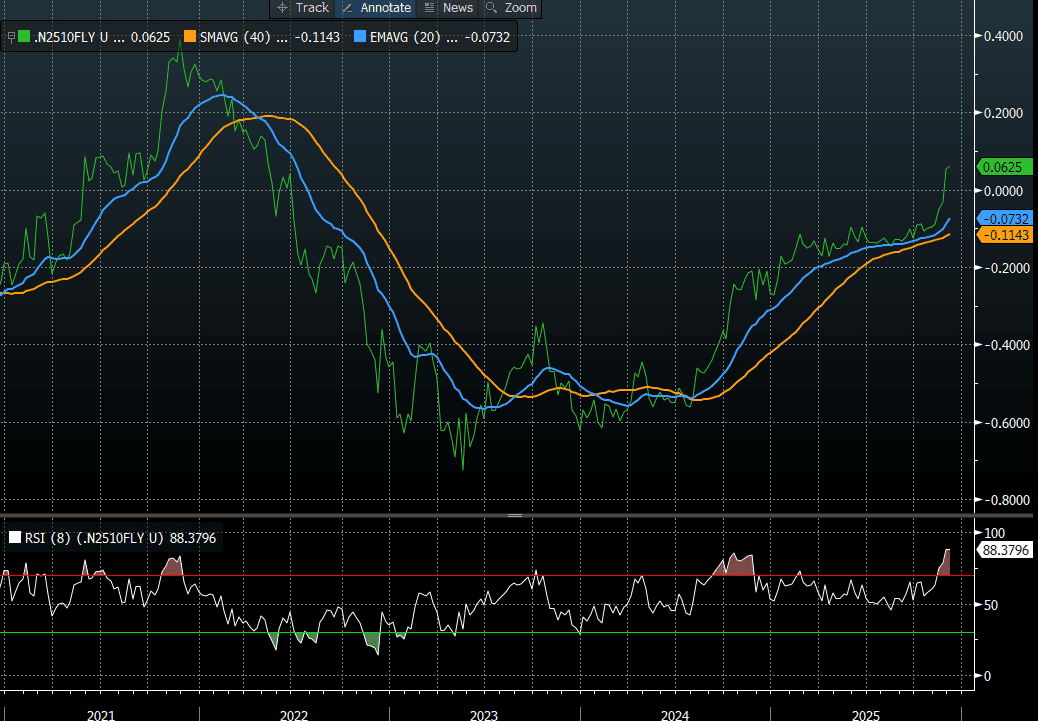

BONDS: NZGBS: Slightly Richer Today But 5Y Remains Cheap In The Fly

NZGBs closed flat to 2bps richer, with the 5-year outperforming. Nevertheless, yields remain 12-24bps higher than last week's pre-RBNZ levels, with the 5-year the underperformer.

- Indeed, on a relative value basis, the 5-year swap is at its cheapest valuation since mid-2022, based on the 2-/5-/10-year butterfly spread (see chart).

- Today’s weekly supply delivered mixed results, with cover ranging from 2.72x (May-35) to 5.23x (May-51).

- On a relative basis versus its $-bloc counterparts, NZGBs also had a good day, with the NZ-US and NZ-AU 10-year yield differentials 1bp and 4bps lower, respectively.

- “New Zealand residential building rebounded in the third quarter, with the volume of residential building work rising 2.8% from the second quarter. The rebound in construction follows a pick up in third-quarter retail sales and exports, suggesting gross domestic product is recovering after a contraction in the second quarter.” - BBG

- RBNZ-dated OIS pricing closed little changed across meetings. 1bps of easing is priced for February, while November 2026 assigns 30bps of tightening.

- The local calendar will be empty until next Wednesday, when RBNZ Governor Breman hosts a media Q+A alongside Net Migration data.

Bloomberg Finance LP

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

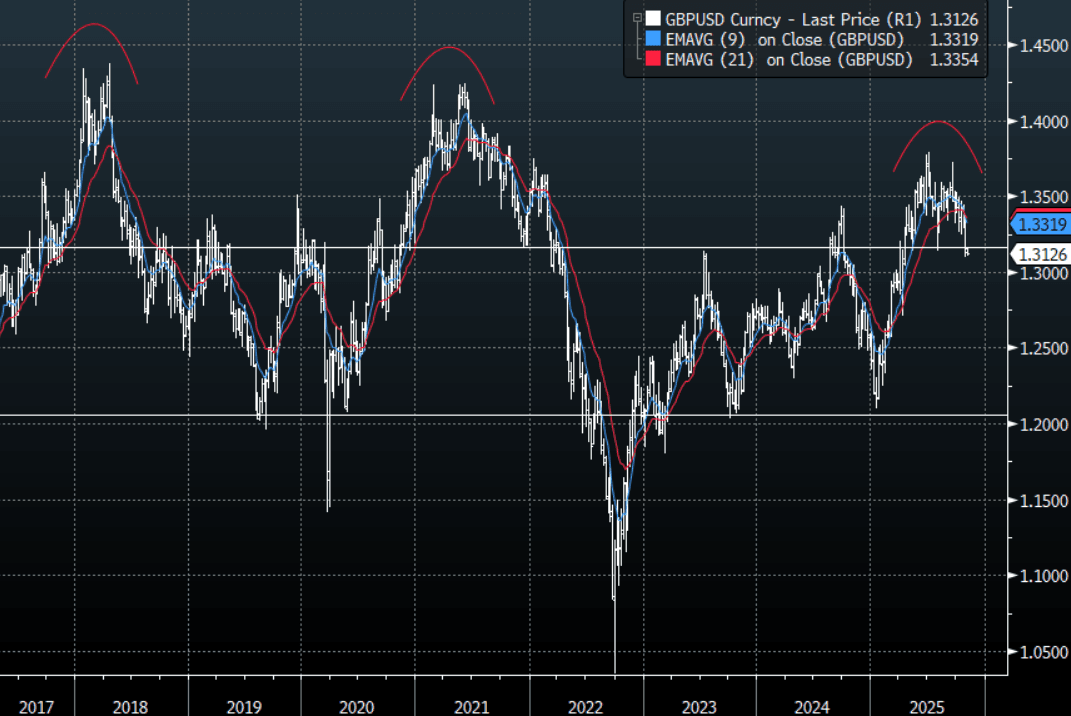

FOREX: Asia-Pac FX: The USD Continues To Grind Higher, Testing Resistance

The BBDXY has had a range today of 1221.38 - 1223.25 in the Asia-Pac session; it is currently trading around 1222, +0.10%. The USD continues to build on its recent gains eking out new highs every day. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- EUR/USD - Asian range 1.1498 - 1.1523, Asia is currently trading 1.1515. The pair has moved back toward its support just above 1.1500. A break under this support could signal a deeper correction, first target 1.1400 and then the 1.1100/1.1200 area.

- GBP/USD - Asian range 1.3118 - 1.3162, Asia is currently dealing around 1.3125. The pair looks to be building some downward momentum. This 1.3100/1.3150 area has proved to be supportive on more than 1 occasion this year so some work around this level could be expected. I continue to favor fading rallies though as GBP attempts to put in a medium term top.

- Cross asset : SPX -0.45%, Gold $3988, US 10-Year 4.1050%, BBDXY 1222, Crude Oil $60.90

- Data/Events : Italy New Car Registrations YoY, France Budget Balance YTD, Spain Unemployment Change

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

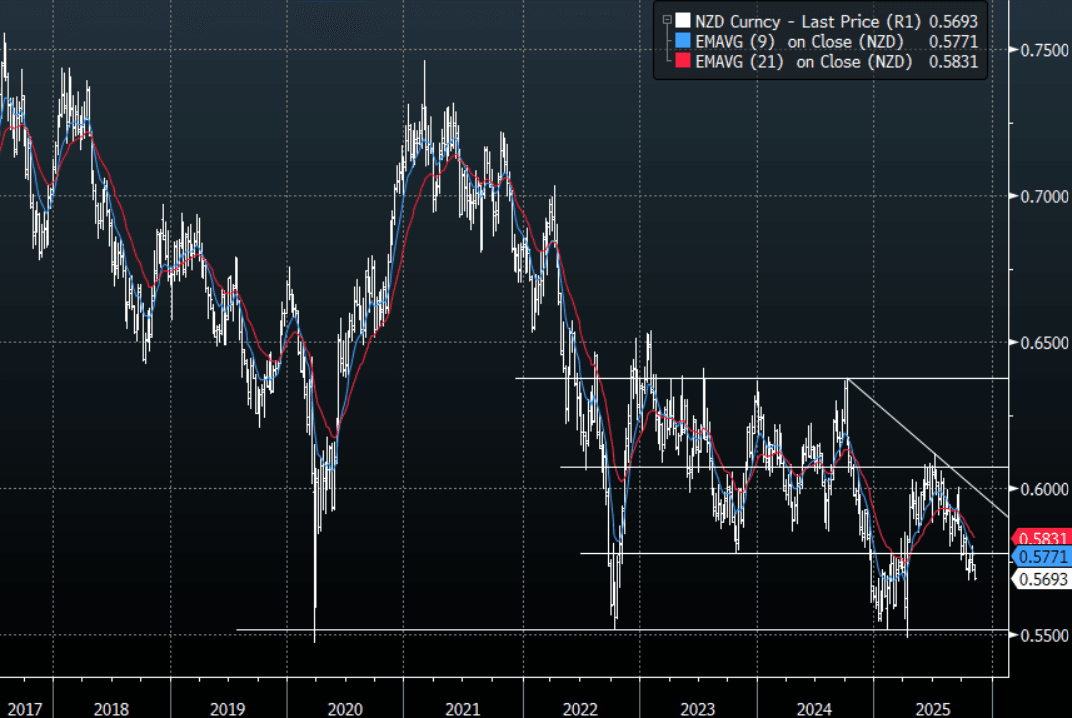

NZD: Asia-Pac: NZD/USD Trades Heavy Breaking Below Overnight Lows

The NZD/USD had a range of 0.5686 - 0.5710 in the Asia-Pac session, going into the London open trading around 0.5695, -0.25%. The NZD has slipped lower and remained under pressure for most of our session. While price remains below the 0.5800/50 area I suspect rallies continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. NZD continues to stand out as a short against a resurgent USD but it is worth noting that because of the size of the market the market can very quickly become all positioned the same way, so I think the USD will need to break above its pivotal resistance for the NZD to test those lows. That being said, a poor unemployment print tomorrow in New Zealand would certainly give it another nudge.

- MNI AU - Significantly Weaker Jobs Data Could Increase Easing Expectations: Q3 jobs and wages data are released Wednesday and with spare capacity an important driver of monetary easing, will be monitored closely as there has been excess supply in the labour market. Monthly data in the quarter signal there was a stabilization but employment is likely to have remained soft. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ’s August projections. A 25bp cut on 26 November is generally expected but if the labour data print significantly weaker, then expectations of 50bp may increase.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD1.1b Nov 5), 0.5675(NZD1.05b Nov 5), 0.5750(NZD604m Nov 5) - BBG

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

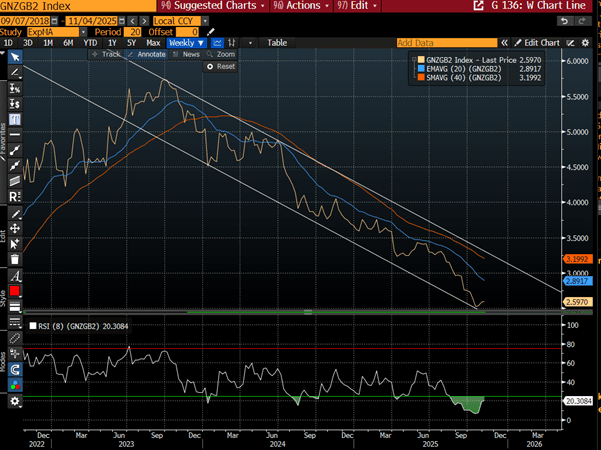

BONDS: NZGBS: Steady Ahead Of Labour Mkt & Wages Data

NZGBs closed little changed across benchmarks after a subdued session.

- Tomorrow sees the key event of the week’s calendar with the release of Q3 labour market and wages data.

- Filled jobs for the quarter signal a stabilisation, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- Swap rates are little changed. The 2-year rate is holding its recent rise, bouncing off channel support, after reaching extreme overbought conditions. (see chart)

- RBNZ dated OIS pricing is little changed across meetings. 24bps of easing is priced for November, with a cumulative 31bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP