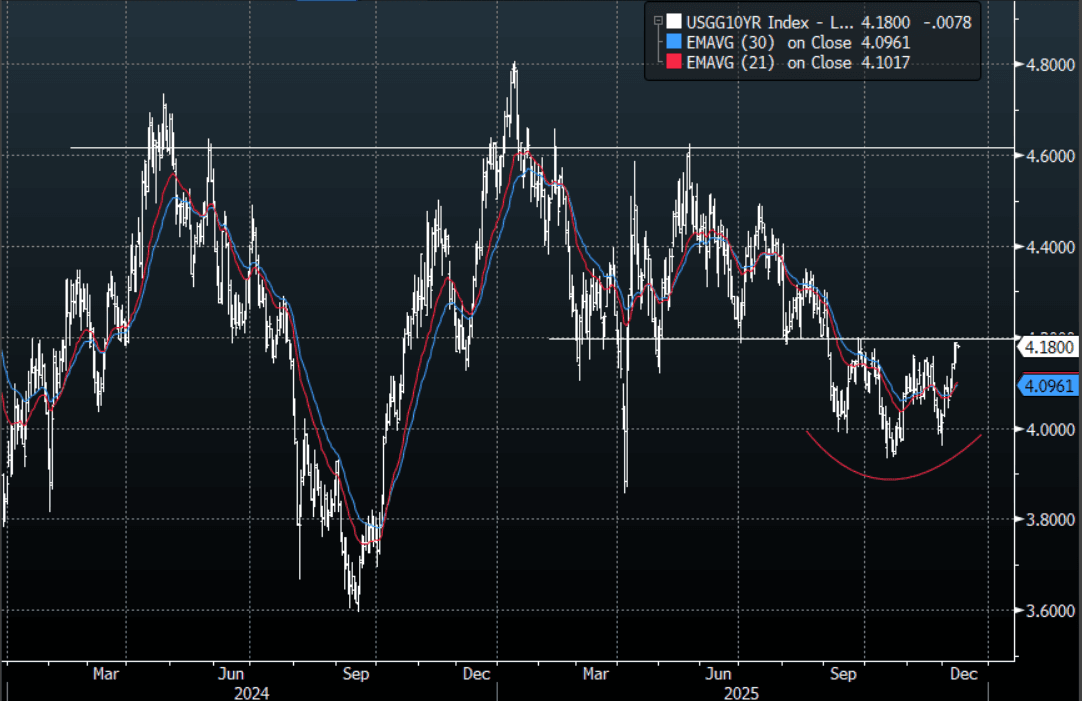

FOREX: USD - BBDXY Well Supported Heading Into FOMC

The BBDXY has had a range today of 1214.46 - 1215.08 in the Asia-Pac session; it is currently trading around 1214, -0.05%. The USD has traded sideways in a quiet Asian session. US yields continue to extend higher as we approach the FOMC, and both risk and the USD have begun to take notice. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1216-1218 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1221-1223. The US 10-year yield is approaching the pivotal 4.20% area so the FOMC will have a big say in whether this area breaks or caps yields going into the end of year. Which has direct implications for the fortunes of the USD.

- EUR/USD - Asian range 1.1622-1.1629, Asia is currently trading 1.1625. The pair continues to consolidate above the 1.1600 area. On the day, all eyes will be focused on the FOMC tomorrow morning, dips toward 1.1580-1600 should be supported initially, looking to retest the 1.1660-1680 area again eventually.

- GBP/USD - Asian range 1.3296-1.3305, Asia is currently dealing around 1.3305. The pair is consolidating around the 1.33 area. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3250-1.3280 area, while above here look for the market to test the 1.3350-80 area again at some point. FOMC will dictate which side is tested.

- Cross asset : SPX +0.02%, Gold $4205, US 10-Year 4.18%, BBDXY 1214, Crude Oil $58.35

- Data/Events : Italy Industrial Production MoM

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Bear-Steepener Ahead Of Tomorrow's 30Y Supply

JGB futures are weaker and near session lows, -20 compared to settlement levels.

- "JAPAN PM TAKAICHI: NOT RULING OUT SALES TAX CUT AS OPTION IN FUTURE, BUT IMMEDIATE PRIORITY IS TO COMPILE PACKAGE OF STEPS TO CUSHION BLOW FROM RISING COST OF LIVING, CHANGING SALES TAX RATE WOULD TAKE TIME, SO DECISION ON WHETHER TO DO SO WOULD NEED TO TAKE INTO ACCOUNT WAGE, INFLATION LEVELS AT THE TIME - [RTRS]"

- MNI: BOJ board members largely agreed on the need to raise the policy interest rate eventually but saw no urgency to act at the Oct 29-30 meeting, preferring to confirm sustained wage momentum and the firmness of underlying inflation, according to the summary of opinions released Monday.

- Cash US tsys are 3-4bps cheaper in today's Asia-Pac session after headlines that key US Senate Democrats will advance a GOP bill to end the government shutdown. Risk appetite is firmer.

- Cash JGBs have bear-steepened across benchmarks, with yields flat to 3bps higher. This leaves the 2/30 curve within its well-established range ahead of tomorrow’s 30-year supply. (see chart)

- The benchmark 30-year yield is 2.6bps higher at 3.13% versus the cycle high of 3.351%.

- Swap rates are 1-3bps higher.

- Tomorrow, the local calendar will see Trade balance and Bank Lending data alongside 30-year supply.

OIL: Positive Risk Sentiment Drives Oil Higher As US Shutdown May End Soon

News of an imminent end to the lengthy US government shutdown has boosted risk sentiment in Monday’s trading and thus helped to drive oil prices higher. The impasse was seen to be costly to the economy and would as a result weigh on energy demand. WTI is up 0.8% to $60.25/bbl, close to the intraday high, after falling to $59.74 early in the session. Brent is 0.7% higher at $64.08/bbl after falling to $63.60. Prices remain range bound as the market looks for new information.

- News from the US says that enough Democrats in the senate will vote to pass a bill to end the government shutdown which is in its sixth week.

- The US dollar is slightly higher while the S&P e-mini is up 0.7% and copper +1.6%.

- The market will monitor monthly reports closely this week for any deterioration in the excess supply situation. The IEA increased its 2026 surplus forecast in its October monthly report. It publishes updates on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November.

- The uncertain impact of additional sanctions against Russia has been providing a floor to oil prices. However, US President Trump has given Hungary a one year exemption from the US sanctions on Russia’s Rosneft and Lukoil, as “it’s very difficult for him [Hungarian PM Orban] to get the oil and gas from other areas”. According to Bloomberg, Hungary imports 90% of its oil from Russia.

NZD: Asia- Pac: NZD/USD Still Trades Heavy But Wary Of Positioning

The NZD/USD had a range today of 0.5616 - 0.5634 in the Asia-Pac session, going into the London open trading around 0.5630, +0.15%. A combination of what looks like the end of the US shutdown and better China Inflation data has seen the NZD start the week drifting back up off its lows. The NZD continues to trade heavy but it is prudent to be wary of what the reaction to the end of the US shutdown might look like. I am a little wary of positioning in the NZD market though I still suspect any decent bounce will again attract sellers. The first sell area on a pullback would be around 0.5750 and then the more pivotal 0.5850 area.

- "NZ'S PM LUXON WANTS BANKS TO PASS ON RBNZ RATE CUTS FASTER" - BBG

- Bloomberg reports the NZ Treasury says, “New Zealand Economic Recovery Still Emerging. New Zealand’s economy has more spare capacity than previously assumed while a broad-based recovery is still emerging, the Treasury Department says in its Fortnightly Economic Update.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5380(NZD460m Nov 13), 0.5600(NZD538m Nov12), 0.5800(NZD461m Nov 12) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P