MNI EUROPEAN MARKETS ANALYSIS: Inflation and FOMC in Focus

- With financial markets globally waiting for the outcome from the FOMC, Asia markets had a double shot of inflation data to focus on today. In Japan the NIKKEI was weak as stronger than expected producer pricing data refocused attention on a potential BOJ hike. In China whilst November CPI was the strongest in over a year, it remains well below the target and PPI contracted more than expected, weighing on equities.

- Asia FX markets were also mixed as the Yen gained on rate hike expectations whilst the Won fell again despite news that the National Pension in Korea was selling dollars.

- Looking ahead it is all about the FOMC with other data releases in Europe being CPI from Norway and Industrial Production in Italy and the ECB's Lagarde is being interviewed to discuss currencies.

MARKETS

US TSYS: FOMC Next, Eyes on the 2026 Outlook

US bond futures are flat to modestly better today in a low volume day. As markets await the FOMC decision the US-10-Yr opened with a modest bid tone to reach 112-04+ before falling back to where it started around 112-03+.

Cash was better bid with yields 0.5bp - 1.0bps lower across the curve with 5-Yr and 7-Yr the outperformers.

- The 2-Yr is down -0.8bps to 3.611%

- The 5-Yr is down -1.0bps to 3.78%

- The 10-yr is down -0.8bps to 4.182%

- The 30-Yr is down -0.7bps to 4.802

Tonight's auction will be a US$69 Bln 17-Week Bills.

SEP/Dot Plot: The lack of major data since the September projections round portends only limited changes to the macro and rate forecasts in the December edition out Wednesday.

- None of the rate dot medians are expected to change, with 2025 confirmed at 3.6% (though with an unusual amount of disagreement in the dot distribution for an end-year SEP in a form of "soft dissent" against the cut), 2026 at 3.4% (implying one 25bp cut), with 2027 at 3.1% (another 25bp cut).

- In short, we expect most of the attention to be on the rate distribution. For 2026, the September dots were closely poised between 3.4% and 3.1% (10 above 3.25% vs 9 below 3.25%). We don't see much change here but if anything the risks to the median skew to the downside. For example, if one member who put their dot at 3.4% in September also saw rates ending 2025 at 3.9%, they might mark-to-market the rate view one notch lower.

- We'll also be watching for any dots implying a 2026 hike (we would expect at least one seeing rates higher than 3.6%) with the solidity of a 2026 "hold" also in focus.

- The longer-run dot is broadly expected to remain at 3.0%. But once again with 10 at 3.00% or below and 9 above that level, it would only take 1 moving from 3.00% or below to above 3.00% to move the median higher, likely to 3.1%. That shift will happen at some point and it wouldn't be a shock to see it come this week.

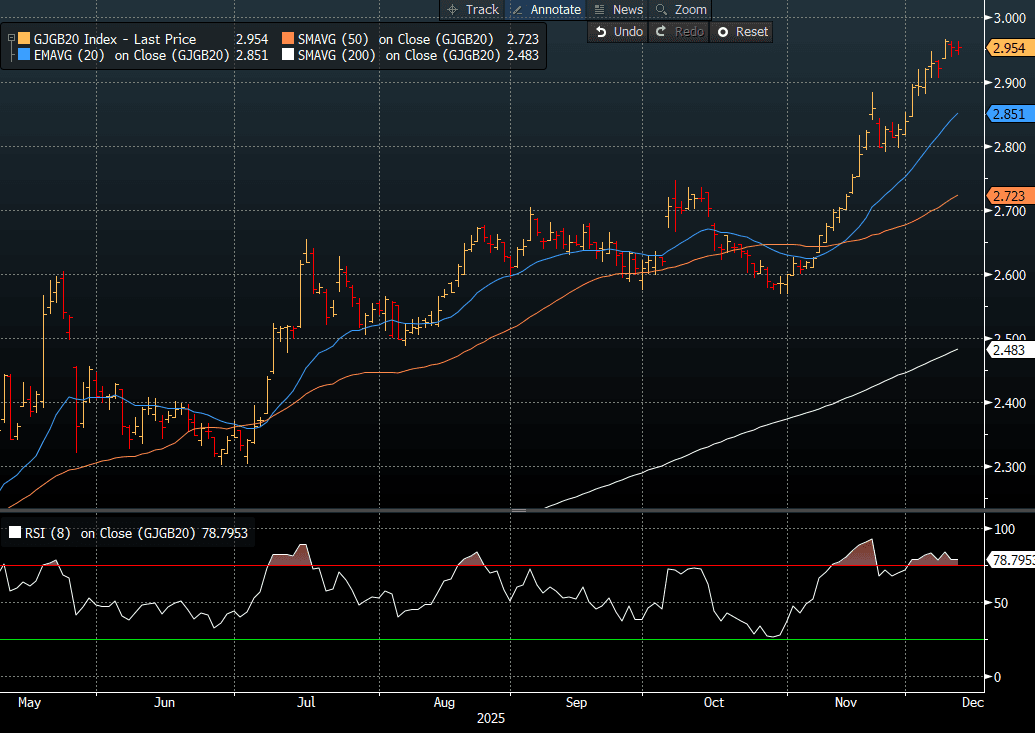

JGBS: Little Changed, PM: Econ Growth Vs Rising Yields, 20Y Supply Tomorrow

JGB futures are slightly weaker, -4 compared to settlement levels.

- PM Takaichi said Japan should prioritise economic growth rather than worry excessively about rising bond yields. She noted that yields reflect many factors, and it’s difficult to isolate the impact of fiscal policy. Takaichi emphasised that Japan’s debt-to-GDP ratio is gradually improving and highlighted the stability of the JGB market, supported by predominantly domestic ownership, while acknowledging potential risks if foreign ownership grows. – BBG

- She said rising yields have mixed effects on the economy, raising borrowing costs but also boosting household income. On currencies, she stressed the importance of stable, fundamentals-driven FX moves and said the government will act if market conditions become disorderly. - BBG

- Cash US tsys are ~1bp richer in today's Asia-Pac session ahead of today's FOMC policy decision. Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation.

- Cash JGBs are little changed across benchmarks out to the 40-year (+15.bps).

- Swap rates are 1-2bps higher, with a flattening bias.

- Tomorrow, the local calendar will see BSI Survey, International Investment Flow and Tokyo Avg Office Vacancies data alongside 20-year supply (see chart).

Source: Bloomberg Finance LP

AUSSIE BONDS: Post-RBA Sell-Off Extends Ahead Of Tomorrow's Jobs Data

ACGBs (YM -6.0 & XM -5.0) have extended the sell-off that started during yesterday's RBA presser by Governor Bullock. As it stands, futures are 6-10bps weaker, with a flatter curve.

- Cash US tsys are ~1bp richer in today's Asia-Pac session ahead of today's FOMC policy decision. Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +60bps.

- The bills strip has bear-steepened across contracts, with pricing flat to -6.

- RBA-dated OIS pricing is 1–8bps firmer across meetings today, extending yesterday’s post-press conference sell-off. Markets are pricing a steady build-up in tightening risk, with the implied probability of a 25bp hike rising from 36% in February to 97% by May and 219% by December 2026.

- The spread between the 1-year forward 3-month swap (1Y3M) and the 3-month rate—often used as a proxy for policy expectations a year ahead—has widened by more than 150bps since April, underscoring the magnitude of the shift in rate expectations (see chart).

- Tomorrow, the local calendar will see labour market data, with the market expecting +20k jobs but a higher unemployment rate (4.4% vs. 4.3% prior).

Figure 1: 1Y3M Swap Rate Vs. 3M Swap Rate

Source: Bloomberg Finance LP / MNI

AUSTRALIA: Nov Unemployment Rate Forecasts Split Between Rise & Unchanged

With the RBA saying this week that “recent data suggest the risks to inflation have tilted to the upside, but it will take a little longer to assess the persistence” and noting signs of capacity pressures, the data before the 4 February decision will be key to the policy outlook. This begins with Thursday’s November job figures.

- The RBA doesn’t just look at the headline employment and unemployment but also the underemployment & youth unemployment rates as well as hours worked. The split between full-time and part-time will also be important.

- Bloomberg consensus is forecasting a 20k rise in employment after October’s 42.2k. Forecasts range from 10-40k with most around 15-25k. Westpac is at consensus, while ANZ is below at +15k and CBA & NAB above at +25k.

- The series is volatile and can easily surprise in both directions but annual growth has slowed over 2025. Therefore it is important to look at the 3-month average, which RBA Governor Bullock has recommended. In October, the average was +15.1k.

- The unemployment rate is projected to rise 0.1pp to 4.4% but 9 analysts expect it to be stable at 4.3% with 15 forecasting 4.4%. Westpac is in line with consensus, while ANZ, CBA and NAB all expect it to remain at 4.3%.

- The participation rate is forecast to be unchanged at 67.0%.

STIR: Year-Ahead Expectations For RBA Have Shifted 150bps Since April

RBA-dated OIS pricing is 1–8bps firmer across meetings today, extending yesterday’s post-press conference sell-off.

- Relative to pre-RBNZ levels yesterday, pricing is now 5–13bps firmer, led by late-2026 meetings.

- Markets are pricing a steady build-up in tightening risk, with the implied probability of a 25bp hike rising from 38% in February to 102% by May and 205% by November 2026.

- The spread between the 1-year forward 3-month swap (1Y3M) and the 3-month rate—often used as a proxy for policy expectations a year ahead—has increased by more than 150bps since April, underscoring the magnitude of the shift in rate expectations.

Figure 1: 1Y3M Swap Rate Vs. 3M Swap Rate

Source: Bloomberg Finance LP / MNI

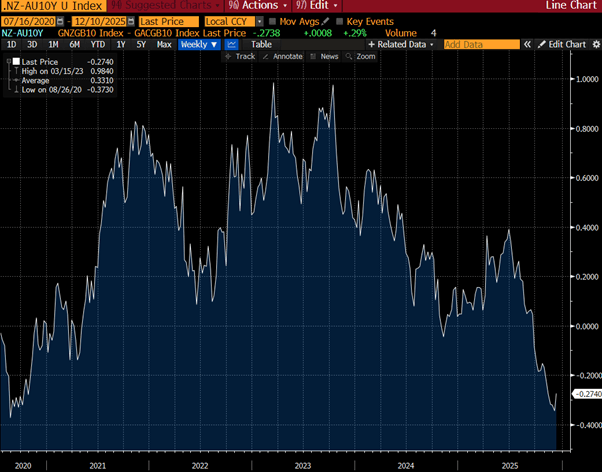

BONDS: NZGBS: Post-RBNZ Sell-Off Extends Further, 63bps Of Hikes In 2026

NZGBs closed 4-6bps cheaper across benchmarks.

- NZGBs showed a mixed relative performance: the NZ–US 10-year yield differential widened by 3bps, while the NZ–AU differential narrowed by 3bps. As the chart shows, the NZ–AU spread is now hovering near its lowest level since 2020.

- Cash US tsys are ~1bp richer in today's Asia-Pac session ahead of today's FOMC policy decision.

- RBNZ Governor Anna Breman said today that monetary policy has no preset path and will change if the inflation outlook shifts. She emphasised the importance of assessing new data ahead of the next meeting and noted that global developments will also factor into policy decisions.

- Swap rates closed 4-9bps higher, led by the 5-year.

- RBNZ-dated OIS pricing closed firmer across meetings. 1bp of tightening is priced for February, while November 2026 assigns 63bps of tightening.

- Tomorrow, the local calendar will see Mfg Activity Volume data.

- On Thursday, the NZ Treasury plans to sell NZ$175mn of the 4.50% May-30 bond, NZ$200mn of the 3.50% Apr-33 bond and NZ$75mn of the 5.00% May-54 bond.

Bloomberg Finance LP

FOREX: USD - BBDXY Well Supported Heading Into FOMC

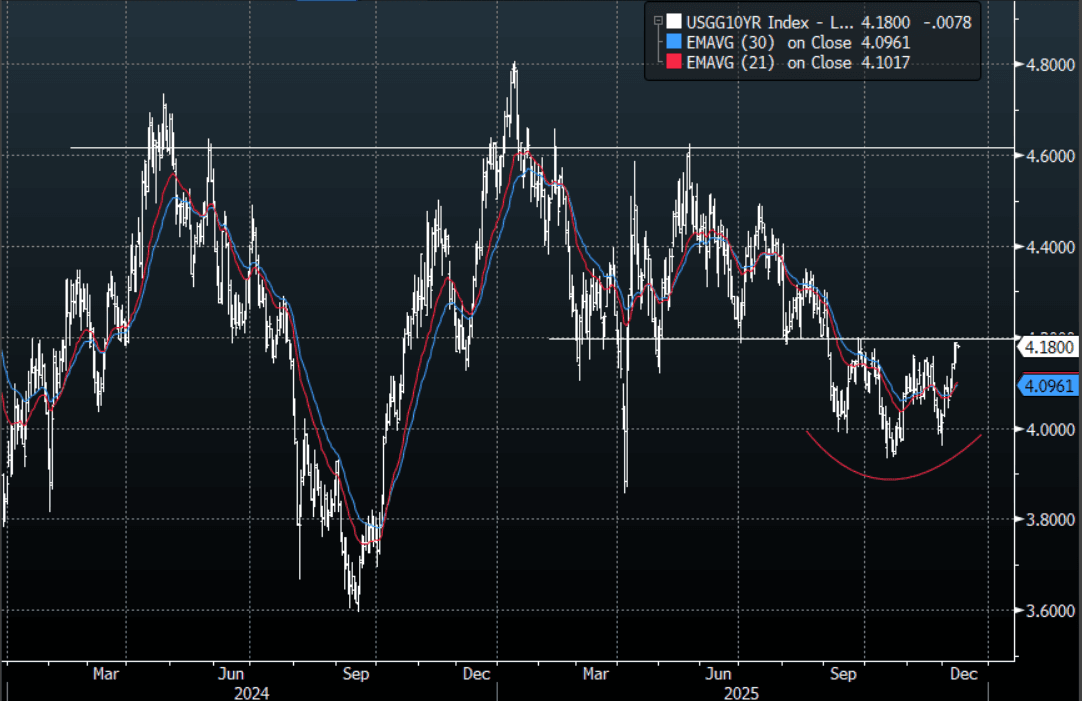

The BBDXY has had a range today of 1214.46 - 1215.08 in the Asia-Pac session; it is currently trading around 1214, -0.05%. The USD has traded sideways in a quiet Asian session. US yields continue to extend higher as we approach the FOMC, and both risk and the USD have begun to take notice. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1216-1218 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1221-1223. The US 10-year yield is approaching the pivotal 4.20% area so the FOMC will have a big say in whether this area breaks or caps yields going into the end of year. Which has direct implications for the fortunes of the USD.

- EUR/USD - Asian range 1.1622-1.1629, Asia is currently trading 1.1625. The pair continues to consolidate above the 1.1600 area. On the day, all eyes will be focused on the FOMC tomorrow morning, dips toward 1.1580-1600 should be supported initially, looking to retest the 1.1660-1680 area again eventually.

- GBP/USD - Asian range 1.3296-1.3305, Asia is currently dealing around 1.3305. The pair is consolidating around the 1.33 area. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3250-1.3280 area, while above here look for the market to test the 1.3350-80 area again at some point. FOMC will dictate which side is tested.

- Cross asset : SPX +0.02%, Gold $4205, US 10-Year 4.18%, BBDXY 1214, Crude Oil $58.35

- Data/Events : Italy Industrial Production MoM

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

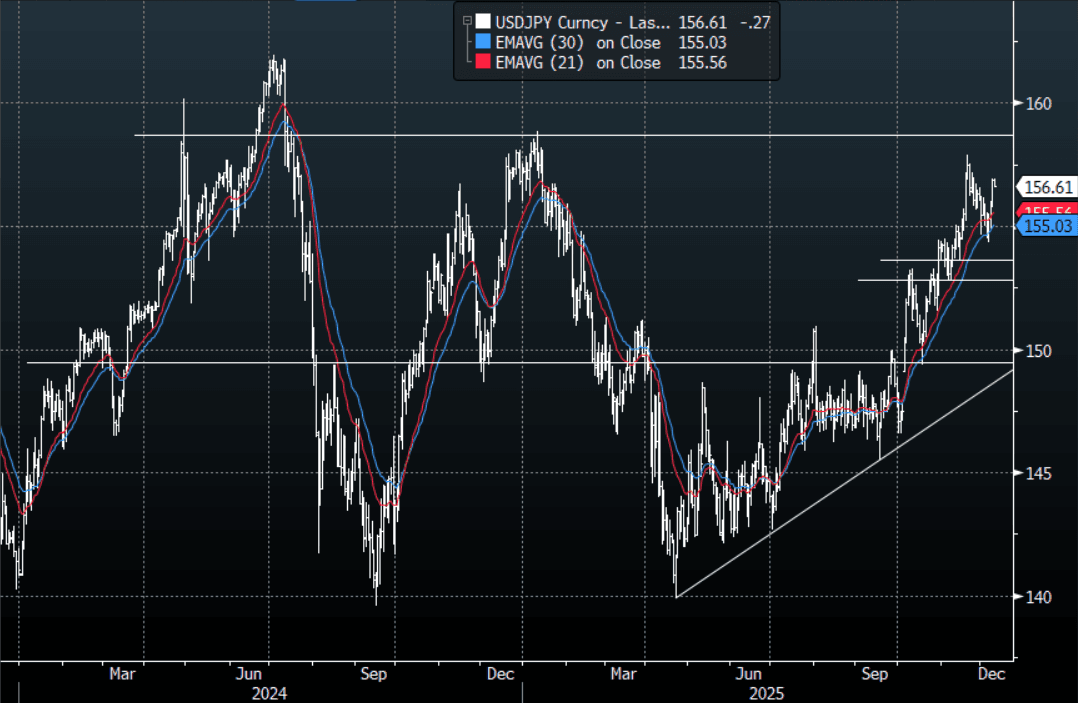

JPY: USD/JPY - Stalls Toward 157.00, Drifts Off Overnight Highs

The USD/JPY range today has been 156.56 - 156.94 in the Asia-Pac session, it is currently trading around 156.60, -0.20%. The pair has drifted lower in Asia after topping out towards 157.00. The move higher overnight was supported by the sell-off in treasuries which has seen yields move quite a bit higher as we approach the FOMC. The U.S. 10-Year yield is approaching the pivotal 4.20% area, a break of which could signal the start of a bigger move higher. The market has been pricing in the fact that the Yen move looks likely to force the BOJ into action in December. This has initially stalled the upward momentum but a hawkish cut from the FOMC tomorrow could potentially undo all that. Technically USD/JPY is in an uptrend, the first big support back toward the 153-155 area has held on very well upon first examination. On the day, look for support back toward 156.00-30, on the topside we should see some initial resistance around 157.00-30, a break above here and the next target is towards 158.00.

- Nick Timiraos on X: “Politico: Is it a litmus test that the new chair lowers interest rates immediately? Trump: Yes.”

- Jim Bianco on X: “As many as five of the 12 voting members of the Fed’s policy committee, and 10 of all 19 members, have signaled in speeches or public interviews that they didn’t see a strong case to cut.”

- "TAKAICHI: VITAL THAT FX MOVES STABLY, REFLECTING FUNDAMENTALS, WILL TAKE APPROPRIATE RESPONSE IF EXCESSIVE FX MOVES. WEAK YEN HAS BOTH MERITS AND DEMERITS FOR ECONOMY" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($592m), 156.00($900m). Upcoming Close Strikes : 155.00($1.13b Dec 12), 156.00($2.46b Dec 11), 159.00($1.55b Dec 12) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 94 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

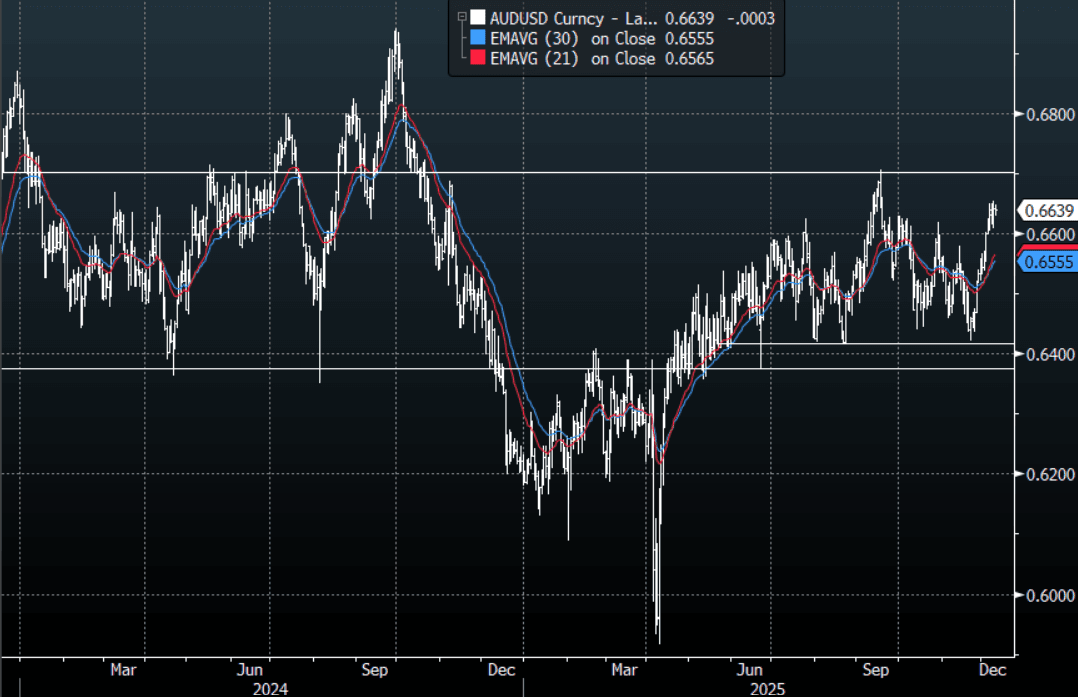

AUD/USD - Treading Water Just Below 0.6650

The AUD/USD has had a range today of 0.6629 - 0.6647 in the Asia- Pac session, it is currently trading around 0.6640, -0.05%. The AUD/USD has drifted lower today with risk on the backfoot in Asia ahead of the FOMC. US yields continue to rise, the 10-Year is approaching the pivotal 4.20% area as we come closer to the FOMC. The AUD price action remains very constructive and it continues to ignore the pullback in the USD for now. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, watch to see if price can continue to hold above 0.6620-0.6630 to rebuild momentum to have another look back toward the 0.6700 area at some point. If that support does not hold I suspect bids will return back towards the 0.6570-0.6600 area. The AUD outperformance is being expressed more clearly in the crosses.

- MNI AU - Nov Unemployment Rate Forecasts Split Between Rise & Unchanged: With the RBA saying this week that “recent data suggest the risks to inflation have tilted to the upside, but it will take a little longer to assess the persistence” and noting signs of capacity pressures, the data before the 4 February decision will be key to the policy outlook. This begins with Thursday’s November job figures. The RBA doesn’t just look at the headline employment and unemployment but also the underemployment & youth unemployment rates as well as hours worked. The split between full-time and part-time will also be important.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD822m). Upcoming Close Strikes : 0.6550(AUD1.59b Dec 11), 0.6650(AUD767m Dec 12) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

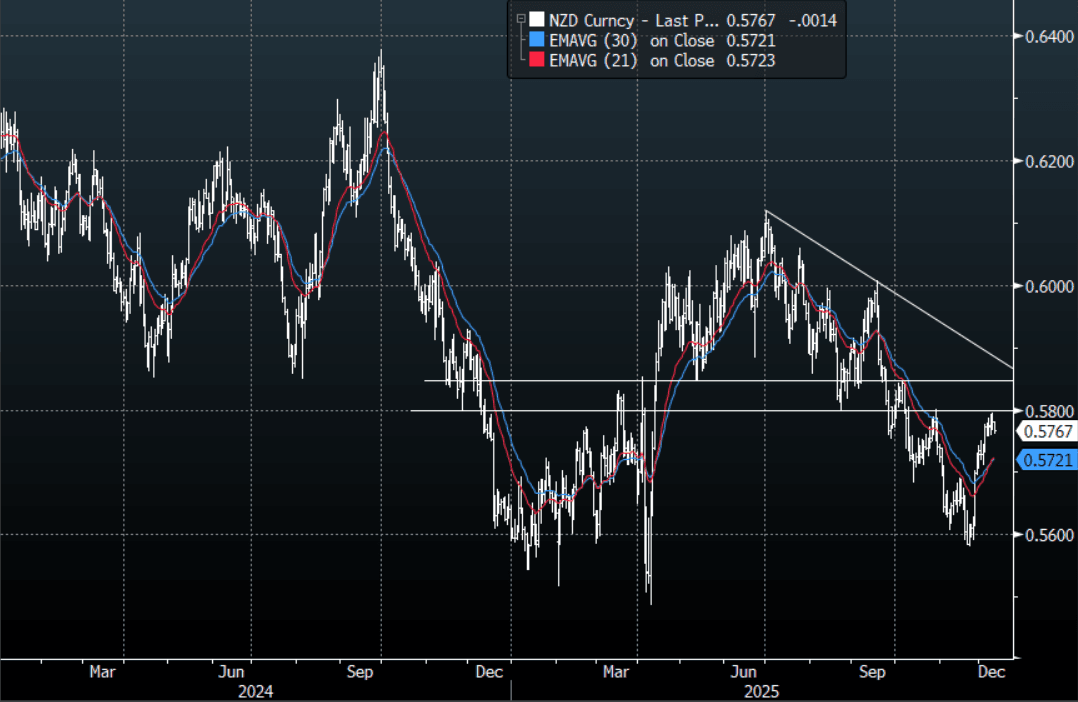

NZD/USD - Drifts Back Toward 0.5750 Heading Into FOMC

The NZD/USD had a range today of 0.5761-0.5782 in the Asia-Pac session, going into the London open trading around 0.5765, -0.30%. The NZD/USD has drifted lower in Asia after stalling overnight toward the 0.5800 area and for the first time it is potentially showing some signs of exhaustion with the USD rebounding as we approach the FOMC meeting. First support is around 0.5735-0.5755 area first up and then the more important 0.5670/0.5700 area.

- "NZ OCT. NET MIGRATION ESTIMATE +2,400" - BBG (Sep was 1760)

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD557m), 0.5800(NZD475m). Upcoming Close Strikes : 0.5700(NZD306m Dec 12) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 32 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

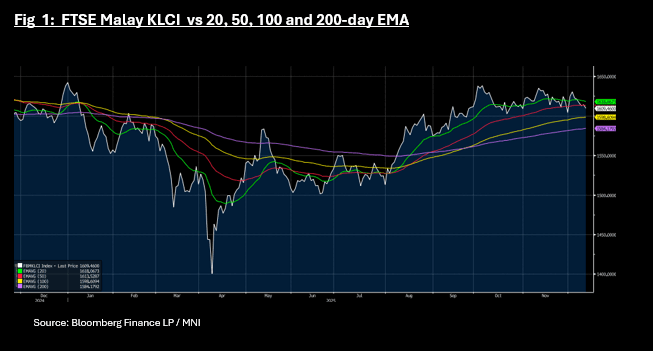

ASIA STOCKS: Pricing Pressures Weigh on China as Markets Wait for FOMC

Caution is evident in equity markets today ahead of the FOMC with the focus now on the forward pricing as rate cut expectations begin to diminish. In Japan, markets are agonizing over a potential Bank of Japan (BoJ) rate hike this month, following stronger-than-expected producer price data. This has influenced the Japanese yen and market dynamics, though rising yields are expected as a part of the normalization process. Whilst in China inflation remains weak even though it has hit near term highs. CPI at +0.7% was the strongest print in more than a year and a step towards easing deflationary fears but remain well below the 2% target. Producer pricing remained was negative again, having last printed positive in late 2022. The push pull of deflationary pressures is obvious, weighing heavy on China's stocks today.

- The NIKKEI couldn't shrug off the concerns on rates and is down -0.25% eating into modest gains for the first few days of trading.

- China's bourses are all down with onshore down marginally more than the HSI. HSI is lower by -0.43% and CSI 300 is down -0.85%

- The KOSPI seems to refuse to fall at the moment and is up over 5% in December alone. It is doing very little today hardly moving from where it started the day.

- The NIFTY 50 had two consecutive days of falls to start the week but has bounced back Wednesday morning to rise +0.35% after a strong IPO for an e-commerce stock

- Malaysia and Jakarta are moving in opposite directions with the FTSE Malay KLCI down -0.29% whilst the JCI is up +0.42%. The FTSE Malay KLCI has now traded below the 50-day EMA and at 1,609 has the 100-day EMA resistance below at 1,598.

OIL: A Hawkish Fed Would Be Seen As Negative For Oil Demand, EIA Data Out Later

Crude has held onto most of Tuesday’s losses during today’s APAC session as it range trades ahead of the Fed decision later. A rate cut is widely expected, which is positive for US energy demand, but a hawkish tone regarding the policy outlook would likely weigh on oil prices. The EIA data release today could also be a market mover.

- WTI is up 0.2% to $58.35/bbl off the intraday low of $58.27, while Brent is also 0.2% higher at $62.05/bbl after falling to $61.96. The USD index is little changed.

- The market focus has returned to demand/supply fundamentals and it will be monitoring Thursday’s IEA and OPEC reports closely after today’s Fed and EIA data.

- A record market surplus in 2026 has been forecast for some time and upward revisions will be watched closely, especially given increased OPEC and non-OPEC output and elevated levels of seaborne crude.

- Bloomberg reported that US oil inventories fell 4.8mn barrels last week, according to those familiar with the API data. Product stocks were higher with gasoline stocks up 7.0mn and distillate 1.0mn.

- Not only is the FOMC decision announced later on Wednesday but Q3 US employment costs and November budget data also print. The BoC also decides rates. ECB President Lagarde gives an interview on the future of the euro and dollar. The ECB’s Donnery and Machado also appear.

PRECIOUS METALS: Silver Continues Rally, Gold Waiting For Fed

Gold & silver have held onto Tuesday’s gains during Wednesday’s APAC trading ahead of the Fed decision later. They have received support from a widely expected rate cut but given the recent rally are vulnerable to a hawkish tone or a very close vote. The last decision was split three ways. The US dollar and yields are little changed as those markets also wait for the Fed outcome (see MNI Fed Preview).

- Silver is up 0.5% to $60.95/oz after reaching another new record high of $61.480, above resistance at $60.852. The tightness of the market, risk silver will face US tariffs, and its current momentum has attracted speculators driving its outperformance.

- Gold is slightly lower at $4205.4/oz off the intraday peak at $4218.85 and now close to the day’s low. It has been in a narrow range this month as it waits for direction from the outlook for the Fed in 2026.

- Given gold & silver are non-yield bearing, they are also finding support from expectations that the new Fed chair will be more dovish than Powell. National Economic Council Director Hassett, a front runner to take the position, said that he sees “plenty of room” to cut rates but would remain independent if he became the next FOMC head.

- Not only is the FOMC decision announced later on Wednesday but Q3 US employment costs and November budget data also print. The BoC also decides rates. ECB President Lagarde gives an interview on the future of the euro and dollar. The ECB’s Donnery and Machado also appear.

LNG: Low EU Prices Driving LNG Imports Elsewhere, US Weather Unwinds Dec Rise

US gas was sharply lower on Tuesday as forecasts for higher temperatures later in December drove the unwinding of last week’s 10% gain. Henry Hub fell 6.8% to $4.579, which is still elevated. In contrast, European prices rose 1.9% to EUR 27.375 as inventory drawdowns continue. Prices are still down 5% this month after falling 8.6% in November and the fall is discouraging LNG shipments to Europe, which drove Tuesday’s increase in gas.

- US prices could rise sharply if there is another cold snap, especially if it impacts gas production and transportation. Storage levels have been declining towards their 5-year average.

- European gas trended higher over Tuesday reaching EUR 27.700 before easing. Not only are LNG imports lower but there have been disruptions to flows from Norway with both driving storage levels down which were 0.5pp lower on Monday at 71.8% and 10pp below the seasonal average.

- A mild start to the heating season has helped inventories, which started lower than in 2024, but some models are signalling that there could be a shift colder across northern Europe in the next week, according to Bloomberg.

MNI EXCLUSIVE: China-German Trade

A German business leader in Beijing provides insight into China-German trade.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com

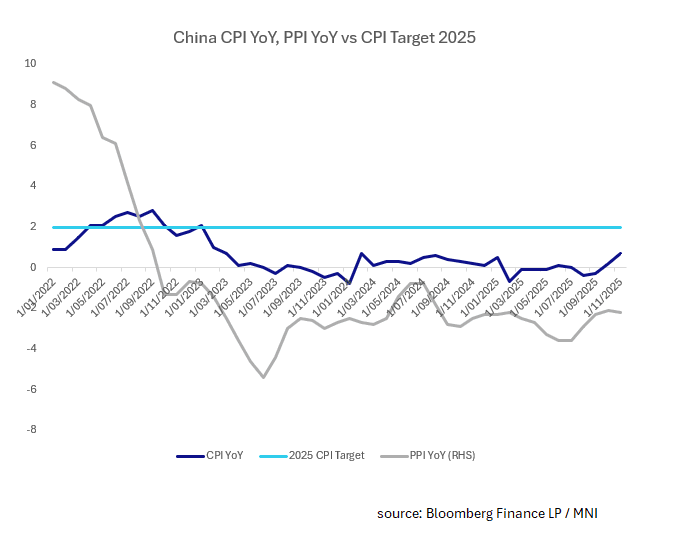

CHINA: PPI Declines More than Expected, Whilst CPI Rises

- October CPI climbed back to positive at +0.2% after 2 consecutive months of deflation and was in line with forecasts of a further increase to +0.7% in November, representing the highest reading since February 2024 with core rising +1.2%.

- PPI however is where deflationary pressures are most entrenched with forecasts for a -2.0% in November not met and PPI declined -2.2%.

- The anti-involution policies enacted to curb price wars seem likely to remain in place for some time with limited expectations for improvements in PPI.

- PPI has now printed negative each month since September 2022.

- Bond futures have edged higher this morning, post the injection during the OMO and the CPI.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/12/2025 | 0700/0800 | *** | CPI Norway | |

| 10/12/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/12/2025 | 0900/1000 | * | Industrial Production | |

| 10/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/12/2025 | 1000/1000 | Chancellor Reeves Testifies at TSC on Budget | ||

| 10/12/2025 | 1055/1155 | ECB Lagarde Interview on Currencies/Digital Euro | ||

| 10/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 10/12/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 10/12/2025 | - | *** | Money Supply | |

| 10/12/2025 | - | *** | Social Financing | |

| 10/12/2025 | - | *** | New Loans | |

| 10/12/2025 | 1330/0830 | *** | Employment Cost Index | |

| 10/12/2025 | 1445/0945 | *** | Bank of Canada Policy Decision | |

| 10/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/12/2025 | 1530/1030 | BOC press conference | ||

| 10/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 10/12/2025 | 1900/1400 | ** | Treasury Budget | |

| 10/12/2025 | 1900/1400 | *** | FOMC Statement | |

| 10/12/2025 | 1930/1430 | Fed Chair Powell Press Conference | ||

| 11/12/2025 | - | Swiss National Bank Meeting | ||

| 11/12/2025 | 0001/0001 | * | RICS House Prices | |

| 11/12/2025 | 0030/1130 | *** | Labor Force Survey | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0700/0800 | *** | Final Inflation Report | |

| 11/12/2025 | 0830/0930 | *** | SNB Interest Rate Decision | |

| 11/12/2025 | 0950/0950 | BOE Bailey Pre-recorded Chat on Financial Stability | ||

| 11/12/2025 | 1000/1000 | BOE Bailey Gives Evidence At Covid-19 Inquiry | ||

| 11/12/2025 | 1100/0600 | *** | Turkey Benchmark Rate |