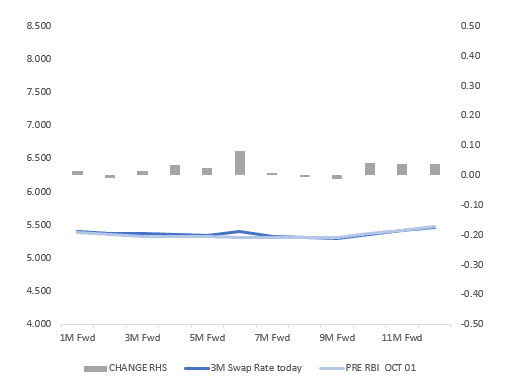

INDIA: INR Swaps Indicate Easing Cycle End is Near

- With just over a month to go before the next RBI meeting, swaps and bond signals are no longer suggesting that the last meeting for the year will see a cut.

- The swaps market had 25bps of cuts over the next month and 29bps over the next two at the beginning of last week, whilst the MIPR function on Bloomberg has 29 cuts priced in over the next month.

- Today that it remains at 0 bps (from -7bps last week) over the next month and -1bps (from -9bps last week) over two with the BBG MIPR function down to -9bps (from -22bps last week) over the next year.

- The next focus for markets in India will be October CPI out on the 12th, where if forecasts are correct will reach a new low of 0.40% on falling food prices given strong harvest and the first month of impact from the changes to GST

- If swaps pricing is correct, that looks likely nearing the end of the tightening cycle with very little priced in over the next 12 months and may suggest that bond yields have room to move higher from here.

- The market pricing is somewhat at odds with the MPC who at their last meeting where rates were maintained at 5.50%, also maintained their neutral stance. The market is likely hinging on the fact that 2 of the 6 members voted for an accommodative stance.

- At the time of the last meeting on Oct 1, USDINR closed at 88.69 only to rally into the back end of October. However in recent sessions this has given back and it is back at the Oct 1 level today. Headlines overnight on a potential trade deal could be the catalyst for a rally for the Rupee, which would be timely heading into the next RBI meeting on December 5.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Oval Office Announcement Underway Shortly

US President Donald Trump is shortly due to deliver an announcement in the White House Oval Office. LIVESTREAM The announcement is expected to relate to drug pricing and could follow a similar template to a recent pledge from Pfizer.

- The announcement will be Trump's first press remarks since a market-moving Truth Social statement earlier today in which Trump suggested calling off a meeting with Chinese President Xi Jinping and raising tariffs on China in response to new export controls from Beijing on rare earths. See earlier bullets here and here.

RATINGS: Moody's Completes Periodic Review Of Belgium, No Rating Action

No ratings actions for Belgium from Moody's, which is quoted in a press release on Bloomberg: "Moody's Ratings (Moody's) has completed a periodic review of the ratings of Belgium and other ratings that are associated with this issuer. The review was conducted through a rating committee held on 2 October 2025 in which we reassessed the appropriateness of the ratings in the context of the relevant principal methodology(ies), and recent developments. This publication does not announce a credit rating action and is not an indication of whether or not a credit rating action is likely in the near future."

- There had been some speculation there could be a ratings action - MNI wrote Thursday: "* Moody's on Belgium (Current rating Aa3, Outlook Negative): We expect Moody's to maintain their current stance in the absence of 2026 budget details."

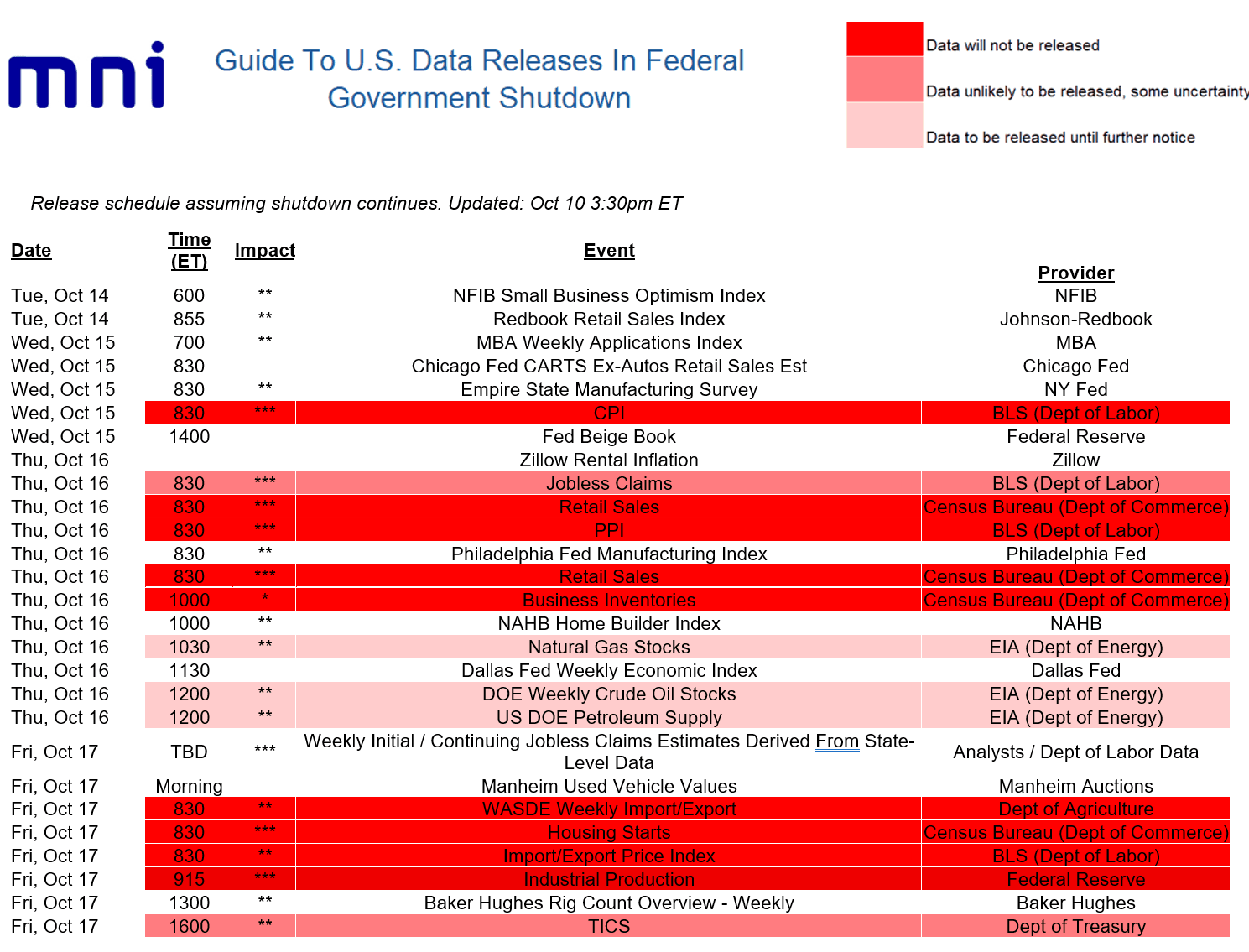

MACRO ANALYSIS: US Macro Week Ahead: No CPI, But Plenty Of Pre-Blackout FedSpeak

Below is the week’s data schedule, with MNI’s annotation of whether or not data will be postponed.

- As we went to press, the Fed announced that next week's Industrial Production data will be postponed (was due to be published next Friday Oct 17) as the data “incorporate a range of data from other government agencies, the publication of which has been delayed as a result of the federal government shutdown.”

- We won’t be getting September CPI as scheduled on Oct 15, but at least the BLS announced it will publish the data on Oct 24.

- As such next week we’ll be looking at some under-covered data points, including the Redbook weekly and Chicago Fed’s CARTS retail sales data (in lieu of the Census Bureau retail sales report), with a little more focus than usual on regional Fed manufacturing indices (NY, Philadelphia).

- Once again, the dearth of tier-one data leaves Fed commentary in focus ahead of the pre-FOMC blackout period: highlights for us are Philadelphia Fed President Paulson making her first comments on monetary policy on Monday since being appointed in the summer, while as always Chair Powell bears watching on Tuesday (we also hear from Bowman, Waller, Collins, Miran, Schmid, and Musalem).

- Additionally we get the latest Beige Book which was already key given the FOMC was already increasingly focused on anecdotal information as it attempts to navigate murky economic waters.