EQUITIES: US Equities Stabilise Ahead Of Jobs Data, US News Supports Asian Tech

US futures have drifted lower in Asian trading with E-minis -0.02% and NQZ5 - 0.10%. This comes after a powerful move higher overnight as the US builds on its reversal of the weak start to the week. Weak labour data contributed to the move as the market gears up for U.S. rate cuts. Tonight we have Challenger Job Cuts and Initial Jobless claims. The market will be watching these closely to get confirmation of a cooling labour market to reinforce their rates view.

- Asian equities are mixed with the KOSPI weaker but Nikkei rallying. Risk sentiment is moderately stronger with commodities up.

- HK and China equities are higher with the Hang Seng +0.2% and CSI 300 0.3%. Hang Seng Tech is outperforming up 0.6% supported by robotic companies on reports that the White House will make an announcement in 2026. The US apparently wants to grow the sector, according to Politico.

- The ASX is up 0.2% driven by miners given higher commodity prices, especially copper. However, increasing RBA rate hike expectations is pressuring domestic equities. The NZX50 in contrast is down 0.5%.

- Korea’s KOSDAQ is outperforming the KOSPI down 0.1% compared with -0.7%.

- ASEAN indices are mixed with the Jakarta Comp up 0.2% but Straits Times down 0.3%.

- Later US November Challenger job cuts, 29 November jobless claims and delayed September orders are released as well as euro area October retail sales, Canada’s October trade & November PMI. The ECB’s Lane, de Guindos and Cipollone, and BoE’s Mann appear.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Market Cheapens As Gov Bullock Delivers A Hawkish Tone

ACGBs (YM -4.5 & XM -2.5) cheapen during RBA Gov Bullock’s presser.

- RBA Governor Michele Bullock said the labour market remains slightly tight relative to full employment and that the Board did not consider cutting or raising rates at its latest meeting, opting instead to hold and review its strategy. She noted that while both inflation and unemployment have risen, the Board is more concerned about inflation, with core inflation above 3% considered “not ideal.”

- Bullock added that the RBA may not need to cut rates much further.

- She dismissed concerns about stagflation.

- Overall, her comments carried a slightly hawkish tone.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +25bps.

- The bills strip is -3 to -6 across contracts.

- RBA-dated OIS pricing had implied just a 3% probability of a move today. As it currently stands, the OIS market has a 75% chance of a 25bp cut by mid-2026.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.

- Tomorrow, the local calendar will see S&P Global Composite & Services PMIs.

US TSYS: Treasuries Look to QTRLY Borrowing Estimates for Next Catalyst

US bond futures didn't get out of bed today, with the 10-Yr where it started at 112-21+ to remain at the mid-point of the 50-day EMA and the 100-day EMA. With economic data releases still constrained by the government shutdown, bonds will look to the release this week of the maturity breakdown for funding going forward into 2026. Current expectations are for a significant increase in bill issuance that should create increased demand for longer bonds, thus bring yields down and lowering the interest cost for the government.

Cash was quiet from the open also inching lower in yield after last night's rise with all maturities around 0.5bps lower in yield.

- The 2-Yr is marginally lower at 3.60%.

- The 5-Yr is at 3.71%

- The 10-Yr is steady at 4.10%

- The 30-Yr is -0.5bps lower at 4.68%

Tonight's focus for issuance will continue to come from corporates, where the blockbuster start to the month is set to continue. For USTs the focus will be US$95bn 6-week bills

JGBS: Curve Steepens Ahead Of Tomorrow's 10Y Supply

JGB futures are weaker and at session lows, -20 compared to the settlement levels.

- “Japanese Prime Minister Sanae Takaichi will put together the nation’s new growth strategy by next summer, while pledging to boost tax revenues without increasing taxation rates." - BBG

- MNI Brief: Japan’s economy is expected to have contracted for the first time in six quarters in the July-September period, as weaker private consumption and capital investment offset earlier front-loaded gains, according to private economists. Preliminary estimates suggest GDP fell 0.7% quarter-on-quarter, or an annualised 2.7%, reversing from a 0.5% q/q (annualised 2.2%) expansion in the April-June quarter.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off.

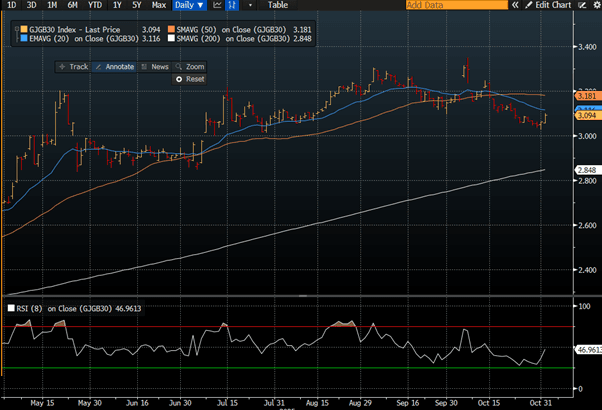

- Cash JGBs are flat to 3bps cheaper across benchmarks, with the 30-year underperforming. The benchmark 30-year yield is at 3.094% versus the cycle high of 3.35%. The near-term technical bias, however, appears lower. (see chart)

- Swap rates are 1-4bps higher, with a steepening bias.

- Following last week's policy decision, BoJ-dated OIS pricing is softer across late 2025/early 2026 meetings compared to early August levels, but slightly firmer for mid to late 2026 meetings.

- Tomorrow, the local calendar will see BOJ Minutes (Sep MPM) and Monetary base data alongside 10-year supply.

Source: Bloomberg Finance LP