US TSYS: FOMC Next, Eyes on the 2026 Outlook

US bond futures are flat to modestly better today in a low volume day. As markets await the FOMC decision the US-10-Yr opened with a modest bid tone to reach 112-04+ before falling back to where it started around 112-03+.

Cash was better bid with yields 0.5bp - 1.0bps lower across the curve with 5-Yr and 7-Yr the outperformers.

- The 2-Yr is down -0.8bps to 3.611%

- The 5-Yr is down -1.0bps to 3.78%

- The 10-yr is down -0.8bps to 4.182%

- The 30-Yr is down -0.7bps to 4.802

Tonight's auction will be a US$69 Bln 17-Week Bills.

SEP/Dot Plot: The lack of major data since the September projections round portends only limited changes to the macro and rate forecasts in the December edition out Wednesday.

- None of the rate dot medians are expected to change, with 2025 confirmed at 3.6% (though with an unusual amount of disagreement in the dot distribution for an end-year SEP in a form of "soft dissent" against the cut), 2026 at 3.4% (implying one 25bp cut), with 2027 at 3.1% (another 25bp cut).

- In short, we expect most of the attention to be on the rate distribution. For 2026, the September dots were closely poised between 3.4% and 3.1% (10 above 3.25% vs 9 below 3.25%). We don't see much change here but if anything the risks to the median skew to the downside. For example, if one member who put their dot at 3.4% in September also saw rates ending 2025 at 3.9%, they might mark-to-market the rate view one notch lower.

- We'll also be watching for any dots implying a 2026 hike (we would expect at least one seeing rates higher than 3.6%) with the solidity of a 2026 "hold" also in focus.

- The longer-run dot is broadly expected to remain at 3.0%. But once again with 10 at 3.00% or below and 9 above that level, it would only take 1 moving from 3.00% or below to above 3.00% to move the median higher, likely to 3.1%. That shift will happen at some point and it wouldn't be a shock to see it come this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

INDONESIA: October Consumer Sentiment Jumps Following BI Easing

October consumer confidence jumped 5.4% to 121.2, the highest in 6 months but in line with the same time last year. The index fell 1.9% q/q in Q3, pressured by social unrest and economic problems, with real consumption growth moderating slightly to 4.9% y/y from 5%. Sentiment at the start of Q4 suggests that spending could be around 5% again in the quarter possibly supported by the 75bp of easing in H2 2025 to date and an announced moderate fiscal easing in 2026.

- Confidence was supported in October by both economic conditions and expectations which rose 6.2% m/m and 4.8% respectively.

- Concerns over the labour market caused sentiment to decline over H2 and drive protests. This improved in October rising to its highest since May at 102.6 and expectations to 132.0 from 123.1 in September. Current incomes rose to 117.1 from 112.9 while the outlook improved 4.1 points to 138.4.

- Time to buy durable items jumped to 107.5 from 103.2 in September.

- Retail sales growth has held up but auto sales remain very weak. Tourist arrivals have been strong but are now slowing with September up 5.8% y/y after 12.2% y/y in August.

Indonesia economic outlook improves in October

Source: MNI - Market News/LSEG/Bloomberg Finance L.P.

US TSYS: Sell Off Gathers Pace in PM Trading on Shutdown Hopes

The sell off of US bonds continued into the afternoon, as bond futures all dipped. The US 10-Yr bond future is down -09 at 112-18+ and is at the mid-point below the 50-day EMA of 112-25+ and above the 100-day EMA of 112-12+.

Cash sold off as the US inches towards a resolution of the shutdown, with bonds wearing the brunt. A sharp sell off at the opening of cash trading slowed as the morning went on but gathered some pace after the lunch time break, with most maturities a further 0.5bps to 1.0bps higher in the afternoon alone.

- The 2-Yr is up +3.3bps to 3.597%

- The 5-Yr is up +3.8bps to 3.724%

- The 10-Yr is up at 4.136%, +3.7bps higher

- The 30-Yr is up +3.7bps to 4.738%.

The key auction tonight will b e a US$86bn 13-week and US$77bn 26-week bills auction. The key test will be the US$42bn 10-Yr on the 13th.

There is no scheduled Tier 1 data tonight, but markets will focus predominantly on the vote to end shutdown with news that enough Democrats in the senate will vote to pass a bill to end the impasse.

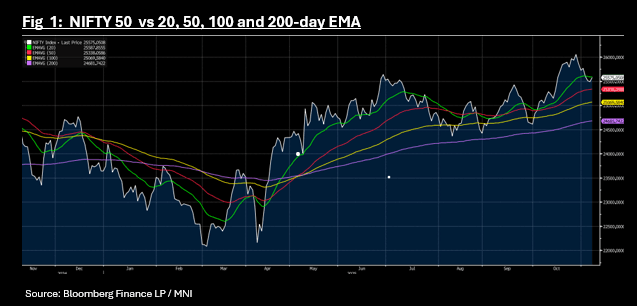

ASIA STOCKS: Tech Bounces Again, NIFTY 50 Nears Key Technical

The sell off in Asia's tech sector appears short lived as bell weather shares like SK Hynix in Korea, jump over 7% today. Last week's decline was the worst in over six months for the tech sector with many key names delivering record breaking gains. Last week's falls started in Wall Street and wasn't helped by warnings from the Korea exchange and is a reminder of stock bubbles of the past. Some key bourses in Asia (like the KOSPI and TAIEX) face concentration risk with the tech sector given their surge, as the sector's share of the index reaches new highs. Risk appetite returned today as it appears the US shutdown could be ending, with most major bourses higher today.

- The NIKKEI delivered gains of +0.93% to reach 50,755, just back from last week's high of 50,752 whilst the KOSPI rose almost 3.00% to reach a new recover more than half of last week's falls.

- In China the story was more mixed with the onshore offshore divide on show. The Hang Seng is up +0.61% whilst onshore bourses are all down modestly. The CSI 300 fell -0.24% to 4,667 but remains above the 20-day EMA of 4,639.

- The FTSE Malay KLCI is up +0.63% whilst the JCI in Indonesia +0.22%. Both retain their positions above all major moving averages.

- In India, as P/E's continue to look stretched and at year end forecasts, the NIFTY 50 fell modestly last week despite the turmoil elsewhere. The falls however took it below the 20-day EMA for the first time since September. The gains this morning takes it to 25,568, just below the 20-day EMA of 25,587.