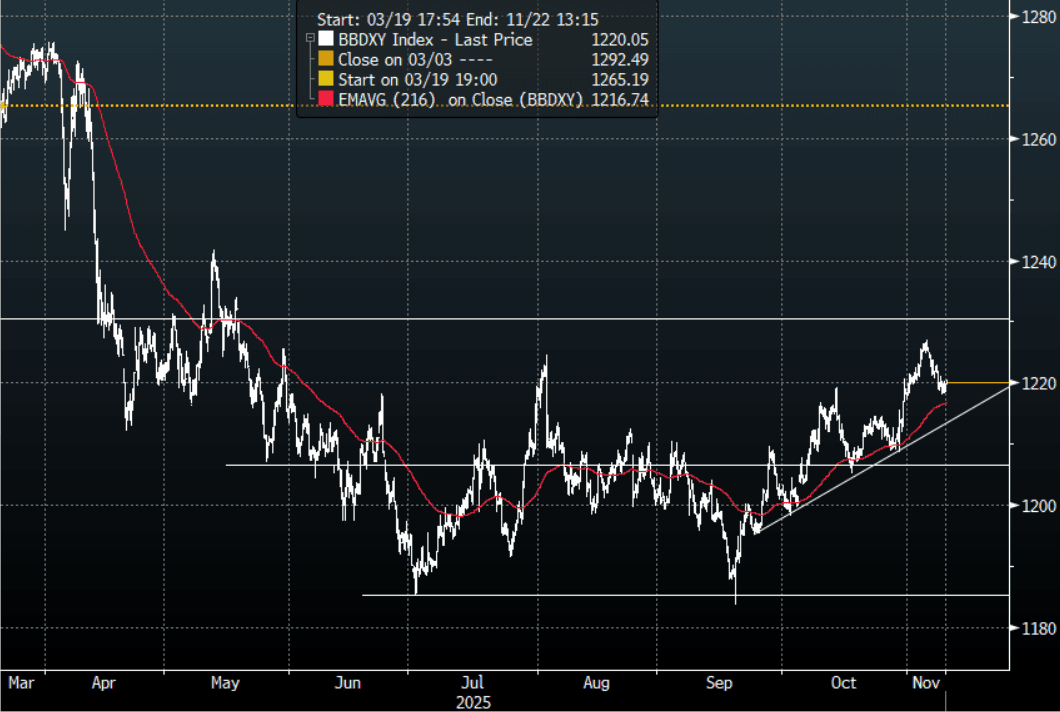

FOREX: Asia-Pac FX: USD Drifts Higher In Asia

The BBDXY has had a range today of 1218.71 - 1220.57 in the Asia-Pac session; it is currently trading around 1220, +0.10%. The USD has found some support between 1218-1220 and has consolidated here the last couple of sessions. USD/JPY should continue to be well supported but I suspect the USD will be sold against risk currencies like the AUD & NZD and the EUR if this surge in risk sentiment turns into an end of year rally for risk. I am caught undecided on the USD at the moment, I liked the fade into 1230 initially but short term I expect dips back toward 1210-1215 to now be supported first up. We could chop around sideways for a while while the market decides which way to go. Above 1230 and we could start to break higher, below 1205 and the downtrends momentum could be re-engaged.

- EUR/USD - Asian range 1.1547 - 1.1564, Asia is currently trading 1.1555. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This has been the pivot with the larger 1.1400-1.1900 range over the past few months.

- GBP/USD - Asian range 1.3158 - 1.3181, Asia is currently dealing around 1.3170. The pair continues to build on its bounce off the 1.3000 area. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.05%, Gold $4145, BBDXY 1220, Crude Oil $60.01

- Data/Events : EZ ZEW Survey Expectations, Germany ZEW Survey Expectations

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

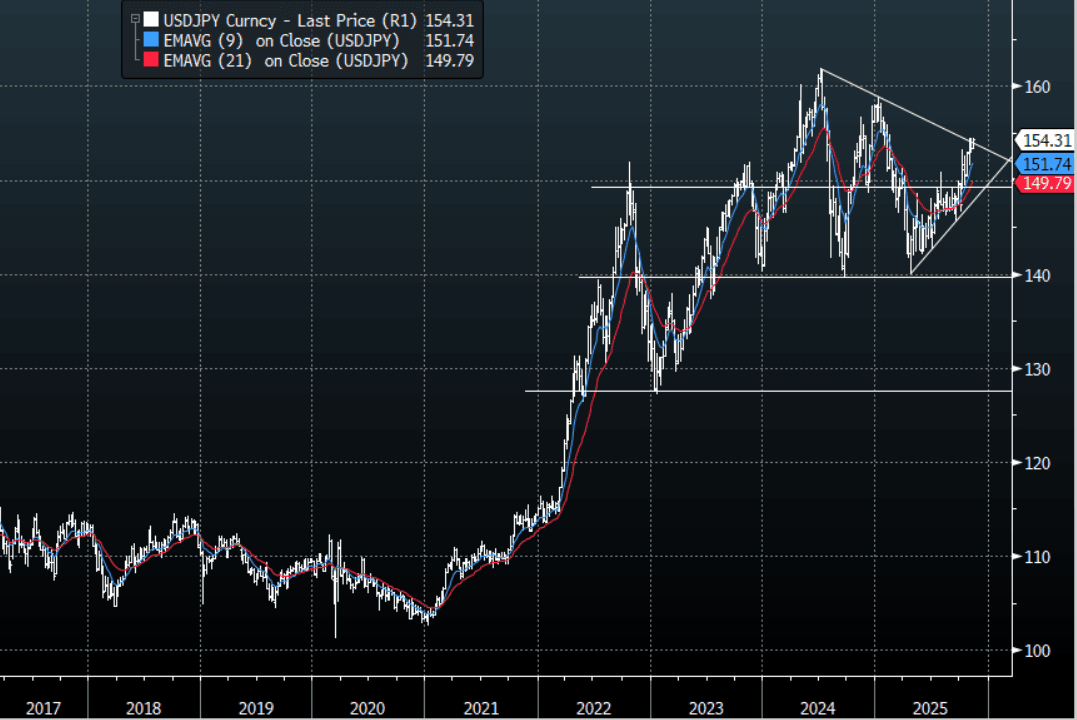

JPY: Asia-Pac: USD/JPY Stalls Toward 154.50, Consolidates Gains Above 154.00

The USD/JPY range today has been 154.02 - 154.49 in the Asia-Pac session, it is currently trading around 154.30, +0.10%. The pair extended higher in our session as it consolidated its recent gains above the 154.00 area. USD/JPY found solid demand around the 153.00 area last week and this return of positive sentiment has brought the focus back to the 154-155 resistance area. A sustained break above here is needed to potentially see the uptrend regain upward momentum, through here the focus would then turn toward the 160 area where I would start to become wary of intervention risks. If the pair is to move higher the dips towards 153.70/1.5400 should be supported on the day.

- MNI AU - Current A/C Surplus Surges On Income Inflows, But May Not Aid Yen: Japan Sep trade and current account balance data were stronger than forecast, particularly on the current account side. In unadjusted terms we printed 4483.3bn, versus 2456.6bn projected and 3701.4bn prior. In seasonally adjust terms we were at 4347.6bn for the current account, close to double the consensus projection and prior outcome. This is the best outcome for at least a few decades. This isn't necessarily a yen positive though, at least based off recent correlations. Current account shifts haven't coincided with yen shifts in recent years.

- The 30-year JGB auction delivered weak results. Today's result is consistent with this month's 10-year auction, which also demonstrated weak demand metrics

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

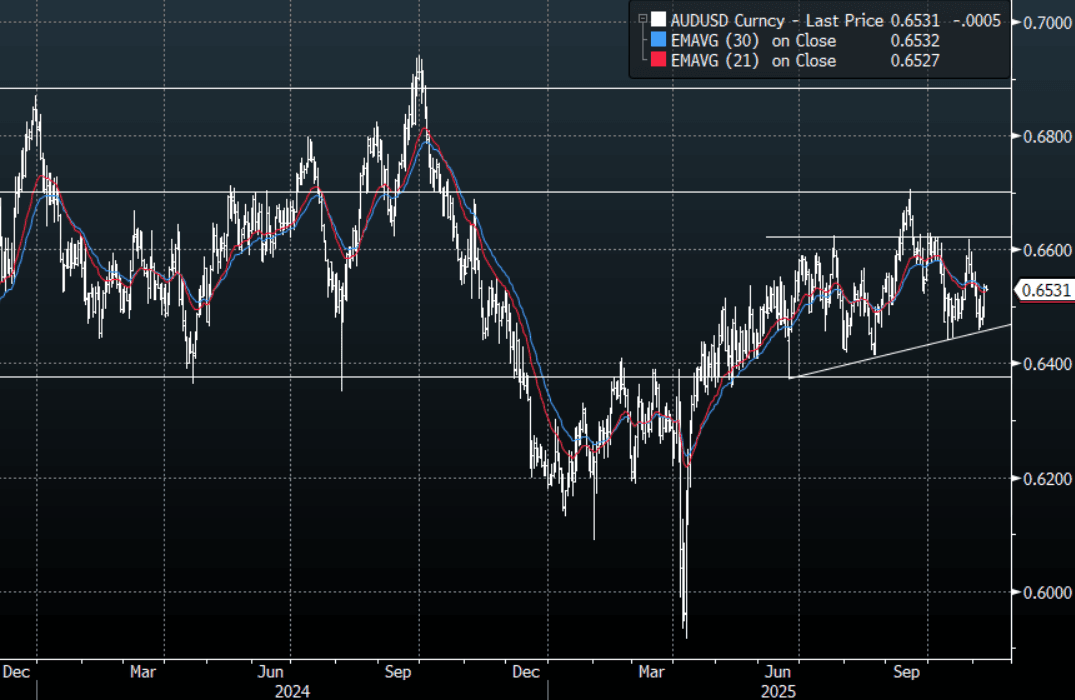

AUD: Asia-Pac: AUD/USD Drifts Lower, Consolidates Above 0.6500

The AUD/USD has had a range today of 0.6526 - 0.6539 in the Asia- Pac session, it is currently trading around 0.6530, -0.10%. The AUD/USD has drifted a little lower in our session as it consolidates above 0.6500. Is that the end of the correction ? Does the end of the shutdown override all the concerns that seemed to be weighing on the market last week, time will tell. The AUD will be one of the main beneficiaries while this positive sentiment dominates proceedings. The AUD/USD is probing the pivot around the 0.6550 area, a sustained push above here and the focus will turn back toward the 0.6650/0.6700 year highs. Look for intra-day support toward the 0.6500/0.6515 area first up.

- MNI AU - NAB Survey Signals Ongoing Recovery & Lower Inflation. NAB business confidence and conditions were little changed in October with the former down 1 point to +6 and the latter up 1 point to +9. The survey details were generally positive though with forward orders positive and their highest in two and a half years, investment up, labour demand steady and cost/price increases moderating. It is consistent with an ongoing economic recovery and contains inflation and therefore the RBA on hold.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6350(AUD396m), 0.6450(AUD 644m), 0.6650(AUD391m). Upcoming Close Strikes : 0.6500(AUD1.22b Nov 12), 0.6750(AUD2.17b Nov 14)- BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

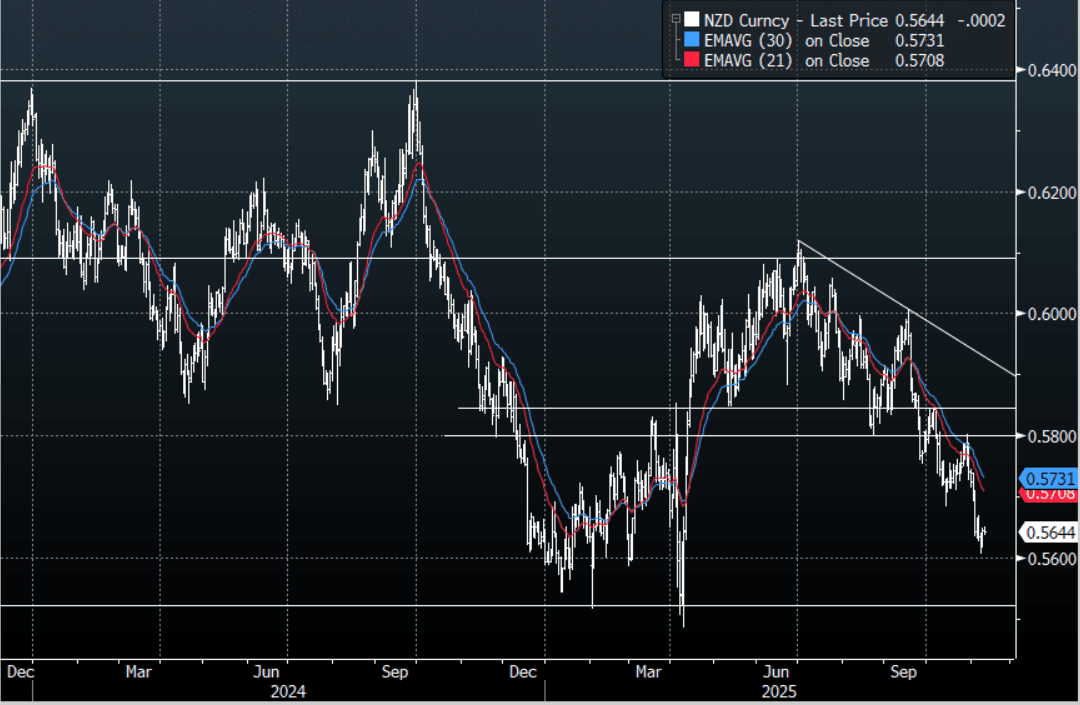

NZD: Asia-Pac: NZD/USD Consolidates Around 0.5650

The NZD/USD had a range today of 0.5636 - 0.5651 in the Asia-Pac session, going into the London open trading around 0.5645, -0.05%. The NZD continues to trade heavy but I continue to be a little wary of positioning in the NZD though as the market is small and traders tend to very quickly become all positioned the same way. The NZD does stand out as a vehicle to express a short in but should this bout of improved risk sentiment grow it will be tough for the NZD to ignore it and it could play catch up to the move at some point, if you feel this bounce in risk will fail and move back lower then the NZD remains a great way to express that. I still suspect any decent bounce will again attract sellers though. The first sell area on a pullback would be around 0.5750 and then the more pivotal 0.5850 area.

- The AU-NZ 10-year yield differential stands at +30bps, its widest since October 2020.

- MNI AU - Inflation Expectations Stable, RBNZ On Track For November Cut. The RBNZ’s Q4 survey of expectations posted unchanged inflation expectations. The central bank is likely to be relieved that not only are they within its 1-3% target band but they didn’t increase in the latest reading following the rise in Q3 CPI to 3.0% y/y from 2.7%, although the RBNZ’s measure of core held steady at 2.7%. The RBNZ has maintained for some time that the Q3 increase would be temporary and its August projections showed inflation moderating from Q4 and approaching the band midpoint in 2026 given the degree of spare capacity in the economy.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5380(NZD460m Nov 13), 0.5600(NZD538m Nov12), 0.5800(NZD461m Nov 12) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Skips Party, as Regional Bourses Strong on Tech/Shutdown End

The NIKKEI was buoyed by improving global sentiment as Sony Group has delivered decent quarterly earnings, with a share buyback as well. The KOSPI's relentless rally continues as key tech stocks rise between 4-6% on the potential for an end to the US shutdown. In Taiwan, TSMC reported with sales up over 16% in October, in line with forecasts, but the slowest month in six months. Markets are looking ahead to Nvidia's earnings outlook next week and with Asia's key tech stocks correlations growing with Nvidia, it is likely to drive sentiment into next week.

- The NIKKEI's gains were modest, a mere +0.24% and over 2.6% below last week's record high.

- The KOSPI is up +0.86% today and almost 14% over the last month. The sell off last week sees the KOSPI no longer overbought on the relative strength index, providing potential upside should Nvidia's results be in line or better than expected.

- China's bourses have missed the rally today with all major bourses down. All major bourses remain above all moving averages, with upward sloping trend lines suggesting that the positive trend remains in place. Despite this the Hang Seng is down -0.20%, the CSI 300 -0.67%, Shanghai down -0.38% and Shenzhen down -0.32%.

- South East Asia's major bourses are mixed with SE Thai and Jakarta Comp down, whilst the FTSE Malay KLCI is up +0.58% and the FTSE Straits Times in Singapore +1.1%. For the KLCI, it is the best start to a trading week since the end of September.

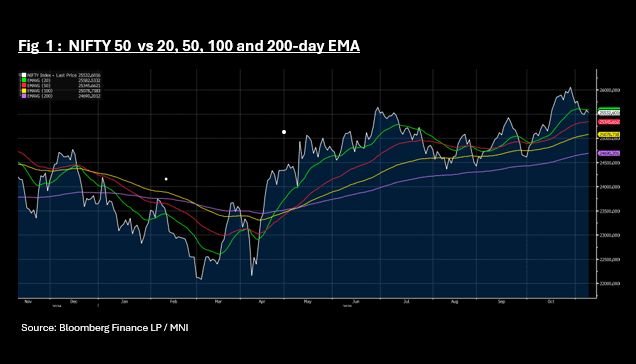

- Whilst India's NIFTY 50's finished higher yesterday, it finished on a weakening trend; giving back earlier gains. That sentiment flowed over into today with falls of -0.21% to 25,535 as the index fails to break above the 20-day EMA of 25,582.

ASIA STOCKS: Better Global Equity Sentiment Fails To Lift SK/Taiwan Inflows

Yesterday's equity market rebounds for both South Korea and Taiwan didn't aid offshore inflows into these markets. We saw modest outflow trends continue despite the better global equity tone, as market sentiment was boosted by signs the US government shutdown would end. For South Korea, the positive price action for the Kospi has continued today, with the index up a further +1.75%, putting the index back around 4140/45. Fresh record highs above 4225/30 aren't too far away. Early trends, per the NBUY function on BBG, point to positive inflows so far today, but less than $100mn at this stage.

- For Taiwan, late yesterday TSMC reported a 16.9%y/y rise in sales for Oct, which was the slowest rise since Feb 2024, creating some AI demand concerns. Still, this was in line with analyst estimates, while BBG noted that FX shifts may have played a role. Also note this follows the bumper export number for Oct, led by the tech/chip side (up nearly 50%). TSMC shares remained supported on dips but we remain sub recent highs, last around TWD1480.

- Elsewhere, Indian inflows recovered into the end of last week, bringing the 5-day sum back into positive territory. Earlier remarks from US President Trump stated a US-India trade deal pretty close and that Indian tariff rates would come down at some stage. Indian equities have struggled since the start of Nov, but regained some ground yesterday.

- In South East Asia, Indonesia remains the main positive, with YTD outflows continuing to be pared back. The strong inflows for the Philippines last Friday wasn't repeated on Monday.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -114 | -4875 | -1761 |

| Taiwan (USDmn) | -273 | -3759 | 1013 |

| India (USDmn)* | 872 | 274 | -15888 |

| Indonesia (USDmn) | 55 | 170 | -2293 |

| Thailand (USDmn) | -33 | -92 | -3088 |

| Malaysia (USDmn) | 15 | 32 | -4179 |

| Philippines (USDmn) | 2 | 102 | -673 |

| Total (USDmn) | 524 | -8148 | -26869 |

| * Data Up To Nov 7 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Lower As Risk Sentiment Stabilises & Waits For November Reports

Oil prices are slightly lower in Tuesday’s APAC session following moderate gains yesterday as risk sentiment stabilised. WTI is down 0.3% to $59.96/bbl but it has spent much of the session below $60. It made a high of $60.12 before moderating again. Brent is 0.2% lower at $63.95/bbl after reaching $64.06. The USD index is up 0.1%, likely pressuring dollar-denominated crude.

- With the support of a number of Democrats, the bill to provide US government funding until 30 January passed the Senate. The House of Reps will vote on Wednesday EST.

- After Saudi Arabia reduced its price premium for shipments to Asia, Kuwait has set December deliveries to Europe at a $2/bbl discount while the US faces a $2.90/bbl premium.

- Attention remains firmly on the expected record 2026 market surplus with the IEA’s monthly report published on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November. The IEA increased its 2026 surplus forecast in its October monthly report.

- US President Trump said that a US-India trade deal is close which would reduce the average tariff rate. However, Russia’s Interfax reported that India continues to buy Russian crude despite Trump commending them for reducing purchases.

- The US bond market is shut for Veterans Day, which could impact oil trading volumes, but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

GOLD: Release Of US Delayed Data Could Drive Fed Easing, Political Risks Persist

Gold prices have not only held onto Monday’s 2.9% gain but have risen further despite a stronger US dollar (BBDXY +0.1%) as risk appetite has been more stable. Bullion is up 0.7% to $4144.5/oz after a high of $4149.0, approaching resistance at $4161.4, 22 October high. It has found significant support from progress to end the US government shutdown, which will allow data to be released again. Clarity on the economy and the outlook is key to the 10 December Fed decision.

- With the support of a number of Democrats, the bill to provide government funding until 30 January passed the Senate. The House of Reps will vote on Wednesday EST and if it passes it will go to President Trump to be signed. He has voiced his support. It could then take a few days for operations to resume.

- With funding only assured to the end of January, another impasse next year is clearly possible. A vote by December on extending healthcare benefits was promised to Democrats, which could again be a hurdle to further financing.

- Silver is up 0.9% to $50.97 after reaching $51.142, breaching initial resistance at $51.071, a Fibonacci retracement point.

- Equities are mixed with the KOSPI up 1.0%, Hang Seng down 0.2% but S&P e-mini flat. Oil prices are lower with WTI -0.2% to $59.99/bbl. Copper is down 0.4%.

- The US bond market is shut for Veterans Day but equities will be open. Later ECB President Lagarde speaks. US October NFIB small business optimism, UK labour market data and euro area /German November ZEW print.

ASIA FX: USD/KRW To Fresh Multi Month Highs, Steady Trends Elsewhere

In North East Asia FX, the main focus point has been on fresh highs in USD/KRW. The pair is comfortably above 1460 to fresh multi month highs. USD/CNH is a little high, but at 7.1250 remains within recent ranges. USD/TWD spot is little changed.

- USD/KRW was last 1464/65, up around 0.50% versus end Monday levels (session highs rest at 1467.5). Yesterday's relief rally in the won proved to be fleeting. We had USD/JPY levels earlier (threatening a break above 154.50), but even as this pair has softened somewhat, there has been little relief for USD/KRW. Local equities are higher, but after being up +2.6% at one stage we were last +0.40%. Offshore inflows have been very limited so far today. Price action in USD/KRW points to on-going domestic capital outflow pressures. Focus will be on if we see a policy response around verbal FX jawboning, or actual intervention, if we move towards 1480.

- USD/CNH has edged a little higher so far today, last near 7.1245/50, in line with broader USD trends (the dollar is up against most of the G10), but beta with respect to such moves remains very modest. CNH/JPY got to highs earlier of 21.6821, but we sit back under 21.65 in latest dealings, with the yen leg continuing to drive most of the volatility.

- USD/TWD is little changed in both the spot and 1 month NDF space. We were last near 30.99 for spot. Local equities are higher, but only marginally and like South Korea are away from best levels.

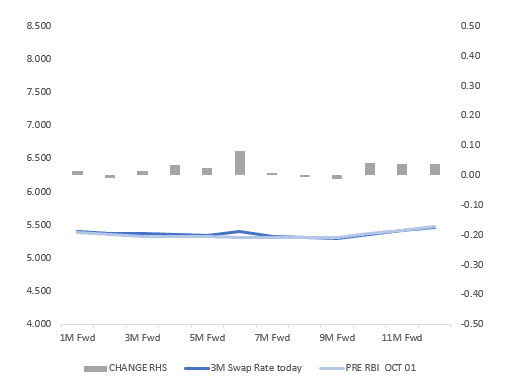

INDIA: INR Swaps Indicate Easing Cycle End is Near

- With just over a month to go before the next RBI meeting, swaps and bond signals are no longer suggesting that the last meeting for the year will see a cut.

- The swaps market had 25bps of cuts over the next month and 29bps over the next two at the beginning of last week, whilst the MIPR function on Bloomberg has 29 cuts priced in over the next month.

- Today that it remains at 0 bps (from -7bps last week) over the next month and -1bps (from -9bps last week) over two with the BBG MIPR function down to -9bps (from -22bps last week) over the next year.

- The next focus for markets in India will be October CPI out on the 12th, where if forecasts are correct will reach a new low of 0.40% on falling food prices given strong harvest and the first month of impact from the changes to GST

- If swaps pricing is correct, that looks likely nearing the end of the tightening cycle with very little priced in over the next 12 months and may suggest that bond yields have room to move higher from here.

- The market pricing is somewhat at odds with the MPC who at their last meeting where rates were maintained at 5.50%, also maintained their neutral stance. The market is likely hinging on the fact that 2 of the 6 members voted for an accommodative stance.

- At the time of the last meeting on Oct 1, USDINR closed at 88.69 only to rally into the back end of October. However in recent sessions this has given back and it is back at the Oct 1 level today. Headlines overnight on a potential trade deal could be the catalyst for a rally for the Rupee, which would be timely heading into the next RBI meeting on December 5.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0820/0920 | ECB Lagarde Video Message at Bank of Albania | ||

| 11/11/2025 | 0830/0930 | Riksbank Minutes | ||

| 11/11/2025 | 0830/0830 | BOE Greene in Panel at UBS European Conference | ||

| 11/11/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 11/11/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 11/11/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 11/11/2025 | 1200/1200 | BOE APF Quarterly Report | ||

| 11/11/2025 | - | *** | Money Supply | |

| 11/11/2025 | - | *** | New Loans | |

| 11/11/2025 | - | *** | Social Financing | |

| 11/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 11/11/2025 | 0325/2225 | Fed Governor Michael Barr | ||

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0700/0800 | *** | Germany CPI (f) | |

| 12/11/2025 | 0900/1000 | * | Industrial Production | |

| 12/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 12/11/2025 | 1045/1145 | ECB Schnabel Speech at BNP Paribas | ||

| 12/11/2025 | 1140/1240 | ECB de Guindos at FIBI International Banking Conference | ||

| 12/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 12/11/2025 | 1205/1205 | BOE Pill in Panel at International Monetary Research Conference | ||

| 12/11/2025 | - | ECB Lagarde, Cipollone at Eurogroup Meeting in Brussels | ||

| 12/11/2025 | - | BOE MPG Meeting | ||

| 12/11/2025 | 1330/0830 | * | Building Permits |