JGBS: 10YY Up But 30YY Down, BOJ Ueda: Fiscal Stimulus To Boost UCPI

JGB futures are back near session lows, -20 compared to settlement levels, after quickly reversing the spike higher following today’s 30-year auction result.

- The 30-year JGB auction delivered strong results. The low price exceeded dealer expectations of 96.40 (Bloomberg survey), the cover ratio jumped to 4.0445x—the highest since 2019—from 3.1248x, and the auction tail narrowed sharply to 0.09 from 0.27, all pointing to firmer bidding.

- MNI - BOJ Governor Kazuo Ueda said on Thursday that the government’s economic stimulus package will have a positive impact on economic growth and boost underlying inflation. Ueda told lawmakers that the stimulus package, mainly countermeasures to cope with high prices, will lower headline CPI, but it will exert upward pressure on underlying inflation through economic growth. However, he could not comment on the degree of the impact.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

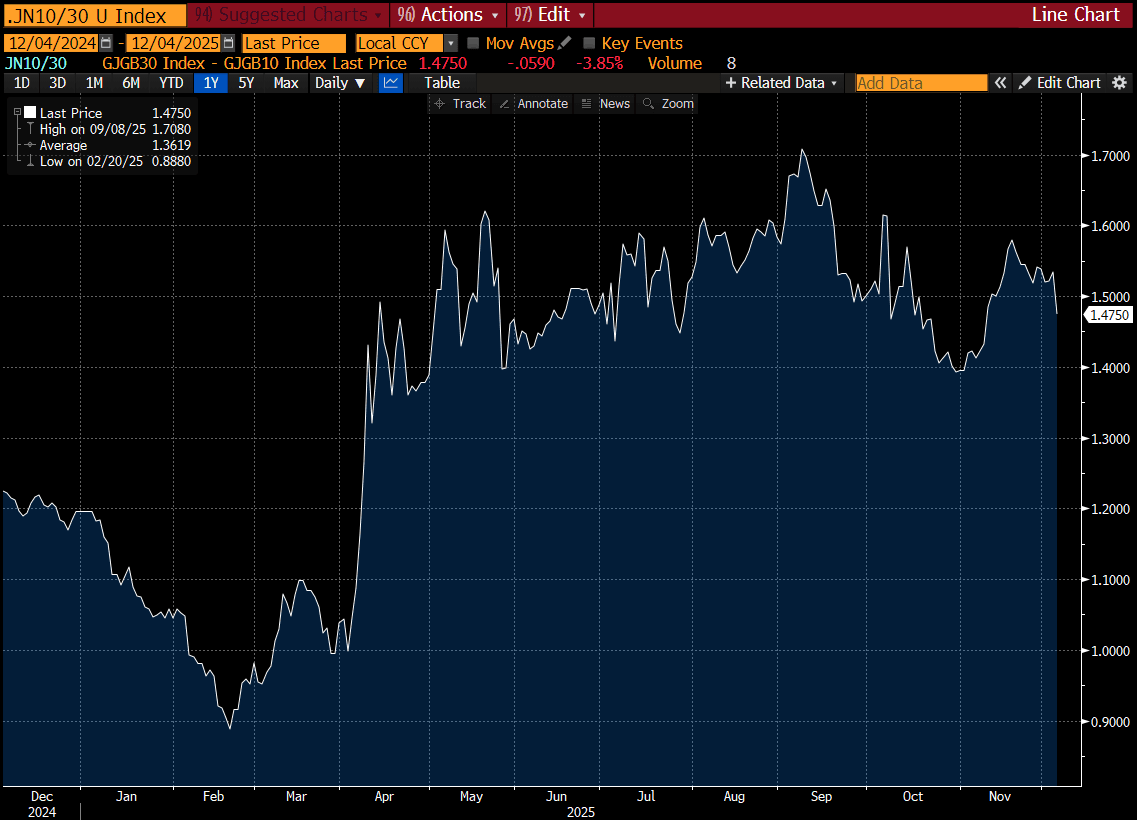

- Cash JGBs are mixed across benchmarks, with the 10-year underperforming (+2.6bps) and the 30-year outperforming (-3.2bps) (see chart).

- Swap rates are flat to 3bps higher.

- Tomorrow, the local calendar will see Household Spending and the Coincident/Leading Index data.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Treasuries Look to QTRLY Borrowing Estimates for Next Catalyst

US bond futures didn't get out of bed today, with the 10-Yr where it started at 112-21+ to remain at the mid-point of the 50-day EMA and the 100-day EMA. With economic data releases still constrained by the government shutdown, bonds will look to the release this week of the maturity breakdown for funding going forward into 2026. Current expectations are for a significant increase in bill issuance that should create increased demand for longer bonds, thus bring yields down and lowering the interest cost for the government.

Cash was quiet from the open also inching lower in yield after last night's rise with all maturities around 0.5bps lower in yield.

- The 2-Yr is marginally lower at 3.60%.

- The 5-Yr is at 3.71%

- The 10-Yr is steady at 4.10%

- The 30-Yr is -0.5bps lower at 4.68%

Tonight's focus for issuance will continue to come from corporates, where the blockbuster start to the month is set to continue. For USTs the focus will be US$95bn 6-week bills

JGBS: Curve Steepens Ahead Of Tomorrow's 10Y Supply

JGB futures are weaker and at session lows, -20 compared to the settlement levels.

- “Japanese Prime Minister Sanae Takaichi will put together the nation’s new growth strategy by next summer, while pledging to boost tax revenues without increasing taxation rates." - BBG

- MNI Brief: Japan’s economy is expected to have contracted for the first time in six quarters in the July-September period, as weaker private consumption and capital investment offset earlier front-loaded gains, according to private economists. Preliminary estimates suggest GDP fell 0.7% quarter-on-quarter, or an annualised 2.7%, reversing from a 0.5% q/q (annualised 2.2%) expansion in the April-June quarter.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off.

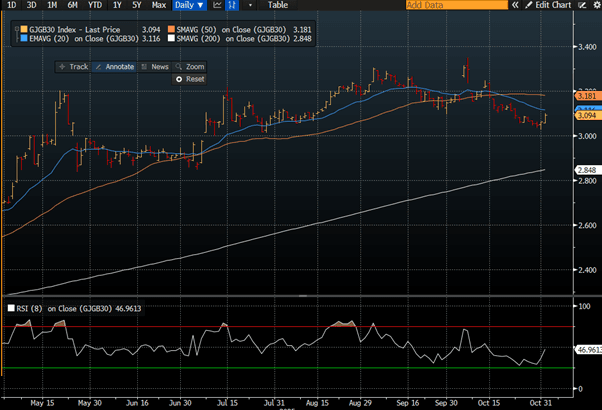

- Cash JGBs are flat to 3bps cheaper across benchmarks, with the 30-year underperforming. The benchmark 30-year yield is at 3.094% versus the cycle high of 3.35%. The near-term technical bias, however, appears lower. (see chart)

- Swap rates are 1-4bps higher, with a steepening bias.

- Following last week's policy decision, BoJ-dated OIS pricing is softer across late 2025/early 2026 meetings compared to early August levels, but slightly firmer for mid to late 2026 meetings.

- Tomorrow, the local calendar will see BOJ Minutes (Sep MPM) and Monetary base data alongside 10-year supply.

Source: Bloomberg Finance LP

ASIA STOCKS: Nikkei / KOSPI in Rare Down Day as CSI Approaches Key Tech Level

In a day where stock specific news was muted, a pull back occurred for major bourses which for some was the first in several days. Whilst tech stocks are still underwriting the positive momentum in Asia, a minor pullback was due. The DOW finished modestly down and with futures pointing down also, most major bourses opened on the back foot. The KOSPI's fall can also be attributed to the unusual occurrence that occurred overnight with the Korea Exchange issuing an 'investment caution' over SK Hynix shares. SK Hynix are up over 280% from their lows this year. The warning sees the company's shares down 6% today, with Samsung down -3.5%.

- The KOSPI was the biggest faller today, with losses of -1.90%, the biggest one day fall since September. It does little to change the technical backdrop with the KOSPI remaining above all major moving averages, and overbought on the 14-day Relative Strength Index.

- The NIKKEI's fall of -0.50% does little to impact the technical backdrop for the index. All major moving averages are steep in their upward slope, an indicator that the positive momentum remains.

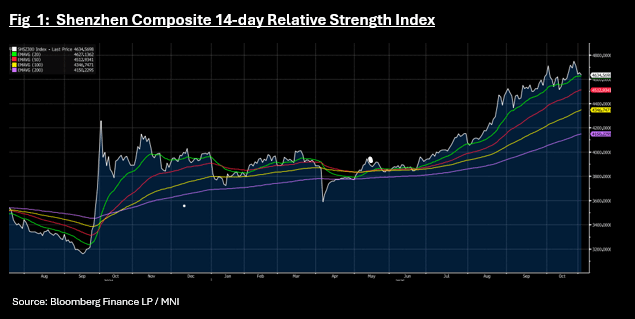

- China's major bourses are again inversely correlated with the Hang Seng up modestly by +0.20%, whilst the CSI 300 is down -0.40%, Shanghai down -0.19% and Shenzhen down -1.09%. Shenzhen's technical pullback mirrors that of the CSI 300 as they both near their 20-day EMA.

- SE Asia's major bourses are mixed with the JCI up +0.27%, FTSE Malay up +0.15% whilst the SE Thai is down -0.38% for its fourth day of falls as it nears its 20-day EMA.