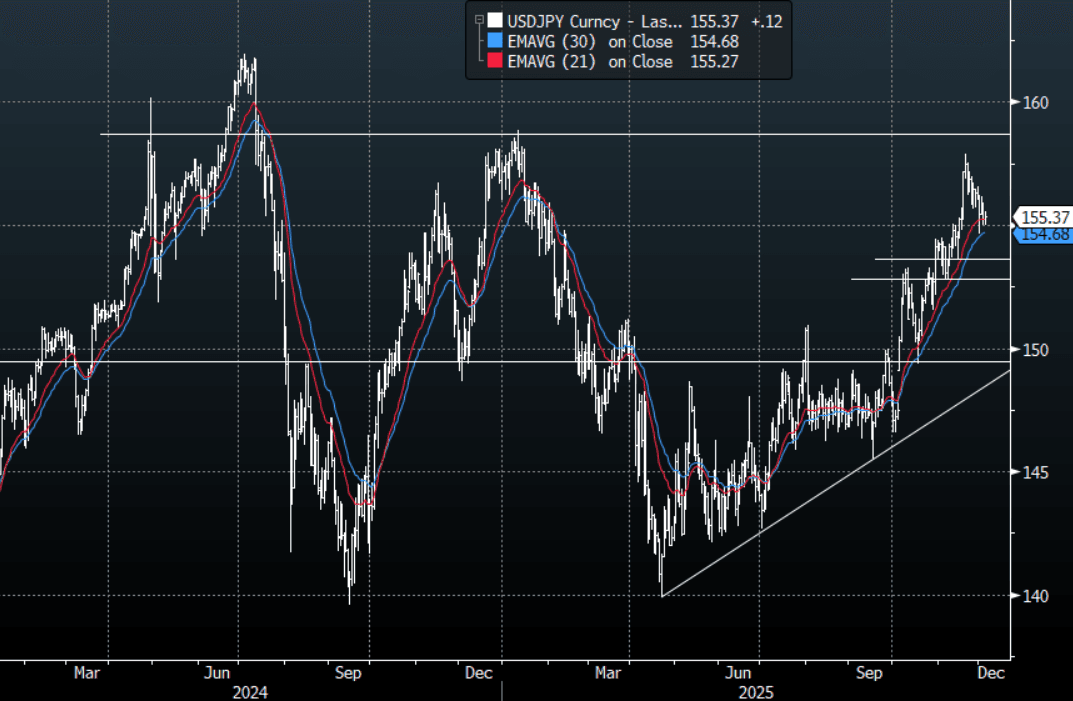

JPY: USD/JPY - Bounces Off 155.00 As USD Bounces In Asia

The USD/JPY range today has been 155.02 - 155.54 in the Asia-Pac session, it is currently trading around 155.40, +0.10%. The pair has bounced off the 155.00 area as the USD gets a reprieve thanks to pushback from the PBOC in our session. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December, as well as the U.S. firming its pricing of more potential cuts. This has stalled the upward momentum and should keep it contained in the short-term but I still suspect the market will still look for opportunities to express a long USD at the right levels. Technically USD/JPY is still in an uptrend with the first big support back toward the 153-155 area which should see buyers reemerge. On the day I suspect we will continue to consolidate within a wider 154.75-156.25 range.

- MNI Policy: BOJ Frets Over Neutral Rate Update. They are concerned that future market signalling will become more difficult as the policy rate moves closer to the bank’s 1-2.5% neutral-rate estimate.

- MNI AU - BOJ-dated OIS currently assigns an 80% probability to a 25bp hike in December, rising to 99% by March 2026. As recently as 21 November, markets saw less than a 20% chance of a December move. Notably, investors are now pricing in two 25bp hikes by October 2026.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($1.2b), 154.00($900m), 155.70($993m). Upcoming Close Strikes : 155.00($1.81b Dec 5), 156.00($1.44b Dec 8 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 91 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

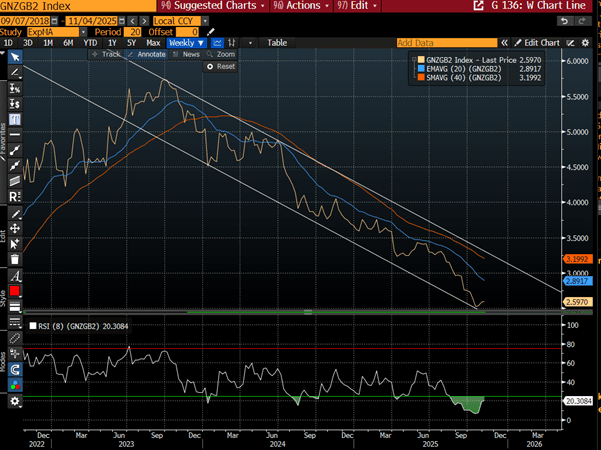

BONDS: NZGBS: Steady Ahead Of Labour Mkt & Wages Data

NZGBs closed little changed across benchmarks after a subdued session.

- Tomorrow sees the key event of the week’s calendar with the release of Q3 labour market and wages data.

- Filled jobs for the quarter signal a stabilisation, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- Swap rates are little changed. The 2-year rate is holding its recent rise, bouncing off channel support, after reaching extreme overbought conditions. (see chart)

- RBNZ dated OIS pricing is little changed across meetings. 24bps of easing is priced for November, with a cumulative 31bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

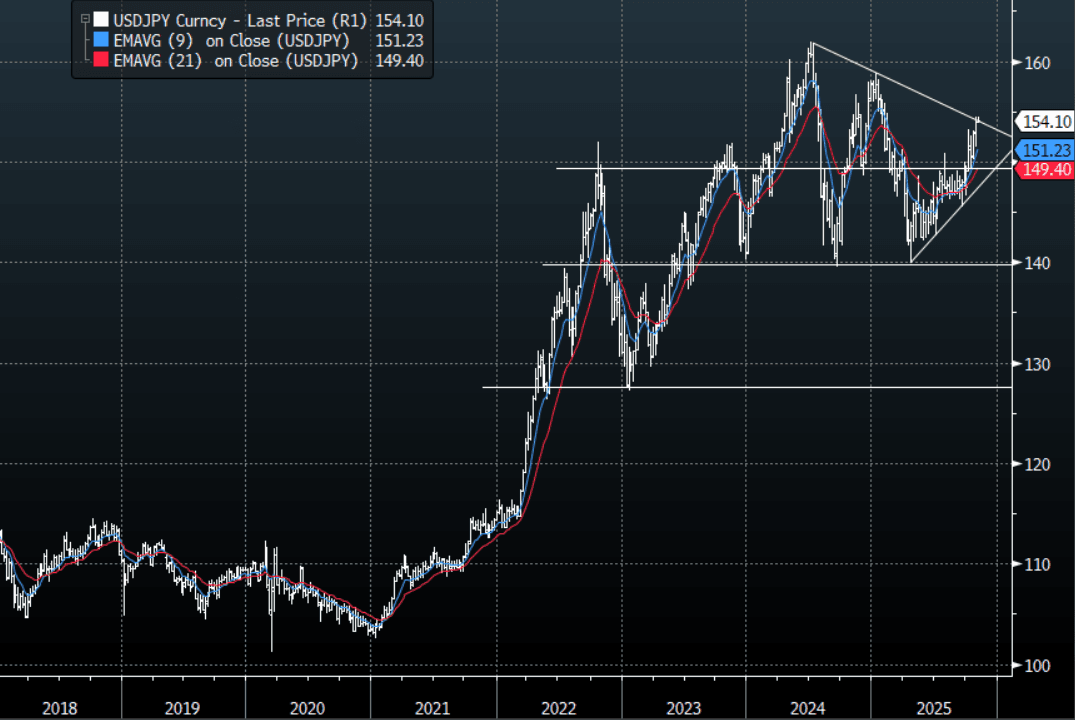

JPY: Asia-Pac: USD/JPY - Official Jaw-Boning Sees It Pull Back To 154.00

The USD/JPY range today has been 154.06 - 154.48 in the Asia-Pac session, it is currently trading around 154.10, +0.05%. The pair remains well supported thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are testing some resistance around the 154/155 area and I would expect we might to do some work around here initially. A sustained break back above 155 could see the move begin to accelerate and with that the potential for a new round of intervention, though personally I think they will wait for levels closer to 160 to get involved. Look for dips to continue to be supported while above 149-150, the first buy zone is back toward the 152.00 area.

- Yen comments by the FinMin today show FX remains a close watch point for the authorities. Still, based on historical remarks, the comments suggest concern, but not yet suggesting intervention is imminent.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

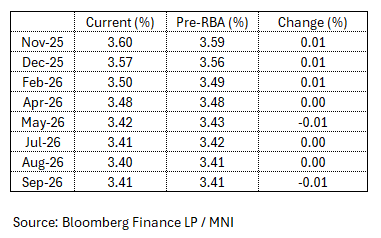

AUSSIE BONDS: Little Reaction To RBA Decision To Leave Cash Rate Unchanged

ACGBs (YM -1.0 & XM -1.5) are little changed after leaving the cash rate at 3.60%, as unanimously expected.

- The RBA Board decided to keep the cash rate unchanged, noting that inflationary pressures persist amid recovering private demand and a still-tight labour market.

- Although financial conditions have eased, the Board expects the impact of earlier rate cuts will take time to materialise.

- Citing more persistent inflation and heightened uncertainty, it chose to remain cautious and data dependent. The Board reaffirmed its commitment to price stability and full employment, saying it will adjust policy as needed based on developments in the global economy, domestic demand, inflation, and the labour market.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off

- Cash ACGBs are 1bp cheaper with the AU-US 10-year yield differential at +24bps.

- The bills strip is -1 to -3 across contracts.

- RBA-dated OIS pricing had implied just a 3% probability of a move today. As it currently stands, the OIS market has a 75% chance of a 25bp cut by mid-2026.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.