ASIA STOCKS: Pricing Pressures Weigh on China as Markets Wait for FOMC

Caution is evident in equity markets today ahead of the FOMC with the focus now on the forward pricing as rate cut expectations begin to diminish. In Japan, markets are agonizing over a potential Bank of Japan (BoJ) rate hike this month, following stronger-than-expected producer price data. This has influenced the Japanese yen and market dynamics, though rising yields are expected as a part of the normalization process. Whilst in China inflation remains weak even though it has hit near term highs. CPI at +0.7% was the strongest print in more than a year and a step towards easing deflationary fears but remain well below the 2% target. Producer pricing remained was negative again, having last printed positive in late 2022. The push pull of deflationary pressures is obvious, weighing heavy on China's stocks today.

- The NIKKEI couldn't shrug off the concerns on rates and is down -0.25% eating into modest gains for the first few days of trading.

- China's bourses are all down with onshore down marginally more than the HSI. HSI is lower by -0.43% and CSI 300 is down -0.85%

- The KOSPI seems to refuse to fall at the moment and is up over 5% in December alone. It is doing very little today hardly moving from where it started the day.

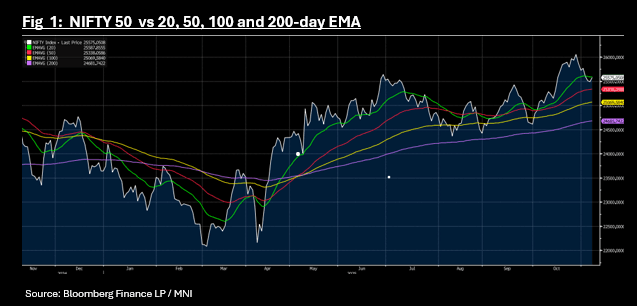

- The NIFTY 50 had two consecutive days of falls to start the week but has bounced back Wednesday morning to rise +0.35% after a strong IPO for an e-commerce stock

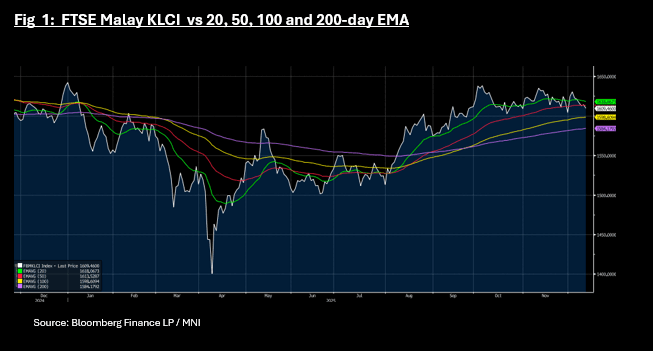

- Malaysia and Jakarta are moving in opposite directions with the FTSE Malay KLCI down -0.29% whilst the JCI is up +0.42%. The FTSE Malay KLCI has now traded below the 50-day EMA and at 1,609 has the 100-day EMA resistance below at 1,598.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Sell Off Gathers Pace in PM Trading on Shutdown Hopes

The sell off of US bonds continued into the afternoon, as bond futures all dipped. The US 10-Yr bond future is down -09 at 112-18+ and is at the mid-point below the 50-day EMA of 112-25+ and above the 100-day EMA of 112-12+.

Cash sold off as the US inches towards a resolution of the shutdown, with bonds wearing the brunt. A sharp sell off at the opening of cash trading slowed as the morning went on but gathered some pace after the lunch time break, with most maturities a further 0.5bps to 1.0bps higher in the afternoon alone.

- The 2-Yr is up +3.3bps to 3.597%

- The 5-Yr is up +3.8bps to 3.724%

- The 10-Yr is up at 4.136%, +3.7bps higher

- The 30-Yr is up +3.7bps to 4.738%.

The key auction tonight will b e a US$86bn 13-week and US$77bn 26-week bills auction. The key test will be the US$42bn 10-Yr on the 13th.

There is no scheduled Tier 1 data tonight, but markets will focus predominantly on the vote to end shutdown with news that enough Democrats in the senate will vote to pass a bill to end the impasse.

ASIA STOCKS: Tech Bounces Again, NIFTY 50 Nears Key Technical

The sell off in Asia's tech sector appears short lived as bell weather shares like SK Hynix in Korea, jump over 7% today. Last week's decline was the worst in over six months for the tech sector with many key names delivering record breaking gains. Last week's falls started in Wall Street and wasn't helped by warnings from the Korea exchange and is a reminder of stock bubbles of the past. Some key bourses in Asia (like the KOSPI and TAIEX) face concentration risk with the tech sector given their surge, as the sector's share of the index reaches new highs. Risk appetite returned today as it appears the US shutdown could be ending, with most major bourses higher today.

- The NIKKEI delivered gains of +0.93% to reach 50,755, just back from last week's high of 50,752 whilst the KOSPI rose almost 3.00% to reach a new recover more than half of last week's falls.

- In China the story was more mixed with the onshore offshore divide on show. The Hang Seng is up +0.61% whilst onshore bourses are all down modestly. The CSI 300 fell -0.24% to 4,667 but remains above the 20-day EMA of 4,639.

- The FTSE Malay KLCI is up +0.63% whilst the JCI in Indonesia +0.22%. Both retain their positions above all major moving averages.

- In India, as P/E's continue to look stretched and at year end forecasts, the NIFTY 50 fell modestly last week despite the turmoil elsewhere. The falls however took it below the 20-day EMA for the first time since September. The gains this morning takes it to 25,568, just below the 20-day EMA of 25,587.

FOREX: Asia-Pac FX: USD Drifts Higher In Asia On USD/JPY Move

The BBDXY has had a range today of 1219.55 - 1221.03 in the Asia-Pac session; it is currently trading around 1220, +0.10%. The USD opened stronger in Asia on reports the US shutdown might be ending, this saw risk and Yen-crosses gap higher on the open. The USD/JPY movement dominated the Asian session but I suspect the USD will be sold against risk currencies like the AUD & NZD and even the EUR into the London open should risk build on this initial reaction. Intra-day I suspect sellers should re-emerge back toward the 1223.50 area, the first real buy zone is back toward the 1215 area. Look for the USD to do some work and chop around within the 1215-1230 range. "SENATE HAS VOTES TO ADVANCE BILL TO END SHUTDOWN" - BBG

- EUR/USD - Asian range 1.1542 - 1.1562, Asia is currently trading 1.1550. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This has been the pivot with the larger 1.1400-1.1900 range over the past few months.

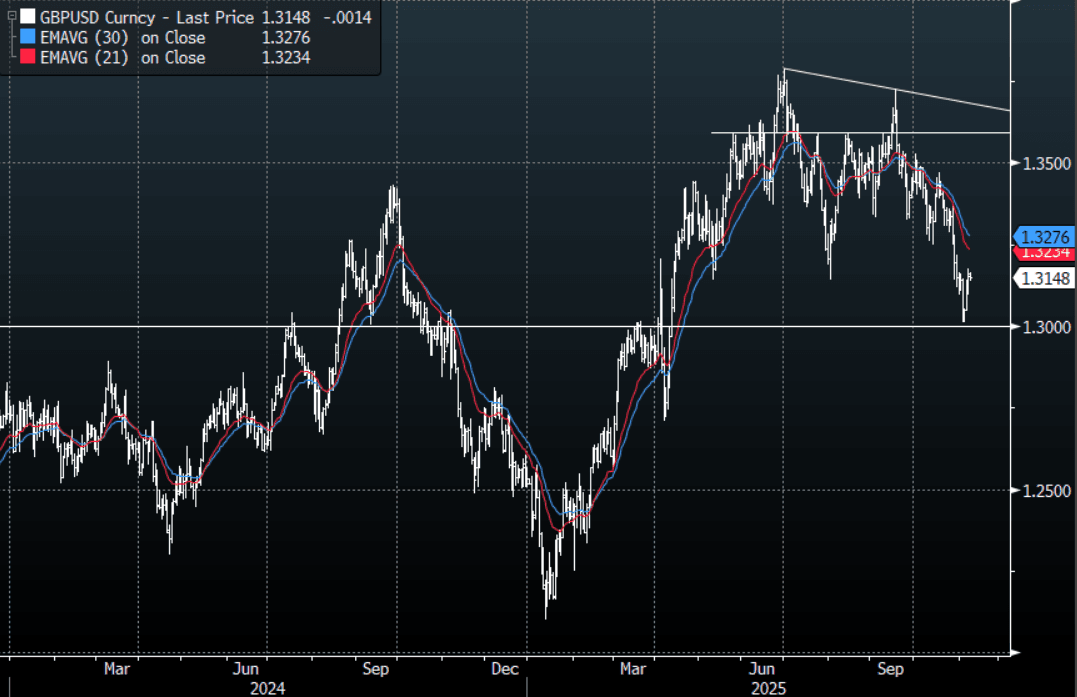

- GBP/USD - Asian range 1.3137 - 1.3164, Asia is currently dealing around 1.3145. The pair continues to build on its bounce off the 1.3000 area. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.70%, Gold $4050, US 10-Year 4.1340%, BBDXY 1220, Crude Oil $60.20

- Data/Events : EZ Sentix Investor Confidence

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P