PRECIOUS METALS: Silver Continues Rally, Gold Waiting For Fed

Dec-10 03:59

Gold & silver have held onto Tuesday’s gains during Wednesday’s APAC trading ahead of the Fed decision later. They have received support from a widely expected rate cut but given the recent rally are vulnerable to a hawkish tone or a very close vote. The last decision was split three ways. The US dollar and yields are little changed as those markets also wait for the Fed outcome (see MNI Fed Preview).

- Silver is up 0.5% to $60.95/oz after reaching another new record high of $61.480, above resistance at $60.852. The tightness of the market, risk silver will face US tariffs, and its current momentum has attracted speculators driving its outperformance.

- Gold is slightly lower at $4205.4/oz off the intraday peak at $4218.85 and now close to the day’s low. It has been in a narrow range this month as it waits for direction from the outlook for the Fed in 2026.

- Given gold & silver are non-yield bearing, they are also finding support from expectations that the new Fed chair will be more dovish than Powell. National Economic Council Director Hassett, a front runner to take the position, said that he sees “plenty of room” to cut rates but would remain independent if he became the next FOMC head.

- Not only is the FOMC decision announced later on Wednesday but Q3 US employment costs and November budget data also print. The BoC also decides rates. ECB President Lagarde gives an interview on the future of the euro and dollar. The ECB’s Donnery and Machado also appear.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Former BoJ Board Member Shares His Policy Rate Outlook

Nov-10 03:59

A former BOJ board member shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

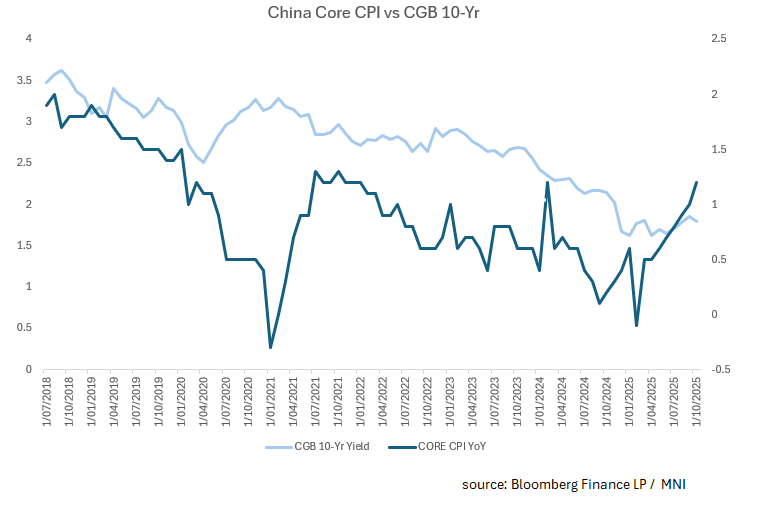

CHINA: Inflation to Lead Yields Higher?

Nov-10 03:15

- Following 5 consecutive day of significant liquidity withdrawal, the PBOC returned to injections this morning with bond futures barely reacting.

- The 10-Yr is flat at 108.475, above the 20-day EMA of 108.36

- The 2-Yr is flat at 102.46, at the mid-point between the 200-day EMA of 102.47and the 20-day EMA of 102.44.

- Bonds yields are steady with the CGB 10-Yr unchanged at 1.80%

- The withdrawal of liquidity over the last week, saw the 10-Yr break below 1.80% for several days with some suggestions being that the PBOC was seeking to set a new range of 1.70-1.80%.

- CGBs have been impervious to issuance this year thanks to the steady hand of the PBOC and looking for catalysts for the next move in bond yields has been difficult.

- Over the weekend, China released it's October CPI the YoY number inched up into +0.2% thanks to rises in Core. Core was up to +1.2% for its highest print since February 2024. When assessing the correlation with CGB yields, there appears a reasonable relationship with Core often leading bond yields higher.

- With mounting suggestions of more policy support given economic growth (for some forecasters) described as on weak footing, it would seem unpalatable for bond yields to gap higher from here. The issuance schedule at regional and federal level will remain elevated into 2026 and as asset allocation trends into equities from bonds grow, it is hard to see any allowance for bond yields to gap higher.

- If this relationship holds true, what this could predicate is an increased focus on liquidity injections over the remainder of 2025 with the aim of maintaining yields in tight, manageable ranges.

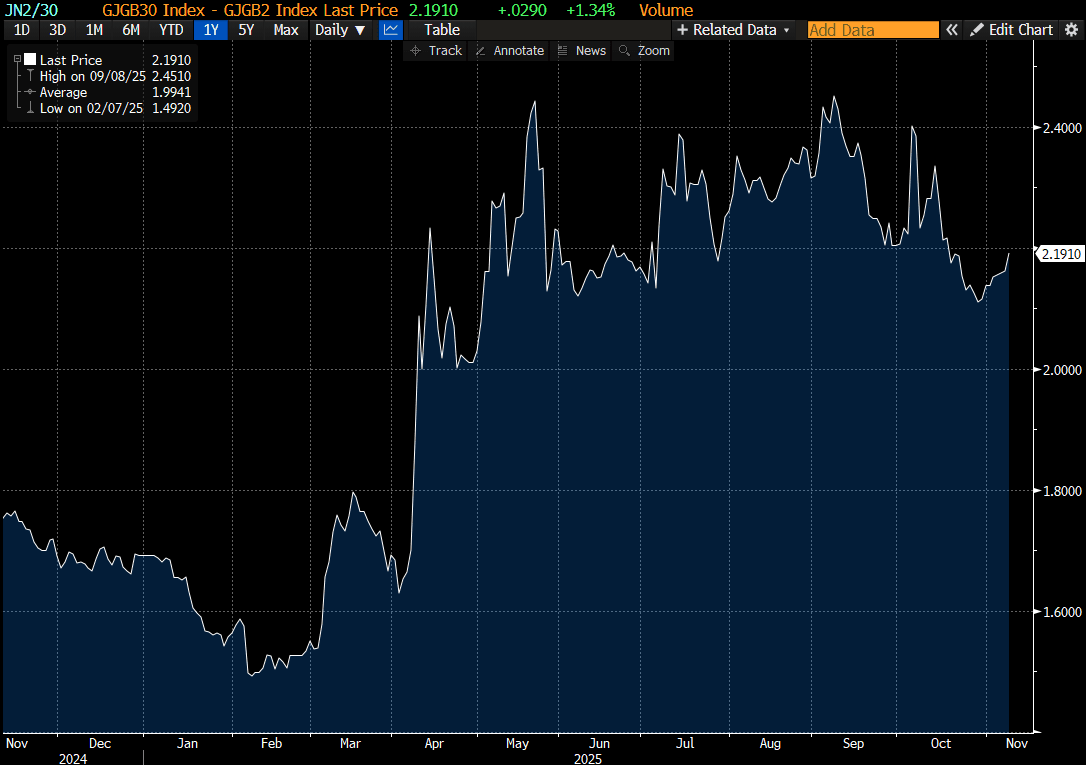

JGBS: Bear-Steepener At Lunch, 2/30 YC Holding Range

Nov-10 03:02

At the Tokyo lunch break, JGB futures are weaker, -20 compared to settlement levels, after today's BOJ SOO.

- MNI: BOJ board members largely agreed on the need to raise the policy interest rate eventually, but saw no urgency to act at the Oct 29-30 meeting, preferring to confirm sustained wage momentum and the firmness of underlying inflation, according to the summary of opinions released Monday.

- “Eight of 13 opinions called for a near-term hike or outlined conditions for one, suggesting the BOJ could lift rates in December or January if wage data remain solid and global conditions steady.” – MTN via BBG

- Cash US tsys are ~3bps cheaper in today's Asia-Pac session after headlines have crossed that key US Senate Democrats will advance a GOP bill to end the government shutdown. This follows earlier headlines from US Republican Senate leader Thune that a deal was coming together. Risk appetite is firmer, albeit away from best levels.

- Cash JGBs have bear-steepened across benchmarks, with yields flat to 3bps higher. This leaves the 2/30 curve within its well-established range. (see chart)

- The benchmark 10-year yield is 1.2bps higher at 1.693% versus the cycle high of 1.705%.

- Swap rates are 1-3bps higher.

Source: Bloomberg Finance LP