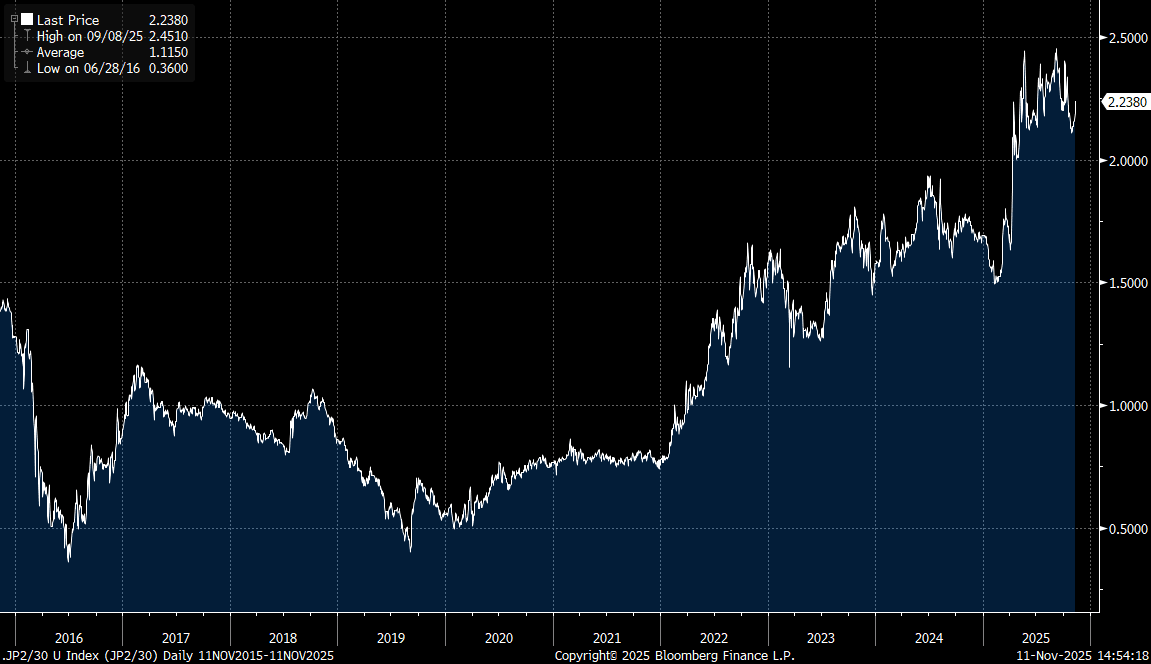

JAPAN: Risks Building For JGB Curve To Re-Visit Recent Cycle Highs

Japan PM Takaichi has again pushed back on Japan's inflation goals being met, noting that it can't be said that Japan has exited deflation yet (via BBG). She added that she would be communicating closely with the BoJ. It also follows earlier remarks in Nov, where Takaichi stated that Japan is around halfway to achieving its goal of stable inflation backed by wages growth. Push back on BoJ's tightening bias, coupled with concerns around fiscal slippage, could see the JGB yield curve return to recent highs and potentially extend higher. The 2/30s curve was last +224bps, with recent highs marked just above +245bps, see the chart below.

- BoJ hike odds for Dec are down a touch from recent highs, with around a 45% chance of a 25bps hike priced in at this stage.

- Takaichi also noted in her remarks that the bulk of the extra budget will go to families (presumably for cost of living relief). Boosting investment is also a key focus point, with 17 key industries identified (including AI, shipbuilding and defence, along with rare earths). Takaichi has noted Abenomics didn't boost economic growth enough.

- Details on the extra budget are expected in coming weeks, with sell-side viewpoints mixed on its potential size and how much pressure this may create in terms of the JGB outlook.

- Via BBG: " Yusuke Ikawa (of BNP Japan) expects fresh spending in the range of ¥15 trillion ($98 billion) to ¥20 trillion with the issuance of more bonds to finance it likely. Last year an extra budget provided ¥13.9 trillion in additional outlays for Ishiba’s economic measures."

- While AXA from late last week (also via BBG): "Currently, reports suggest the total size of the supplemental budget could reach around ¥10 trillion,” says Ryutaro Kimura, a senior fixed-income strategist at AXA Investment Managers. “However, by reallocating funds from existing budgets and utilizing proceeds from bonds issued in advance for next fiscal year’s budget, I expect that large-scale additional issuance can be avoided”.

- Beyond the extra budget, the new government is already looking at more expansive fiscal policy. The aim of achieving a primary balance surplus in the fiscal accounts is no longer a goal for a single year, but will be viewed from a longer-term perspective.

- Recent bond auction results point to unease, with today's 30-year JGB auction delivering weak results. Today’s result was also consistent with this month’s 10-year auction, which also demonstrated weak demand metrics.

Fig 1: JGBs 2/30 Curve Back On A Steepening Trend

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Oval Office Announcement Underway Shortly

US President Donald Trump is shortly due to deliver an announcement in the White House Oval Office. LIVESTREAM The announcement is expected to relate to drug pricing and could follow a similar template to a recent pledge from Pfizer.

- The announcement will be Trump's first press remarks since a market-moving Truth Social statement earlier today in which Trump suggested calling off a meeting with Chinese President Xi Jinping and raising tariffs on China in response to new export controls from Beijing on rare earths. See earlier bullets here and here.

RATINGS: Moody's Completes Periodic Review Of Belgium, No Rating Action

No ratings actions for Belgium from Moody's, which is quoted in a press release on Bloomberg: "Moody's Ratings (Moody's) has completed a periodic review of the ratings of Belgium and other ratings that are associated with this issuer. The review was conducted through a rating committee held on 2 October 2025 in which we reassessed the appropriateness of the ratings in the context of the relevant principal methodology(ies), and recent developments. This publication does not announce a credit rating action and is not an indication of whether or not a credit rating action is likely in the near future."

- There had been some speculation there could be a ratings action - MNI wrote Thursday: "* Moody's on Belgium (Current rating Aa3, Outlook Negative): We expect Moody's to maintain their current stance in the absence of 2026 budget details."

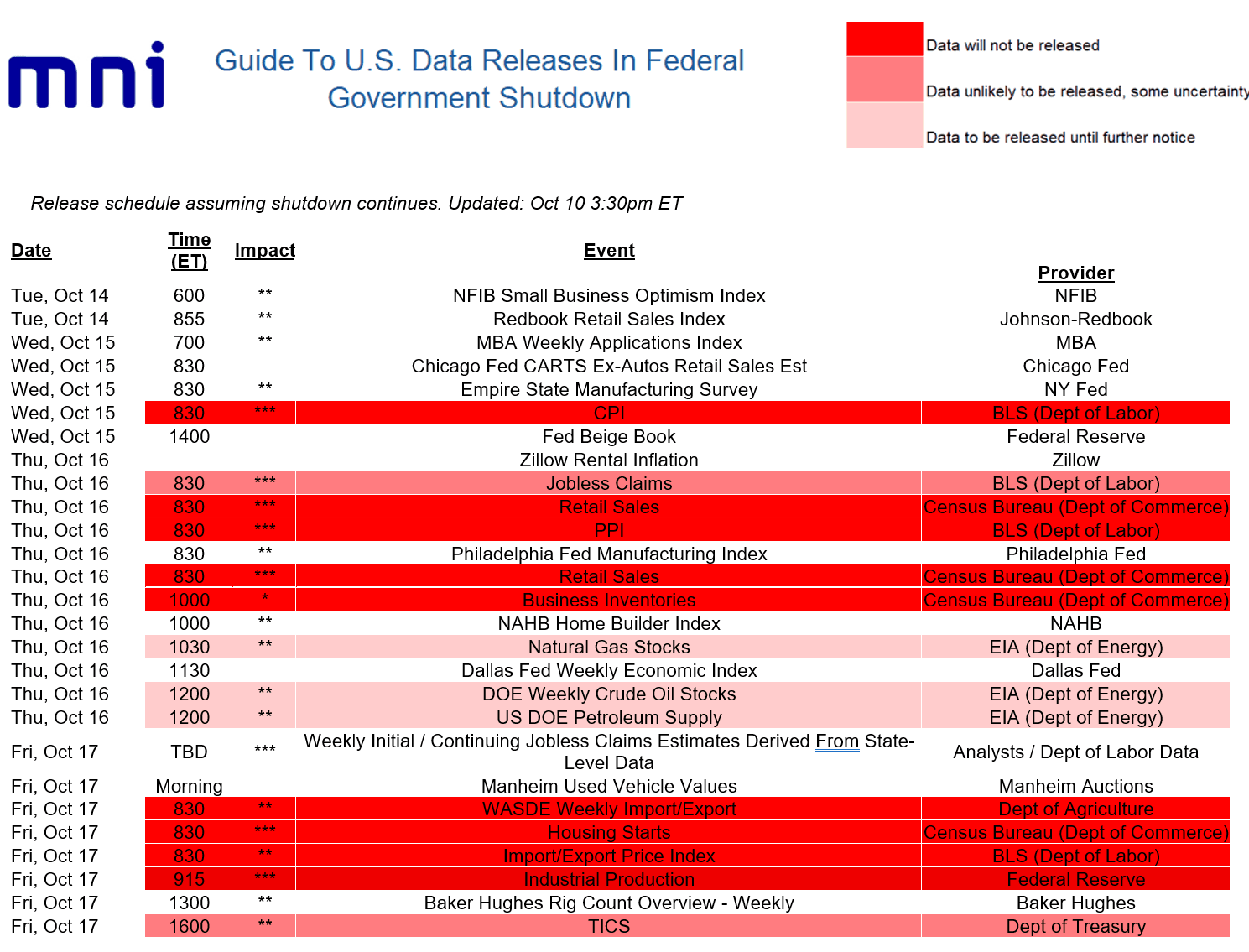

MACRO ANALYSIS: US Macro Week Ahead: No CPI, But Plenty Of Pre-Blackout FedSpeak

Below is the week’s data schedule, with MNI’s annotation of whether or not data will be postponed.

- As we went to press, the Fed announced that next week's Industrial Production data will be postponed (was due to be published next Friday Oct 17) as the data “incorporate a range of data from other government agencies, the publication of which has been delayed as a result of the federal government shutdown.”

- We won’t be getting September CPI as scheduled on Oct 15, but at least the BLS announced it will publish the data on Oct 24.

- As such next week we’ll be looking at some under-covered data points, including the Redbook weekly and Chicago Fed’s CARTS retail sales data (in lieu of the Census Bureau retail sales report), with a little more focus than usual on regional Fed manufacturing indices (NY, Philadelphia).

- Once again, the dearth of tier-one data leaves Fed commentary in focus ahead of the pre-FOMC blackout period: highlights for us are Philadelphia Fed President Paulson making her first comments on monetary policy on Monday since being appointed in the summer, while as always Chair Powell bears watching on Tuesday (we also hear from Bowman, Waller, Collins, Miran, Schmid, and Musalem).

- Additionally we get the latest Beige Book which was already key given the FOMC was already increasingly focused on anecdotal information as it attempts to navigate murky economic waters.