OIL: Geopolitical Risks Continue To Provide Support To Oil Prices

After rising on Wednesday driven by the lack of a Ukraine peace deal, oil prices are moderately higher again in today’s APAC trading but continue to move in a relatively narrow range. Whether an agreement can be achieved remains highly uncertain. Geopolitical risks for Ukraine and Venezuela are supporting crude but projections of a record 2026 market surplus remain the major concern.

- WTI is up 0.5% to $59.25/bbl, close to the intraday peak at $59.29. Brent is 0.4% higher at $62.92/bbl after reaching $62.98. Both continue to trade well below initial resistance levels.

- The IEA, EIA and OPEC monthly reports for December are published next week, which should frame the supply/demand outlook. Fundamentals continue to signal subdued oil prices.

- Venezuela remains in the headlines with President Trump saying that drug cartels will be targeted and not just at sea. Yesterday, Secretary of State Rubio said that negotiating a deal would be difficult as Venezuela’s Maduro has “broken every deal he’s ever made”. Venezuela was the world’s 17th largest oil exporter in 2023 (IEA).

- Ukrainian officials are scheduled to meet with US envoy Witkoff in Florida on Thursday. Trump said that Witkoff’s meeting with President Putin was “reasonably good”.

- Later US November Challenger job cuts, 29 November jobless claims and delayed September orders are released as well as euro area October retail sales, Canada’s October trade & November PMI. The ECB’s Lane, de Guindos and Cipollone, and BoE’s Mann appear.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Nikkei / KOSPI in Rare Down Day as CSI Approaches Key Tech Level

In a day where stock specific news was muted, a pull back occurred for major bourses which for some was the first in several days. Whilst tech stocks are still underwriting the positive momentum in Asia, a minor pullback was due. The DOW finished modestly down and with futures pointing down also, most major bourses opened on the back foot. The KOSPI's fall can also be attributed to the unusual occurrence that occurred overnight with the Korea Exchange issuing an 'investment caution' over SK Hynix shares. SK Hynix are up over 280% from their lows this year. The warning sees the company's shares down 6% today, with Samsung down -3.5%.

- The KOSPI was the biggest faller today, with losses of -1.90%, the biggest one day fall since September. It does little to change the technical backdrop with the KOSPI remaining above all major moving averages, and overbought on the 14-day Relative Strength Index.

- The NIKKEI's fall of -0.50% does little to impact the technical backdrop for the index. All major moving averages are steep in their upward slope, an indicator that the positive momentum remains.

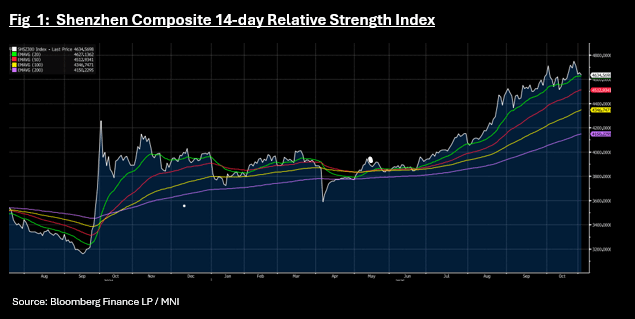

- China's major bourses are again inversely correlated with the Hang Seng up modestly by +0.20%, whilst the CSI 300 is down -0.40%, Shanghai down -0.19% and Shenzhen down -1.09%. Shenzhen's technical pullback mirrors that of the CSI 300 as they both near their 20-day EMA.

- SE Asia's major bourses are mixed with the JCI up +0.27%, FTSE Malay up +0.15% whilst the SE Thai is down -0.38% for its fourth day of falls as it nears its 20-day EMA.

RBA: Inflation Persistence Needs To Abate, Only One Cut Assumed In Forecasts

The RBA left rates at 3.6% as was widely expected but it revised up its trimmed mean forecasts to a peak of 3.2% in both Q4 2025 and Q2 2026 up from 2.6% in August. The main change to the statement was also around the “materially higher” Q3 inflation print and “recent evidence of more persistent inflation” but risks were said to be “in both directions”. The Board didn’t seem concerned about softness in the September labour market data. While inflation is assessed as “persistent” and expected to be above the top of the band, rates are likely on hold.

- Underlying inflation is projected to return to the band by Q4 2026 but the 2.5% mid-point is no longer in the forecast but as Governor Bullock previously said the further out a forecast is, the greater the uncertainty. Headline was revised up 0.3pp to 3.3% for Q4 and 0.6pp to 3.7% in Q2 2026 and is within the band in 2027.

- Inflation returns to the band using a higher rate assumption that has only one 25bp cut for H1 2026 down from 75bp assumed in August. Another sign that for now policy is on hold at “a little restrictive”.

- In September, labour market conditions were overall “stable”, whereas this month they appeared “a little tight” at the statement end, despite the 0.2pp rise in the last unemployment read. It also noted that surveys and liaison suggest “a significant share of firms are experiencing difficulty sourcing labour”. While the unemployment rate path was revised up 0.1pp to 4.4%, the Board doesn’t sound concerned.

- The growth outlook is little changed with Q4 2025 revised up 0.3pp to 2% but the rest of the path similar to August. Q4 consumption is 0.3pp higher at 2.1% supported by a lower savings rate and slightly stronger wage growth but higher inflation reduces real disposable income gains.

FOREX: Asia-Pac FX: The USD Continues To Grind Higher, Testing Resistance

The BBDXY has had a range today of 1221.38 - 1223.25 in the Asia-Pac session; it is currently trading around 1222, +0.10%. The USD continues to build on its recent gains eking out new highs every day. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- EUR/USD - Asian range 1.1498 - 1.1523, Asia is currently trading 1.1515. The pair has moved back toward its support just above 1.1500. A break under this support could signal a deeper correction, first target 1.1400 and then the 1.1100/1.1200 area.

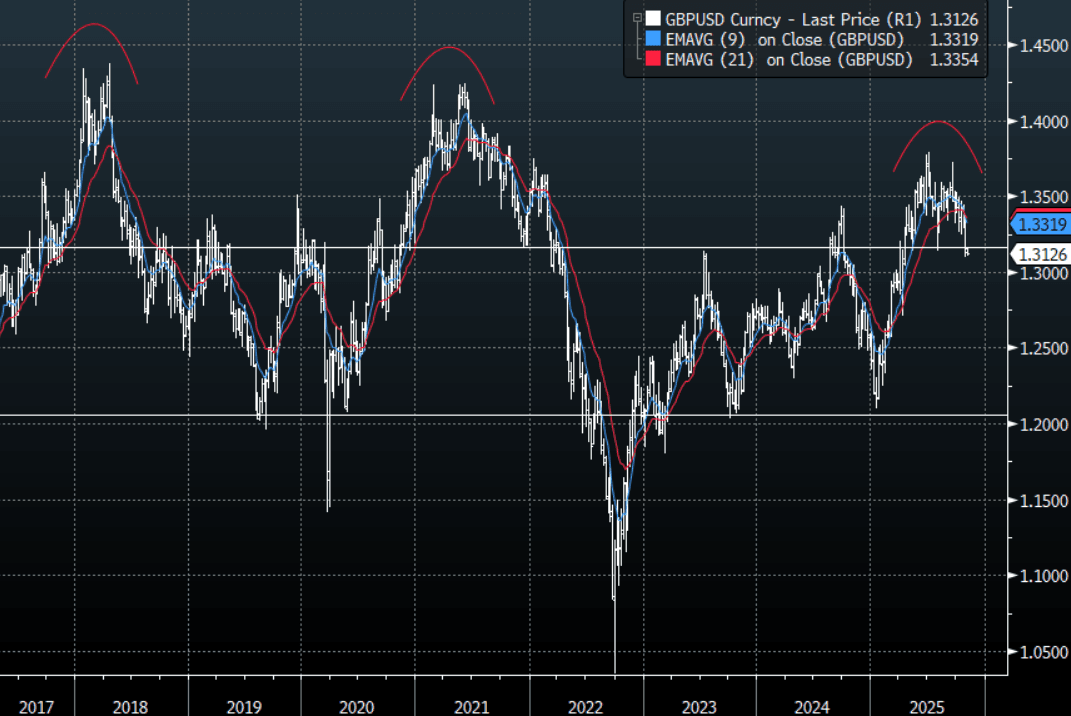

- GBP/USD - Asian range 1.3118 - 1.3162, Asia is currently dealing around 1.3125. The pair looks to be building some downward momentum. This 1.3100/1.3150 area has proved to be supportive on more than 1 occasion this year so some work around this level could be expected. I continue to favor fading rallies though as GBP attempts to put in a medium term top.

- Cross asset : SPX -0.45%, Gold $3988, US 10-Year 4.1050%, BBDXY 1222, Crude Oil $60.90

- Data/Events : Italy New Car Registrations YoY, France Budget Balance YTD, Spain Unemployment Change

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P