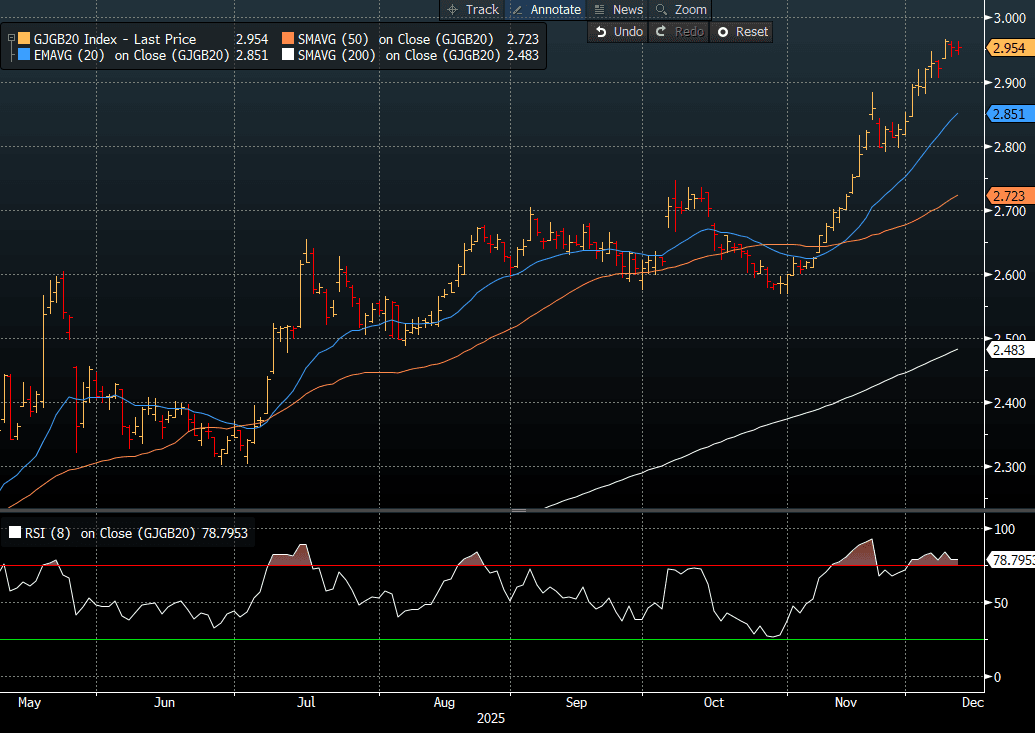

JGBS: Little Changed, PM: Econ Growth Vs Rising Yields, 20Y Supply Tomorrow

JGB futures are slightly weaker, -4 compared to settlement levels.

- PM Takaichi said Japan should prioritise economic growth rather than worry excessively about rising bond yields. She noted that yields reflect many factors, and it’s difficult to isolate the impact of fiscal policy. Takaichi emphasised that Japan’s debt-to-GDP ratio is gradually improving and highlighted the stability of the JGB market, supported by predominantly domestic ownership, while acknowledging potential risks if foreign ownership grows. – BBG

- She said rising yields have mixed effects on the economy, raising borrowing costs but also boosting household income. On currencies, she stressed the importance of stable, fundamentals-driven FX moves and said the government will act if market conditions become disorderly. - BBG

- Cash US tsys are ~1bp richer in today's Asia-Pac session ahead of today's FOMC policy decision. Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation.

- Cash JGBs are little changed across benchmarks out to the 40-year (+15.bps).

- Swap rates are 1-2bps higher, with a flattening bias.

- Tomorrow, the local calendar will see BSI Survey, International Investment Flow and Tokyo Avg Office Vacancies data alongside 20-year supply (see chart).

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Positive Risk Sentiment Drives Oil Higher As US Shutdown May End Soon

News of an imminent end to the lengthy US government shutdown has boosted risk sentiment in Monday’s trading and thus helped to drive oil prices higher. The impasse was seen to be costly to the economy and would as a result weigh on energy demand. WTI is up 0.8% to $60.25/bbl, close to the intraday high, after falling to $59.74 early in the session. Brent is 0.7% higher at $64.08/bbl after falling to $63.60. Prices remain range bound as the market looks for new information.

- News from the US says that enough Democrats in the senate will vote to pass a bill to end the government shutdown which is in its sixth week.

- The US dollar is slightly higher while the S&P e-mini is up 0.7% and copper +1.6%.

- The market will monitor monthly reports closely this week for any deterioration in the excess supply situation. The IEA increased its 2026 surplus forecast in its October monthly report. It publishes updates on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November.

- The uncertain impact of additional sanctions against Russia has been providing a floor to oil prices. However, US President Trump has given Hungary a one year exemption from the US sanctions on Russia’s Rosneft and Lukoil, as “it’s very difficult for him [Hungarian PM Orban] to get the oil and gas from other areas”. According to Bloomberg, Hungary imports 90% of its oil from Russia.

NZD: Asia- Pac: NZD/USD Still Trades Heavy But Wary Of Positioning

The NZD/USD had a range today of 0.5616 - 0.5634 in the Asia-Pac session, going into the London open trading around 0.5630, +0.15%. A combination of what looks like the end of the US shutdown and better China Inflation data has seen the NZD start the week drifting back up off its lows. The NZD continues to trade heavy but it is prudent to be wary of what the reaction to the end of the US shutdown might look like. I am a little wary of positioning in the NZD market though I still suspect any decent bounce will again attract sellers. The first sell area on a pullback would be around 0.5750 and then the more pivotal 0.5850 area.

- "NZ'S PM LUXON WANTS BANKS TO PASS ON RBNZ RATE CUTS FASTER" - BBG

- Bloomberg reports the NZ Treasury says, “New Zealand Economic Recovery Still Emerging. New Zealand’s economy has more spare capacity than previously assumed while a broad-based recovery is still emerging, the Treasury Department says in its Fortnightly Economic Update.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5380(NZD460m Nov 13), 0.5600(NZD538m Nov12), 0.5800(NZD461m Nov 12) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Cheaper With YM1 Testing Support

ACGBs (YM -5.0 & XM -5.0) are weaker with US tsys after headlines that key US Senate Democrats will advance a GOP bill to end the government shutdown. Risk appetite is firmer.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +26bps.

- The bills strip has bear-steepened, with pricing -2 to -5.

- The main takeaway from RBA Deputy Governor Hauser's Q&A today was that the economy could already be close to trend growth, and therefore, supply constraints make further rate cuts difficult.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 8% probability, with a cumulative 16bps of easing priced by mid-2026.

- Tomorrow, the local calendar will see Westpac Consumer and NAB Business Confidence data.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report. YM1 is currently testing horizontal support at 96.28 (see chart).

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond on Wednesday and A$800mn of the 1.75% 21 November 2032 bond on Friday.

Bloomberg Finance LP