AUSTRALIA: Nov Unemployment Rate Forecasts Split Between Rise & Unchanged

With the RBA saying this week that “recent data suggest the risks to inflation have tilted to the upside, but it will take a little longer to assess the persistence” and noting signs of capacity pressures, the data before the 4 February decision will be key to the policy outlook. This begins with Thursday’s November job figures.

- The RBA doesn’t just look at the headline employment and unemployment but also the underemployment & youth unemployment rates as well as hours worked. The split between full-time and part-time will also be important.

- Bloomberg consensus is forecasting a 20k rise in employment after October’s 42.2k. Forecasts range from 10-40k with most around 15-25k. Westpac is at consensus, while ANZ is below at +15k and CBA & NAB above at +25k.

- The series is volatile and can easily surprise in both directions but annual growth has slowed over 2025. Therefore it is important to look at the 3-month average, which RBA Governor Bullock has recommended. In October, the average was +15.1k.

- The unemployment rate is projected to rise 0.1pp to 4.4% but 9 analysts expect it to be stable at 4.3% with 15 forecasting 4.4%. Westpac is in line with consensus, while ANZ, CBA and NAB all expect it to remain at 4.3%.

- The participation rate is forecast to be unchanged at 67.0%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

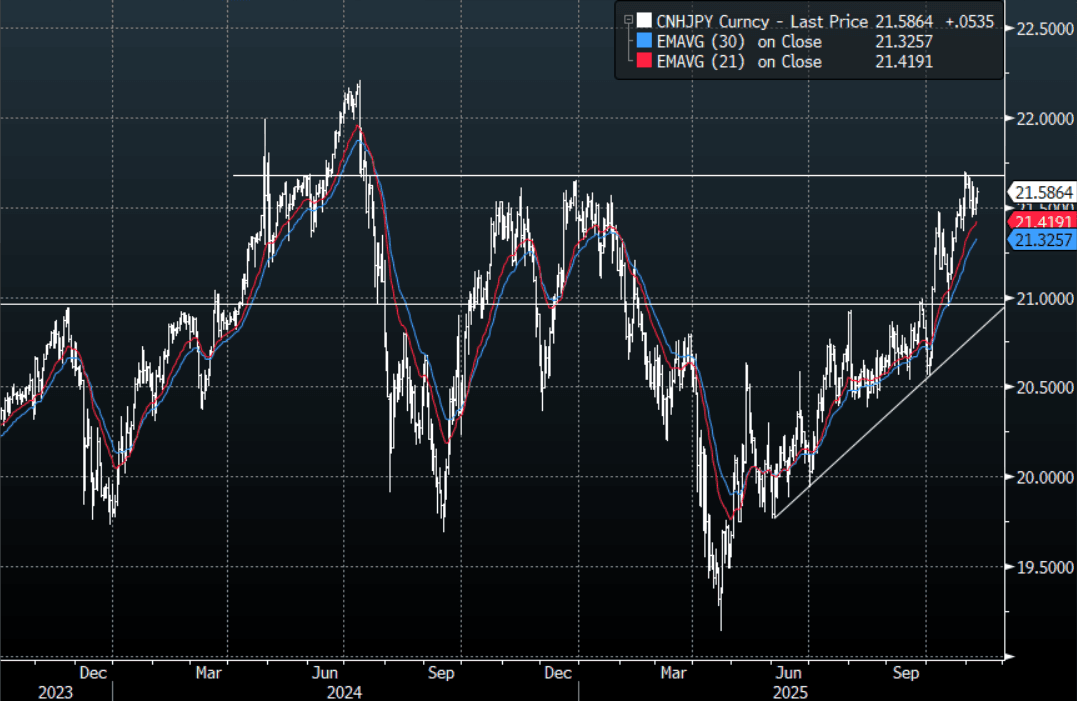

JPY: CNH/JPY - Bounces Off 21.40/45 Area, Looks Back Toward 21.70 Year Highs

The Friday night range was 21.4738 - 21.5519, Asia is currently trading around 21.5900. The pair has found some solid demand on the retracement back toward the 21.40/45 area. With risk taking a leg higher this morning as the market eyes a potential end to the US shutdown, Cross-Yen has reacted higher as you would expect. I thought the pullback in CNH/JPY would be a little deeper than that looking for a move back towards the 21.20-21.30 area. But With the 21.40 Area holding the focus should now return back to the 21.70/75 resistance area a break of which is needed to have a look toward the highs of 2024 seen around the 22.20 area.

Fig 1 : CNH/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

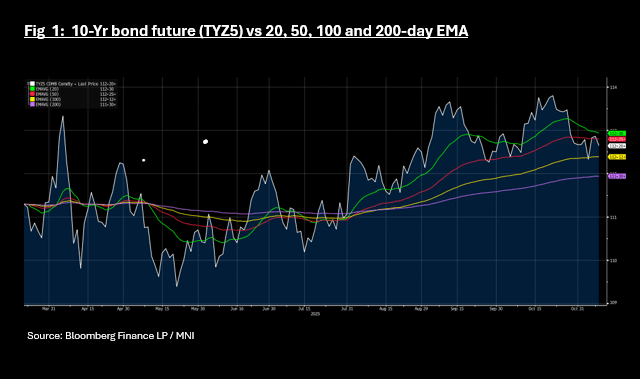

US TSYS: Weak Start to Trading for USTs; Potential Shutdown End Weighing Heavy

Bond are weak on the news that the government shutdown may be ending, with yields up across the curve at the opening of cash trading in Asia.

Bonds future are weak with TYZ5 down -07+ at 112-20+, unable to hold above the 50-day EMA and back below. The 100-day EMA is below at 112-12+. Volumes are low at this stage, potentially exacerbating the move.

Cash is seeing yields higher by 2.5 - 3.0bps across the curve in a fairly uniformed move, though like futures, volumes are low.

- The 2-Yr is up +2.7bps to 3.591%

- The 5-Yr is up +3bps to 3.715%

- The 10-Yr is up at 4.128%, +3bps higher

- The 30-Yr is up +2.6bps to 4.727%

JGBS: Modest Bear-Steepener After BOJ SOO & HLs On Ending US Shutdown

In Tokyo morning trade, JGB futures are weaker, -20 compared to settlement levels, after today’s BOJ SOO.

- MNI: BOJ board members largely agreed on the need to raise the policy interest rate eventually, but saw no urgency to act at the Oct 29-30 meeting, preferring to confirm sustained wage momentum and the firmness of underlying inflation, according to the summary of opinions released Monday.

- “The momentum of initial moves toward next year's annual spring labour-management wage negotiations will be an important factor for the Bank to consider in making policy decisions,” one member said at the meeting, which resulted in a pause to the 0.5% policy rate.

- Cash US tsys are ~3bps cheaper in today's Asia-Pac session after headlines have crossed that key US Senate Democrats will advance a GOP bill to end the government shutdown. This follows earlier headlines from US Republican Senate leader Thune that a deal was coming together. Risk appetite is firmer, albeit away from best levels.

- Cash JGBs have bear-steepened across benchmarks, with yields flat to 2bps higher. The benchmark 10-year yield is 1.4bps higher at 1.695% versus the cycle high of 1.705%. (see chart)

- Swap rates are 1-3bps higher.

Source: Bloomberg Finance LP