MNI EUROPEAN MARKETS ANALYSIS: 80% Chance Dec BOJ Hike

- When asked about the merits of a rate increase and the likelihood of a move this month, Ueda did not shy away from discussing specifics — including the probability of a hike — during the press conference. BOJ-dated OIS currently assigns an 80% probability to a 25bp hike in December, rising to 99% by March 2026.

- Later US November Challenger job cuts and 29 November jobless claims after Wednesday's disappointing November ADP employment. Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Australia's October household spending is another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. This strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision given that inflation is above 3%.

MARKETS

US TSYS: Cheaper Ahead Of Today's Batch Of Labour Market Data

TYZ5 is dealing at 113-01+, -0-05+ from closing levels in today's Asia-Pac session.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- US tsys gained yesterday after fresh data showing weakness in the US labour market supported wagers that the Federal Reserve will deliver a third straight interest-rate cut at its final meeting of the year.

- “For a Fed that is now focused on the employment mandate, the November jobs data is troubling and consistent with a 25 bp rate cut next week,” Ian Lyngen, head of US rates strategy at BMO Capital Markets, wrote. – via BBG

- Thursday US Data Calendar: Challenger Job Cuts, Weekly Claims & Regional Fed Data.

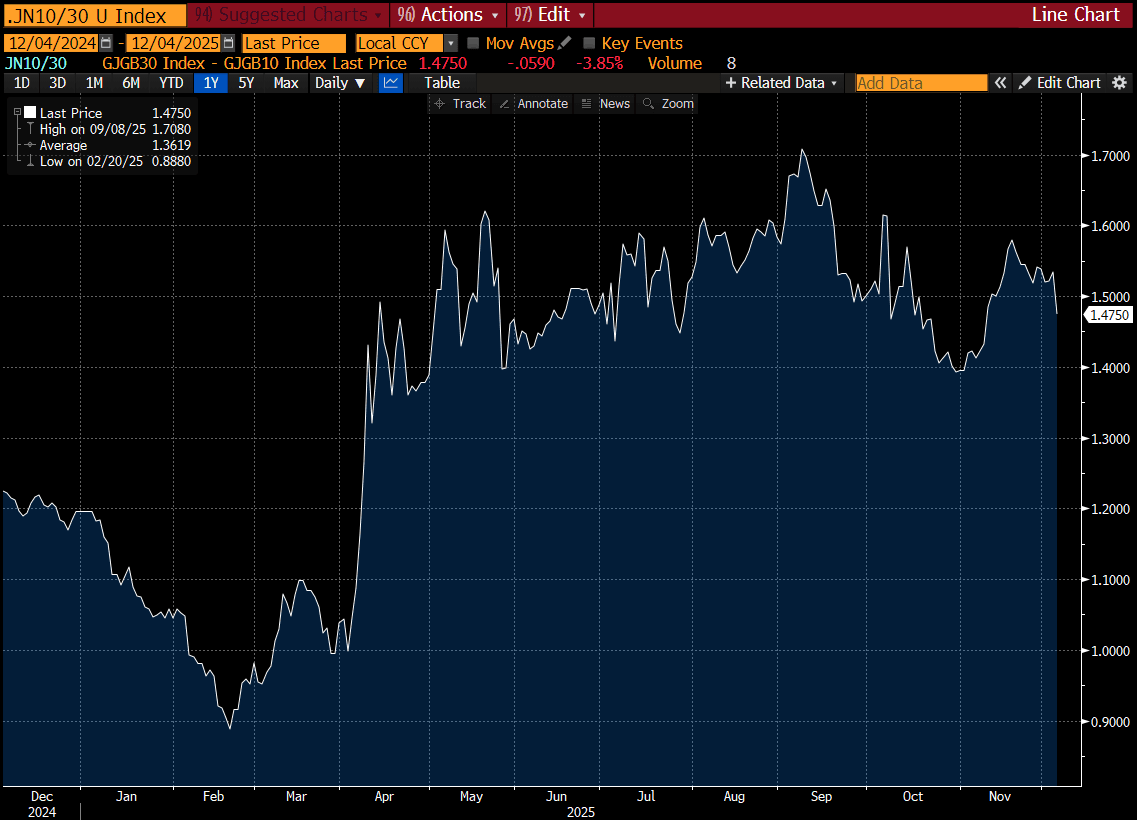

JGBS: 10YY Up But 30YY Down, BOJ Ueda: Fiscal Stimulus To Boost UCPI

JGB futures are back near session lows, -20 compared to settlement levels, after quickly reversing the spike higher following today’s 30-year auction result.

- The 30-year JGB auction delivered strong results. The low price exceeded dealer expectations of 96.40 (Bloomberg survey), the cover ratio jumped to 4.0445x—the highest since 2019—from 3.1248x, and the auction tail narrowed sharply to 0.09 from 0.27, all pointing to firmer bidding.

- MNI - BOJ Governor Kazuo Ueda said on Thursday that the government’s economic stimulus package will have a positive impact on economic growth and boost underlying inflation. Ueda told lawmakers that the stimulus package, mainly countermeasures to cope with high prices, will lower headline CPI, but it will exert upward pressure on underlying inflation through economic growth. However, he could not comment on the degree of the impact.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are mixed across benchmarks, with the 10-year underperforming (+2.6bps) and the 30-year outperforming (-3.2bps) (see chart).

- Swap rates are flat to 3bps higher.

- Tomorrow, the local calendar will see Household Spending and the Coincident/Leading Index data.

Source: Bloomberg Finance LP

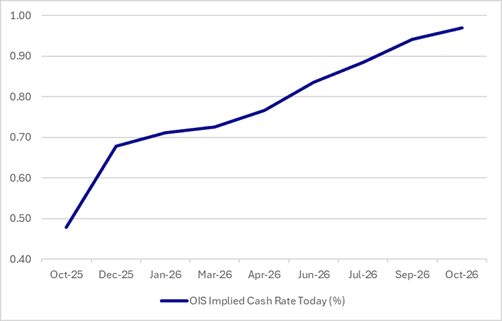

STIR: BoJ Hike 80% Priced By Dec With Two By October 2026

Bank of Japan Governor Kazuo Ueda said on Monday that even if the policy rate were raised to 0.75% from 0.50%, overall financial conditions would remain accommodative.

- When asked about the merits of a rate increase and the likelihood of a move this month, Ueda did not shy away from discussing specifics — including the probability of a hike — during the press conference.

- BOJ-dated OIS currently assigns an 80% probability to a 25bp hike in December, rising to 99% by March 2026. As recently as 21 November, markets saw less than a 20% chance of a December move.

- Notably, investors are now pricing in two 25bp hikes by October 2026.

Figure 1: BoJ-Dated OIS – Today

Source: Bloomberg Finance LP / MNI

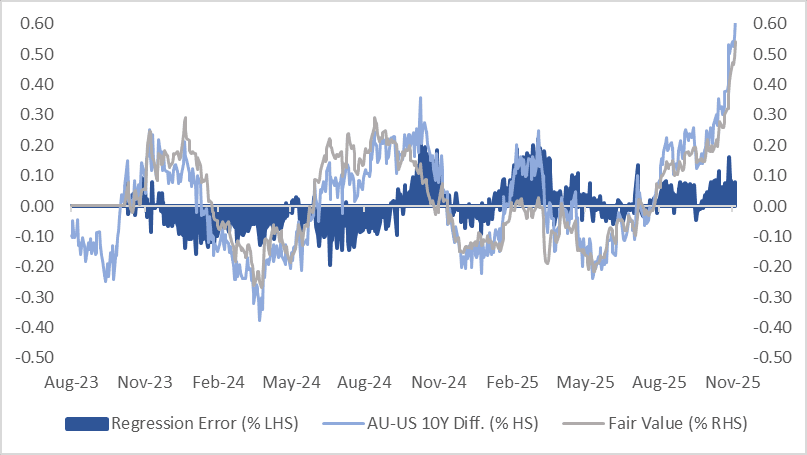

AUSSIE BONDS: AU-US 10Y Diff Keeps Pushing Wider, HH Spend Signals Robust Demand

ACGBs (YM -6.0 & XM -4.0) are weaker, hovering near session cheaps.

- October household spending is another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. With Governor Bullock saying yesterday that the output gap has likely closed, this strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision, given that inflation is above the top of the band.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after yesterday’s modest rally.

- Cash ACGBs are 4-6bps cheaper with the AU-US 10-year yield differential at +61bps, the highest since mid-2022. However, a simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is around 8bps too wide relative to fair value (see chart).

- The bills strip is -2 to -11 across contracts, with late whites underperforming.

- RBA-dated OIS pricing is showing a 25bp rate hike in December at a 3% probability, with 32bps tightening by December 2026.

- Tomorrow, the local calendar will see Foreign Reserves data.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Bloomberg Finance LP

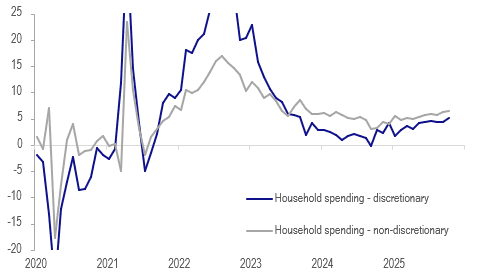

AUSTRALIA DATA: Consumer Recovery In Place, RBA On Hold

October household spending is another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. With Governor Bullock saying yesterday that the output gap has likely closed, this strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision given that inflation is above the top of the band.

- Spending rose 1.3% m/m, highest since January 2024, to be up 5.6% y/y, fastest since September 2023 and up from the previous month’s 5.1% y/y. The increase was broad-based across Australia.

- While both discretionary and non-discretionary spending were higher on the month, the former rose 1.6% m/m to be up 5.1% y/y after 4.5%.

- Expenditure on goods rose 1.7% m/m to be up 4.9% y/y after September’s 3.5% y/y driven by discounting ahead of November’s Cyber Week sales. There could be payback when promotions finish. Clothing & footwear jumped 3.5% m/m and household items +3.0%.

- Services rose 0.8% m/m and 6.4% y/y due to large concerts and festivals.

Australia household consumption y/y%

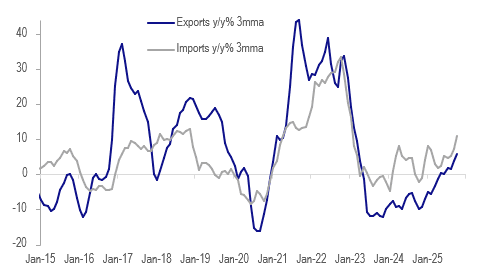

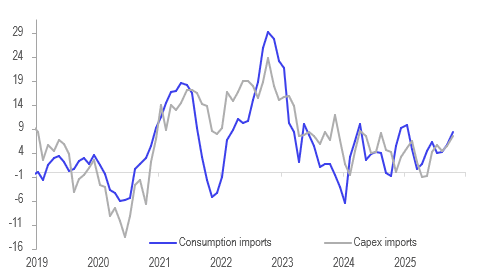

AUSTRALIA DATA: Higher Gold Prices Supportive But Imports & Exports Rising

The October merchandise trade surplus widened to $4.385bn after a downwardly-revised $3.71bn but it remains in the range it has been in since the start of 2024. The move was driven by monthly export growth exceeding imports for the second consecutive month and both are showing upward momentum. Stronger exports add to activity while imports signal that domestic demand is robust. The RBA is likely to be on hold beyond the 9 December decision.

Australia goods exports vs imports y/y% 3-mth ma

- Goods export values rose 3.4% m/m in October to be up 11.3% y/y after 9.8% y/y. Both rural and non-rural were higher on the month but annual growth is very different at 22.1% y/y and 2.7% y/y respectively.

- Non-monetary gold was the main driver of the rise in both export and import values in October as global prices rose 10.6% m/m to be up 50.8% y/y.

- Consumer goods imports rose 1.6% m/m to be up 7.9% y/y driven by increases in food & beverages, clothing & footwear and other goods.

- There was some payback in October for strong capex imports with them falling 5.5% m/m driven by a 30% drop in ADP equipment but telecoms rose 3.9% m/m and machinery & equipment +6.8%.

Australia merchandise imports y/y% 3-mth ma

- Goods exports to the US are moderating towards the 2024 average but are still up 15.8% y/y due to frontloading earlier in the year ahead of the introduction of US tariffs. Growth to China, Korea and India remains strong while it is still soft to Japan, Taiwan and has moderated to the UK and Indonesia.

- Metal ore shipments rose in October but coal & metals fell. Volumes were higher for iron ore, LNG and hard-coking & semi-soft coal. Prices were also generally higher, except for LNG.

BONDS: NZGBS: Slightly Richer Today But 5Y Remains Cheap In The Fly

NZGBs closed flat to 2bps richer, with the 5-year outperforming. Nevertheless, yields remain 12-24bps higher than last week's pre-RBNZ levels, with the 5-year the underperformer.

- Indeed, on a relative value basis, the 5-year swap is at its cheapest valuation since mid-2022, based on the 2-/5-/10-year butterfly spread (see chart).

- Today’s weekly supply delivered mixed results, with cover ranging from 2.72x (May-35) to 5.23x (May-51).

- On a relative basis versus its $-bloc counterparts, NZGBs also had a good day, with the NZ-US and NZ-AU 10-year yield differentials 1bp and 4bps lower, respectively.

- “New Zealand residential building rebounded in the third quarter, with the volume of residential building work rising 2.8% from the second quarter. The rebound in construction follows a pick up in third-quarter retail sales and exports, suggesting gross domestic product is recovering after a contraction in the second quarter.” - BBG

- RBNZ-dated OIS pricing closed little changed across meetings. 1bps of easing is priced for February, while November 2026 assigns 30bps of tightening.

- The local calendar will be empty until next Wednesday, when RBNZ Governor Breman hosts a media Q+A alongside Net Migration data.

Bloomberg Finance LP

Bloomberg Finance LP

FOREX: USD - BBDXY Drifts Higher In Asia Thanks To The PBOC

The BBDXY has had a range today of 1212.73 - 1214.66 in the Asia-Pac session; it is currently trading around 1214, +0.15%. The USD has traded with a bid tone all through the Asian session as the PBOC pushed back strongly on relentless USD selling. With the US labour data showing signs of slowing and Hassett looking like being appointed as Fed chair the market is getting excited about rate cuts and this is providing headwinds for the USD. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, look for some support toward 1212 initially and then through here the more important 1205-1208 area.

- EUR/USD - Asian range 1.1653-1.1675, Asia is currently trading 1.1655. The pair moved higher, testing the 1.1680 area overnight. On the day the pair has stalled up there initially as Asia pushed back on the weaker USD. Look for dips back toward 1.1630-50 to be supported initially looking to retest the 1.1680 area again, if this support can’t hold then it could signal a move back towards 1.1580-1600.

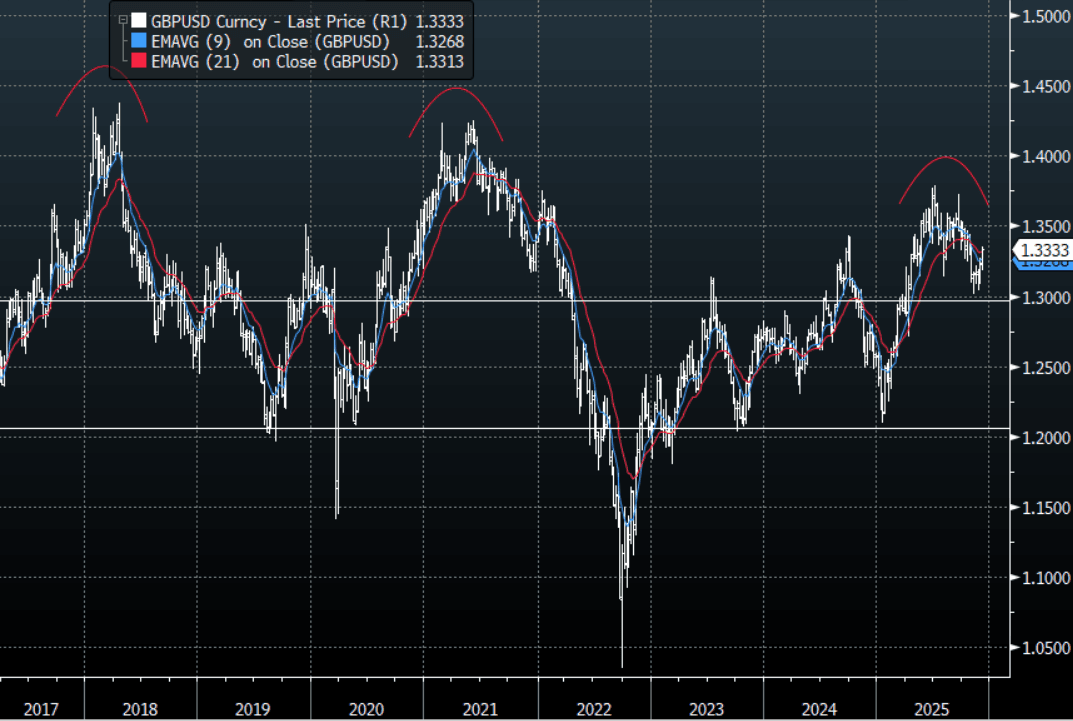

- GBP/USD - Asian range 1.3328-1.3354, Asia is currently dealing around 1.3330. The pair ripped higher breaking above 1.3280 and quickly moving back to 1.3350. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3280-1.3300 area, while above here look for the market to test the 1.3350-70 area again.

- Cross asset : SPX -0.05%, Gold $4195, US 10-Year 4.075%, BBDXY 1214, Crude Oil $59.25

- Data/Events : EZ Retail Sales, Germany HCOB Germany Construction PMI

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Bounces Off 155.00 As USD Bounces In Asia

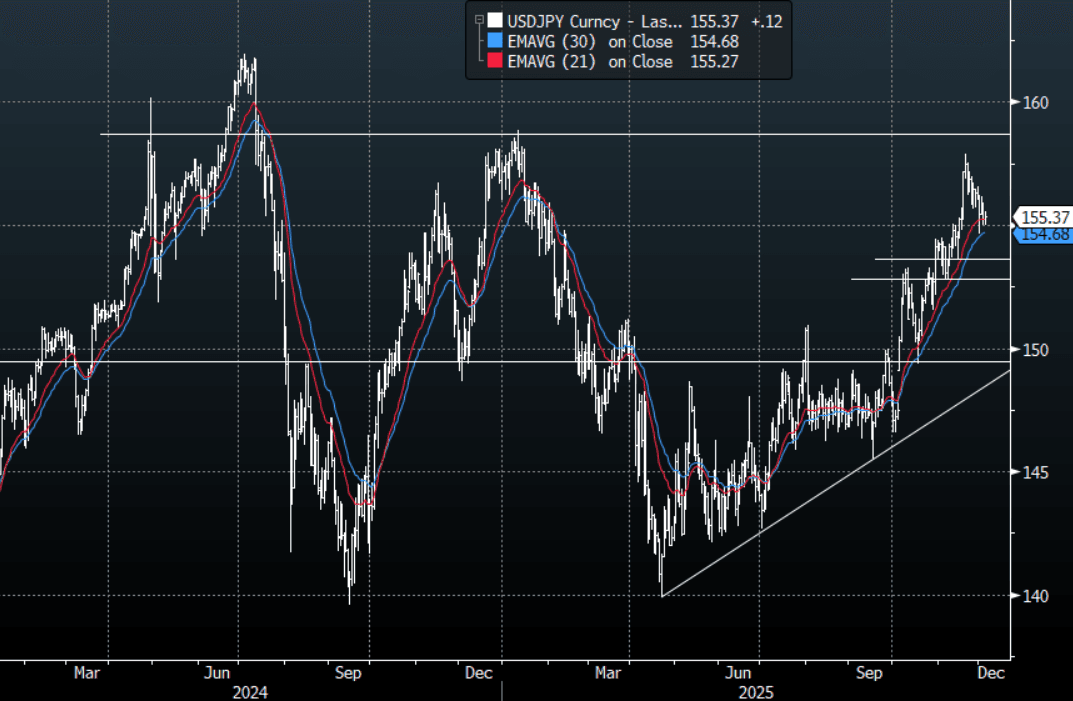

The USD/JPY range today has been 155.02 - 155.54 in the Asia-Pac session, it is currently trading around 155.40, +0.10%. The pair has bounced off the 155.00 area as the USD gets a reprieve thanks to pushback from the PBOC in our session. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December, as well as the U.S. firming its pricing of more potential cuts. This has stalled the upward momentum and should keep it contained in the short-term but I still suspect the market will still look for opportunities to express a long USD at the right levels. Technically USD/JPY is still in an uptrend with the first big support back toward the 153-155 area which should see buyers reemerge. On the day I suspect we will continue to consolidate within a wider 154.75-156.25 range.

- MNI Policy: BOJ Frets Over Neutral Rate Update. They are concerned that future market signalling will become more difficult as the policy rate moves closer to the bank’s 1-2.5% neutral-rate estimate.

- MNI AU - BOJ-dated OIS currently assigns an 80% probability to a 25bp hike in December, rising to 99% by March 2026. As recently as 21 November, markets saw less than a 20% chance of a December move. Notably, investors are now pricing in two 25bp hikes by October 2026.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($1.2b), 154.00($900m), 155.70($993m). Upcoming Close Strikes : 155.00($1.81b Dec 5), 156.00($1.44b Dec 8 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 91 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD/USD - Holds Above 0.6600, Even With A Stronger USD

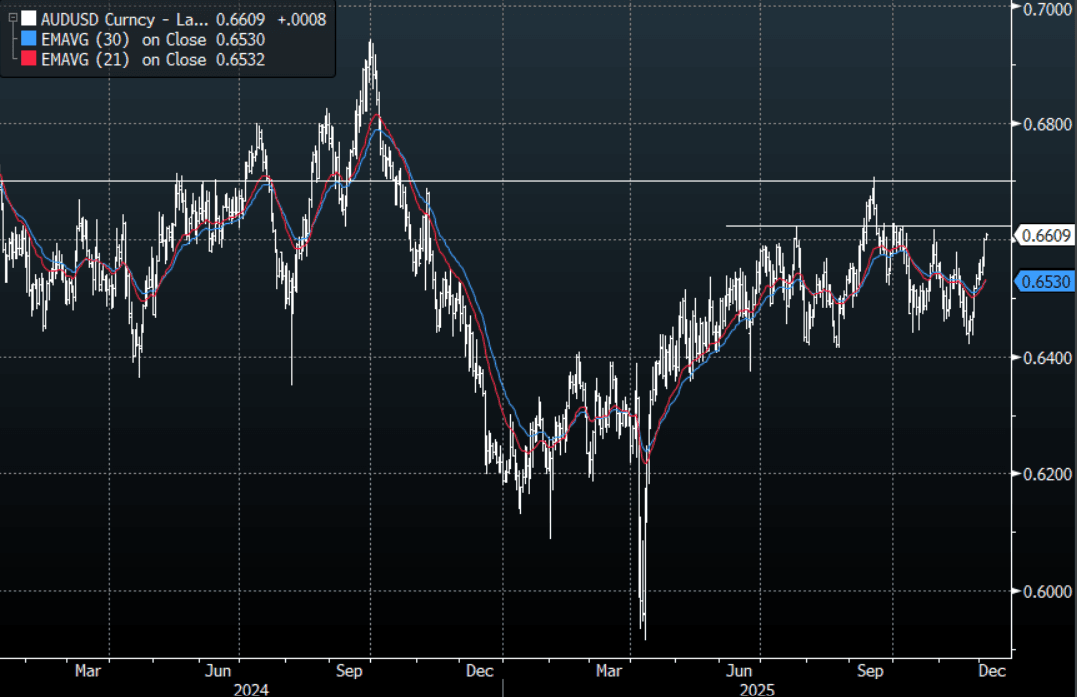

The AUD/USD has had a range today of 0.6598 - 0.6611 in the Asia- Pac session, it is currently trading around 0.6610, +0.15%. The AUD/USD has tried to push above 0.6600 in our session but without much follow through as China pushes back aggressively on the relentless USD selling which put a bottom under it in Asia. The AUD price action remains constructive and indicative of a market with solid buying interest as it pushed through the 0.6580 pivot area overnight. On the day, I suspect dips back toward the 0.6560-0.6580 area could now be supported. The AUD is now looking to build some momentum to once again test the top end of its recent range, first target 0.6630 and then 0.6700.

- MNI AU - Consumer Recovery In Place, RBA On Hold. October household spending is another piece of data signalling robust domestic demand in Australia after Q3 showed it rose 1.2% q/q. With Governor Bullock saying yesterday that the output gap has likely closed, this strength on the demand side is another reason for the RBA to be on hold beyond the 9 December decision given that inflation is above the top of the band.

- MNI AU - AU-US 10Y Diff Extends Push Beyond Old Trading Range: Cash ACGBs are 2-4bps cheaper today, with the AU-US 10-year yield differential at +59bps

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD357m), 0.6490(AUD710m). Upcoming Close Strikes : 0.6475(AUD814m Dec 8 ), 0.6500(AUD1.11b Dec 5), 0.6635(AUD651m Dec 9) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Drifts Lower As PBOC Pushes Back

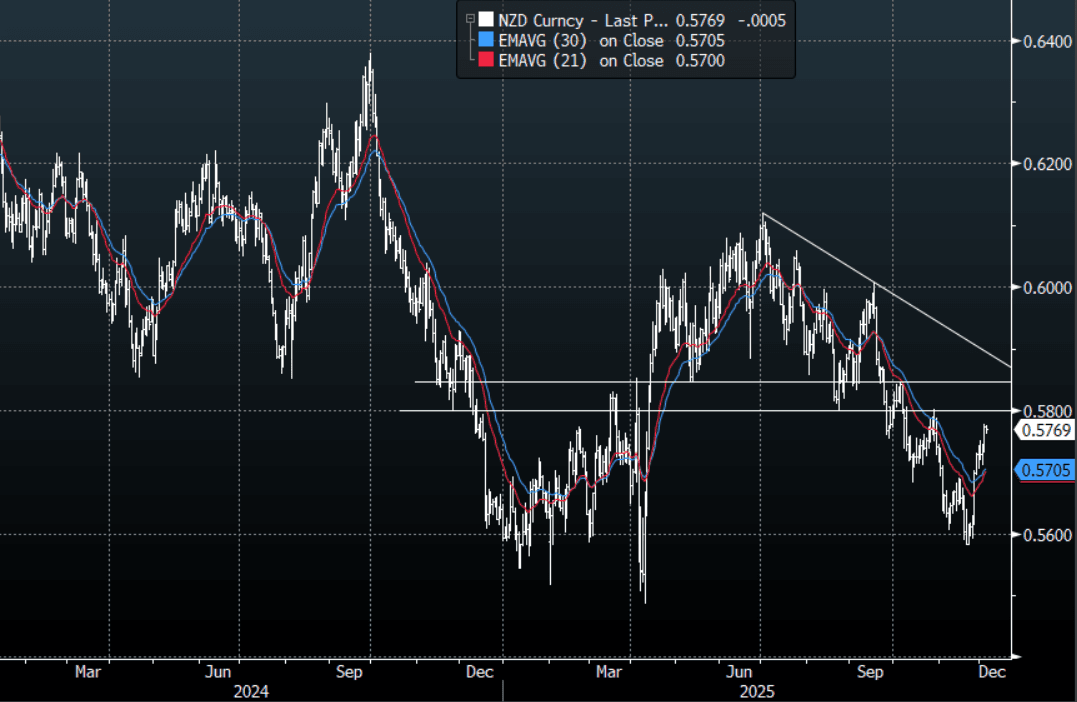

The NZD/USD had a range today of 0.5761-0.5778 in the Asia-Pac session, going into the London open trading around 0.5770, -0.10%. The NZD/USD has drifted lower as China pushes back aggressively on the relentless USD selling which put a bottom under it in Asia. On the day, look for support now back toward the 0.5735-0.5755 area as the focus turns back toward the more important 0.5800-50 resistance where I suspect sellers could return initially.

- (Bloomberg) - That was the most forceful pushback from the PBOC at a daily dollar-yuan fixing since 2022. But it’s likely the central bank will need to repeat the dose in coming days with the US dollar softening into next week’s Fed meeting.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5670(NZD382m Dec 8 ), 0.5700(NZD332m Dec 5), 0.5730(NZD692m Dec 8 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 38 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

EQUITIES: US Equities Stabilise Ahead Of Jobs Data, US News Supports Asian Tech

US futures have drifted lower in Asian trading with E-minis -0.02% and NQZ5 - 0.10%. This comes after a powerful move higher overnight as the US builds on its reversal of the weak start to the week. Weak labour data contributed to the move as the market gears up for U.S. rate cuts. Tonight we have Challenger Job Cuts and Initial Jobless claims. The market will be watching these closely to get confirmation of a cooling labour market to reinforce their rates view.

- Asian equities are mixed with the KOSPI weaker but Nikkei rallying. Risk sentiment is moderately stronger with commodities up.

- HK and China equities are higher with the Hang Seng +0.2% and CSI 300 0.3%. Hang Seng Tech is outperforming up 0.6% supported by robotic companies on reports that the White House will make an announcement in 2026. The US apparently wants to grow the sector, according to Politico.

- The ASX is up 0.2% driven by miners given higher commodity prices, especially copper. However, increasing RBA rate hike expectations is pressuring domestic equities. The NZX50 in contrast is down 0.5%.

- Korea’s KOSDAQ is outperforming the KOSPI down 0.1% compared with -0.7%.

- ASEAN indices are mixed with the Jakarta Comp up 0.2% but Straits Times down 0.3%.

- Later US November Challenger job cuts, 29 November jobless claims and delayed September orders are released as well as euro area October retail sales, Canada’s October trade & November PMI. The ECB’s Lane, de Guindos and Cipollone, and BoE’s Mann appear.

OIL: Geopolitical Risks Continue To Provide Support To Oil Prices

After rising on Wednesday driven by the lack of a Ukraine peace deal, oil prices are moderately higher again in today’s APAC trading but continue to move in a relatively narrow range. Whether an agreement can be achieved remains highly uncertain. Geopolitical risks for Ukraine and Venezuela are supporting crude but projections of a record 2026 market surplus remain the major concern.

- WTI is up 0.5% to $59.25/bbl, close to the intraday peak at $59.29. Brent is 0.4% higher at $62.92/bbl after reaching $62.98. Both continue to trade well below initial resistance levels.

- The IEA, EIA and OPEC monthly reports for December are published next week, which should frame the supply/demand outlook. Fundamentals continue to signal subdued oil prices.

- Venezuela remains in the headlines with President Trump saying that drug cartels will be targeted and not just at sea. Yesterday, Secretary of State Rubio said that negotiating a deal would be difficult as Venezuela’s Maduro has “broken every deal he’s ever made”. Venezuela was the world’s 17th largest oil exporter in 2023 (IEA).

- Ukrainian officials are scheduled to meet with US envoy Witkoff in Florida on Thursday. Trump said that Witkoff’s meeting with President Putin was “reasonably good”.

- Later US November Challenger job cuts, 29 November jobless claims and delayed September orders are released as well as euro area October retail sales, Canada’s October trade & November PMI. The ECB’s Lane, de Guindos and Cipollone, and BoE’s Mann appear.

PRECIOUS METALS: Gold & Silver Lower As USD Rises, More US Jobs Data Later

Gold and silver were stronger early in Thursday’s APAC session driven by the fall in November ADP employment but have declined as the US dollar strengthened (BBDXY +0.1%) while the 2-year yield is slightly higher. There are more jobs data out of the US today.

- Silver is down 0.6% to $58.15 after reaching $58.754, just below resistance at $58.947, and then falling to $58.033. It has outperformed gold in recent sessions not only driven by expectations of Fed easing and a dovish new Fed Chair in 2026 but also a tight physical market, which has encouraged speculators into the market. It is now flashing overbought and given lower volumes than gold is at risk of volatility.

- Gold is 0.2% lower at $4196.0 off the intraday trough of $4187.66 following a high of $4216.85. It has been range trading over much of this week, as a December Fed rate cut is almost fully priced in.

- Equities are mixed with the S&P e-mini down 0.1% and KOSPI -1.0% but Nikkei up 1.5% and Hang Seng +0.3%. Oil prices are higher with WTI +0.5% to $59.25/oz. Copper is up 0.5%.

- Later US November Challenger job cuts, 29 November jobless claims and delayed September orders are released as well as euro area October retail sales, Canada’s October trade & November PMI. The ECB’s Lane, de Guindos and Cipollone, and BoE’s Mann appear.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0800/0900 | ** | Unemployment | |

| 04/12/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/12/2025 | 0930/0930 | BOE Decision Maker Panel Data | ||

| 04/12/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/12/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference | ||

| 04/12/2025 | 1300/1400 | ECB Cipollone Chairs Panel on Fiscal Policy | ||

| 04/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 04/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 04/12/2025 | 1500/1000 | * | Ivey PMI | |

| 04/12/2025 | 1500/1600 | ECB Lane at Fiscal Policy Conference | ||

| 04/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 04/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/12/2025 | 1730/1230 | Fed Vice Chair Michelle Bowman | ||

| 04/12/2025 | 1800/1900 | ECB de Guindos Speech at Business Innovation Awards | ||

| 05/12/2025 | 2330/0830 | ** | Household spending | |

| 05/12/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/12/2025 | 0730/0730 | DMO to publish issuance calendar for FQ4 | ||

| 05/12/2025 | 0745/0845 | * | Industrial Production | |

| 05/12/2025 | 0745/0845 | * | Foreign Trade | |

| 05/12/2025 | 0800/0900 | ** | Industrial Production | |

| 05/12/2025 | 0900/1000 | * | Retail Sales | |

| 05/12/2025 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey |